")

Better than expected data on the Chinese trade balance (-0.9% imports/-6.6% exports) and the hope of a prompt reopening of business in the US have been enough to spark investor optimism.

The USA

The three leading North American indices registered gains for the day despite the earnings of banks such as JP Morgan, and Wells Fargo, who announced notable falls of over 60% in their P&L accounts. Banks have allocated considerable sums to provision the non-performance loans that will accumulate shortly. Other companies like Johnson&Johnson still had first-quarter profits. For the next few days, other major North American banks and companies will present earnings.

But despite these rebounds in the stock markets, many investors and market analysts see no reason for so much optimism but quite the opposite.

First, the figures of the Chinese trade balance are not proof of any recovery, they are negative and only partially reflect the effects of the lockdown, surely worse numbers will be published in the coming months.

On the other hand, Trump's attempts to revamping the North American economy are considered by all analysts to be premature. He finds opposition from many of the governors of the states. The President has announced an appearance within two days to present the measures in this regard.

The new normal

In any case, the return to economic normality will be very uneven in the different areas of the country. Therefore, there will be inactive areas of economic importance that will undoubtedly affect the GDP of the United States considerably.

But the most important and what will undoubtedly have a more lasting negative effect will be the fall in domestic demand. With millions of unemployed in the country who will see their purchasing power significantly reduced and consumer confidence to a minimum, it will be useless to restart the productive force, even partially, if there is no demand from the population.

Everyone agrees that normality will take many months to reestablish itself, and organizations such as the IMF predict that the global economy will suffer the worst blow since 1930.

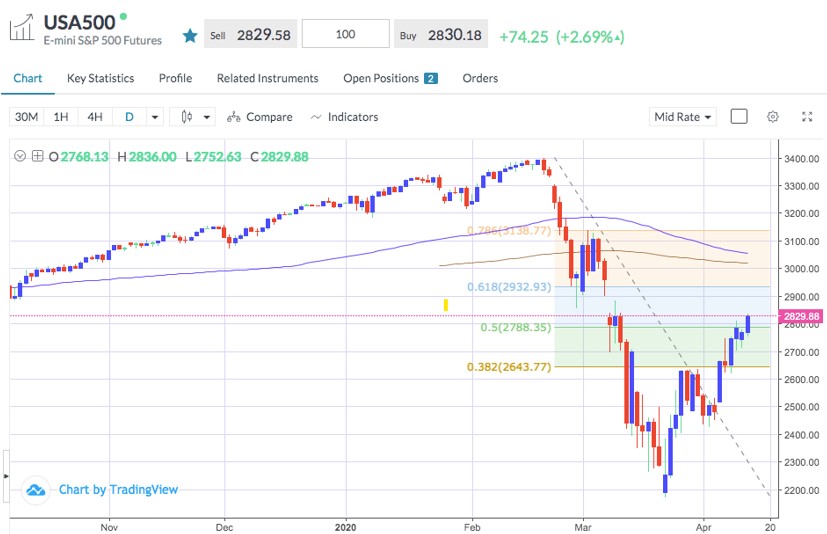

If we take all this into account and compare it with the fall suffered by the stock markets in the 2008 crisis that was over 50% in several months, most analysts agree that a drop in the indexes of around 16%, now , does not reflect the true situation of the economy and that, in the near future the markets will continue to experience downward pressure.

USA500 has already corrected above 50% Fibonacci of the entire decline and finds resistance in the bearish gap between 2850-2880.

In the currency market, on the other hand, the risk-off situation is being reflected mainly in USD/JPY that has continued to drop and has stopped at a support level of 106.85, below which it makes way for further losses to the 105.15 zone. In general terms, the Dollar is in a downtrend, also against the CHF, EUR, and GBP, which, according to public market sentiment, will continue soon.

The commodities

Another asset that faithfully reflects risk aversion in the market is GOLD, which has continued its impressive bullish momentum and is heading towards a first target in the area around $1,795 per ounce.

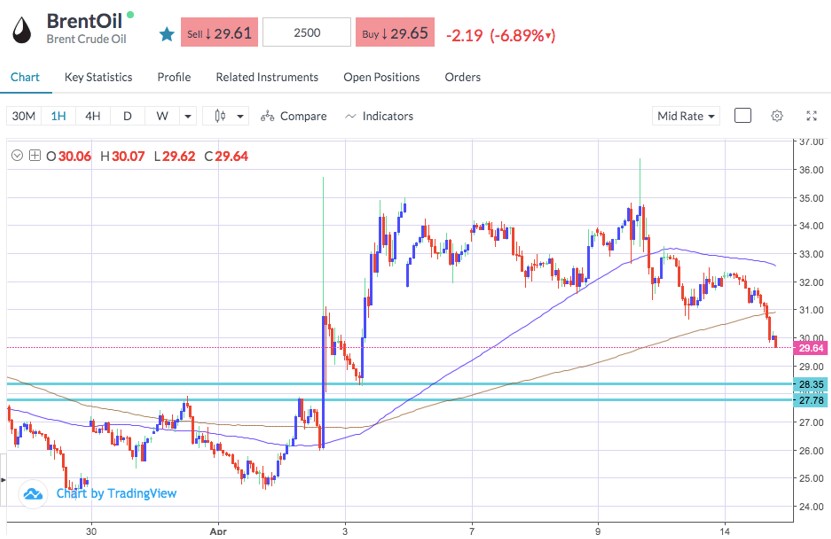

Lastly, Crude Oil, as we pointed out yesterday, has not reacted to production cuts in the OPEC+ and G20 countries as it is considered insufficient to offset the drop in global demand and has lost much of the territory gained in recent days. For the future price action of this asset, the publications of stocks, which currently re-enter the downtrend, play a significant role. BrentOil finds support in the areas of $28.35 and $27.78.