")

Gold is starting the week on a tear, punching above $3,800/oz as traders price a late-October Fed cut and a softer dollar and yields add lift. In FX, USD/CAD is still camped near recent highs, with a wide US–Canada rate gap and mixed oil signals keeping the loonie heavy. On the equity side, Costco stays in the spotlight after a strong quarter—membership and comparables look solid—though the valuation debate is getting louder.

Gold is starting the week on a tear, punching above $3,800/oz as traders price a late-October Fed cut and a softer dollar and yields add lift. In FX, USD/CAD is still camped near recent highs, with a wide US–Canada rate gap and mixed oil signals keeping the loonie heavy. On the equity side, Costco stays in the spotlight after a strong quarter—membership and comparables look solid—though the valuation debate is getting louder.

Gold Hits Fresh Highs; Eyes on October Cut

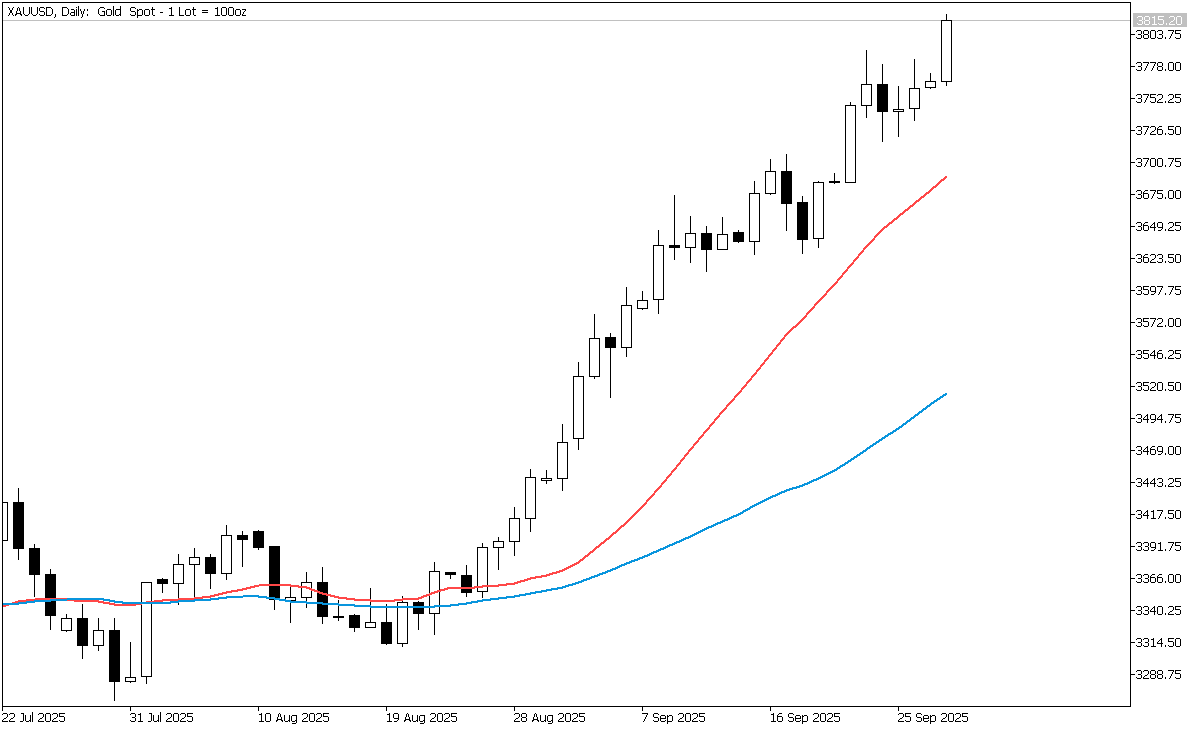

Spot gold blasted to fresh all-time highs above $3,800/oz today as the dollar eased and markets leaned harder into October rate-cut odds. Futures also printed records.

Futures imply ~90% odds of a cut at the October 29 FOMC, with December still in play. However, lower rates reduce carry, boosting gold.

The US Dollar Index drifted lower and Treasury yields edged down in Asia/Europe hours—both tailwinds for bullion.

Also, a potential US government shutdown this week is adding safe-haven demand.

Gold holdings rose to around 1,005.7 tonnes as of September 26, adding fresh metal behind the breakout. On the futures side, managed-money net long in COMEX gold is near 266k contracts into late September—supportive for price, but it raises the risk of a sharper pullback if the macro backdrop turns.

In India, even with record-high rupee prices, dealers reported the strongest premiums in ten months during mid-September as jewellers stocked up ahead of Dussehra and Diwali. August imports rose about 37% month on month, and the weaker rupee further lifted local prices.

In China, physical discounts widened to a multi-year peak, signaling softer demand at today's elevated price levels.

Globally, physically backed gold ETFs registered a third straight month of net inflows in August, taking total assets under management to a new month-end high.

The uptrend is intact, with a steady run of higher highs and fresh all-time records confirming momentum. Initial support sits at $3,790–$3,715, then $3,670. Resistance is near $3,835, followed by the $3,900 psychological extension area.

Keep an eye on upcoming US reports and what the Federal Reserve says. If a government shutdown delays Friday's jobs report, trading could get choppy, but the ISM surveys and the job-openings report will still guide expectations for an October rate cut. Also watch the US dollar and 10-year Treasury yields: if either bounces, gold's rally may cool; if they keep slipping, that's a plus for gold. Finally, track money flowing into the big gold ETF (GLD) and the balance of bullish bets in futures. Steady inflows and firm positioning support prices, while outflows or a sharp pullback in those bets would warn of downside risk.

Canadian Dollar Sruggles as Rate Gap with US Remains Wide

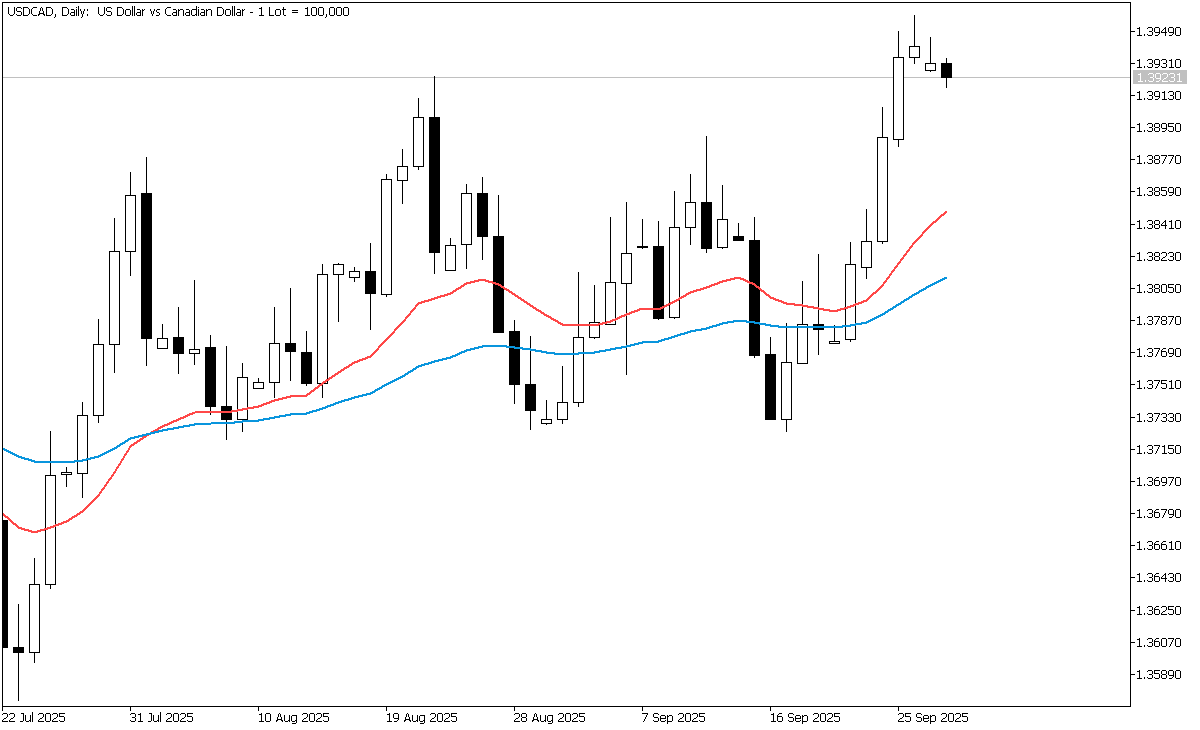

USD/CAD is holding just below recent highs after the loonie slid to a four-month low last week. The dovish Bank of Canada (BoC) signals and a firm US dollar bias have kept the pair elevated. At the same time, Friday's softer greenback and shutdown risk have trimmed topside momentum. Oil is a mixed driver: WTI eased as Kurdish exports resumed, limiting CAD support.

The dollar tone is supported by resilient US data and a market view that meaningful Fed easing will be gradual; however, a potential US government shutdown (from October 1) could delay key releases and inject near-term volatility. Into this week's prints, USD tactically softened. If data remain firm and the shutdown is avoided/brief, USD dips may be shallow. If data are delayed or disappointing, USD/CAD could retrace.

On September 17, the BoC cut 25 bps to 2.50%, its lowest in three years, citing a weaker labor market and softer growth; Governor Macklem signaled willingness to ease again if risks rise. A wider US–Canada yield gap keeps CAD under pressure unless domestic data rebounds.

Canada's economy shrank by 1.6% in the second quarter and lost more than 100,000 jobs in just two months, driving unemployment to its highest level since the pandemic. The weakness is a key reason the Bank of Canada has turned more cautious, and it's likely to keep a careful stance heading into the October 29 meeting, which weighs on the Canadian dollar. At the same time, oil prices, which usually support the loonie, slipped as Kurdish exports came back online. While Oil had risen earlier on supply worries, the restart of flows has capped those gains. Without stronger oil prices, the Canadian dollar doesn't have much to offset the pressure from softer growth and easier monetary policy.

USD/CAD maintains a bullish structure above 1.3890–1.3875 support with resistance layered at 1.3958 and the psychological 1.4000. A daily close above 1.3958 would keep the door open to 1.4000/1.4050. Failure to hold 1.3840 risks a deeper fade toward 1.3775.

The outlook for USD/CAD remains mildly bullish as long as the Bank of Canada continues easing and the interest rate gap with the US stays wide. If a US government shutdown is avoided or kept short, economic data hold steady, and oil prices stay subdued, the pair could climb toward the 1.4000 level. On the other hand, a prolonged shutdown that delays key reports, a dovish shift from the Federal Reserve, or stronger Canadian data combined with firmer oil prices could push USD/CAD back toward 1.3840. In the near term, traders will be watching upcoming US inflation releases, as well as ISM and PMI data, developments around government funding, Nonfarm Payrolls, Canada's monthly GDP report, and the Bank of Canada's communications ahead of the October 29 meeting.

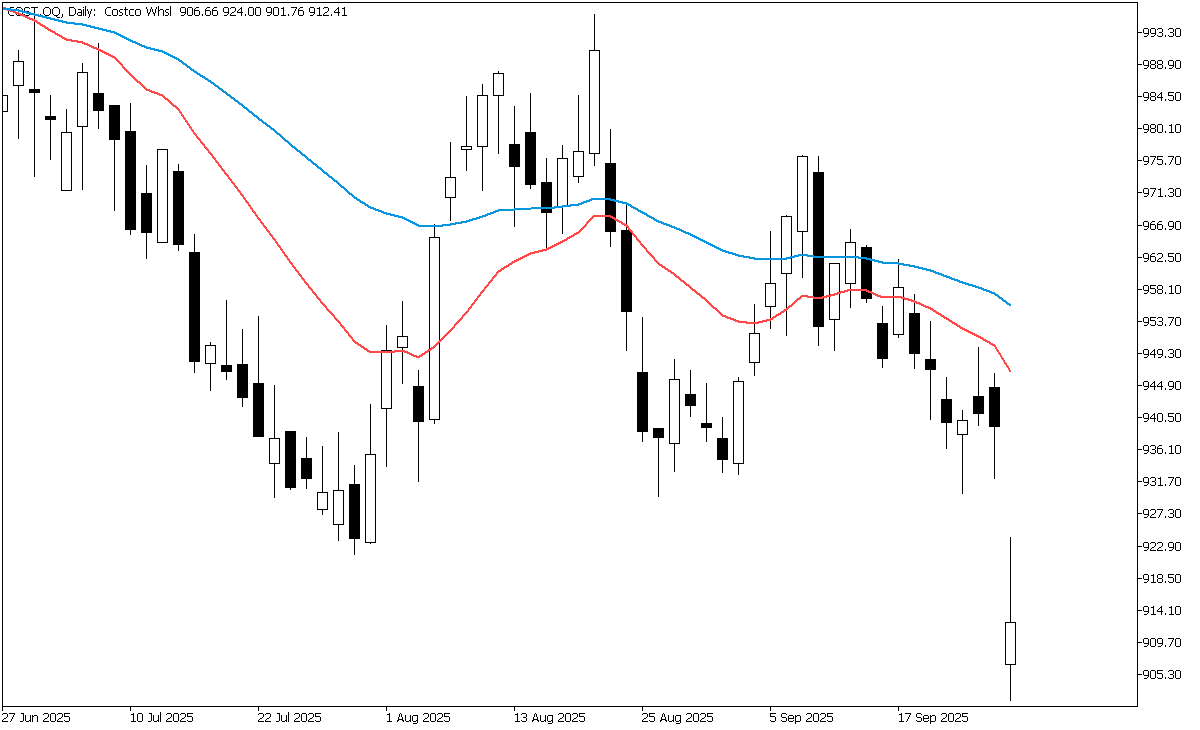

Costco (COST) Stock: Strong Results but Is the Price Too High?

Costco (COST) continues to draw investor focus after delivering a strong quarterly performance driven by resilient consumer demand and strategic membership growth. In its latest quarter, the company reported $86.16 billion in revenue and adjusted EPS of $5.87, both comfortably ahead of expectations. The key question: Can Costco sustain momentum amid inflationary pressures, tariff uncertainties, and evolving consumer behavior?

Costco operates a membership-based warehouse club model, selling high volumes of merchandise at low margins and generating significant profit from recurring membership fees. Its offering includes food, sundries, electronics, appliances, and private label (Kirkland Signature) goods. This model emphasizes efficient operations, inventory turnover, and tight cost control. As inflation squeezes household budgets, Costco's value proposition—bulk discounts, low markups, and strong membership perks—places it in a relatively defensive retail position.

In the fourth quarter, Costco's net sales rose about 8% from a year earlier, helped by stronger same-store sales and a big jump in membership income. Same-store sales, excluding fuel, were up 6.4%. Earnings also came in slightly better than expected, with adjusted earnings per share of $5.87 compared to forecasts of $5.80. Membership fees, which are a key part of Costco's business model, grew 14% to $1.72 billion. At today's prices, Costco's stock is seen as expensive compared to many peers, but investors are willing to pay a premium for its reliable brand, steady performance, and low-risk profile. Still, some analysts warn the stock already looks "fully valued," especially given the challenges facing the retail sector.

Costco's growth is supported by a strong and loyal membership base of about 81 million people, with renewal rates that remain very high. The company also plans to open around 35 new warehouses in fiscal 2026, giving it more presence in both current and new markets. Recent operational changes, such as longer store hours and exclusive early shopping for Executive members, have already boosted weekly US sales by about 1%. On the sourcing side, Costco's strategy of focusing on a limited range of categories, relying more on regional suppliers, and leaning on its popular Kirkland private label helps cushion the impact of tariffs and import costs.

One risk for Costco is that much of its future growth may already be reflected in the current stock price, which leaves little room for disappointment. Rising costs such as freight, wages, and raw materials could also pressure profits if the company cannot fully pass them on to shoppers. Tariffs and unpredictable trade policies add another layer of uncertainty by raising sourcing and inventory costs. Shifts in consumer behavior matter as well—if inflation keeps straining budgets, people may cut back on non-essential purchases, even at value-focused stores like Costco. Finally, growth in mature markets becomes harder to achieve, while international expansion brings challenges ranging from regulations to logistics and competition.

Costco is one of the strongest names in retail, with a reliable membership model and efficient operations that help it handle inflation and economic uncertainty. But because the stock is already expensive, there isn't much room for mistakes. For investors seeking steady growth and dependable cash flow, Costco appears attractive, although it's essential to monitor whether rising costs erode profits and whether new store openings meet expectations.