")

The American stock markets have fluctuated today between losses and gains, and the Europeans started the day weaker, which was reflected in declines in peripheral stocks like Spain and Italy.

Frictions between the United States and China continue, a report that advisers to the President of the United States are planning to destabilize the peg of the Hong Kong Dollar to punish China has had adverse effects on the market.

HSBC holding PLC stocks have fallen more than 3% with the news.

The result of a survey published by a popular website specialized in the distribution of credit cards in the United States, in which the majority of consumers in that country express their intention to reduce their expenses soon due to the uncertainty about the crisis has not helped maintain an optimistic sentiment in the market.

It raises doubts about the economic recovery as a result of the reopening of economic activity.

At the end of the month the earnings session will begin, a fact that will awaken enormous interest from investors due to the uncertainty of the results, so it would be logical to think that in the previous dates there will be a range trading market and directionless, something that the market seems to be anticipating to a great extent.

In the commodity markets, by contrast, we are witnessing a substantial bullish momentum.

GOLD, as already commented in previous analyzes, has continued its unstoppable bullish path and today has exceeded its first objective, the highs of November 2011 at $1802.

All the fundamental analysis factors play in favor of GOLD, the increase in the monetary base in most currencies, the manifest intention of central banks to maintain this unprecedented level of liquidity in the system and even to increase it, the problems in geopolitical relations and the expectation of a weaker Dollar.

Even in a potential future inflationary scenario that is not expected at the moment but that could emerge due to disruptions in supply chains motivated by trade confrontations, central banks would be forced to maintain the current level of rates, historically low so that real rates would further reduce by giving GOLD an extra boost.

Technically it does not have significant obstacles until the historical highs of 2011 located at $ 1920.

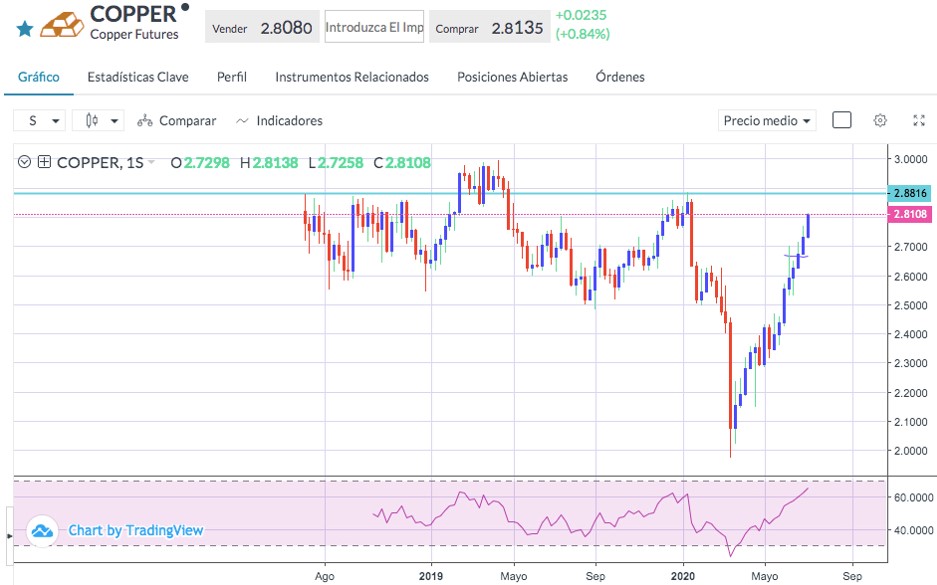

COPPER has also had no pause in its upward movement.

The economic recovery of its primary consumer, China, is behind this remarkable recovery that has brought it to pre-crisis levels in early 2020.

In principle, this should be a positive signal for the rest of the markets, although they still need a more definitive confirmation that, if so, will come with the earnings season.

Technically COPPER, in its uptrend, has room until the next intermediate resistance level at 2.88