")

With underlying Personal Consumption Expenditure (PCE) showing that work is still needed to bring inflation down, the Federal Reserve (Fed) is expected to resume hiking interest rates.

Underlying PCE fell by one tenth

Due to the American July 4 holiday, financial markets were quite quiet yesterday and expected to also have little activity today. Even though this is the case, this week is a crucial one for the markets.

The Fed's primary inflation indicator, PCE, was released last Friday. The PCE came out to be significantly below expectations, which is good news for the Fed, which has been tightening monetary policy in an effort to reduce inflation. However, the underlying PCE, which depicts the evolution of prices in a more structural way, was not as encouraging; it only decreased by one tenth and is still at an excessively high level for the 2% inflation target.

Focus on market interest rates and treasury yields

As a result, the recent hawkish rhetoric from Fed officials, especially Chairman Powell, is likely to persist for some time to come. In fact, market interest rates and Treasury yields have gone up. According to the graph, the 2-year bond is the one that is most susceptible to changes in the reference interest rate because it has a maximum yield of 4.88%.

Investors continue to anticipate interest rate increases considering the recently disclosed strong economic data, with a few notable outliers like yesterday's ISM manufacturing report, which showed numbers slightly below expectations.

Big wait of the week: Nonfarm Payroll

The Nonfarm payroll data, which will be reported this week, will, as usual, be widely monitored by traders and could provide fresh market insights. Only news that is substantially weak, such as an increase in the unemployment rate or a number of non-farm payrolls that are far below expectations, might alter the market's tendency to predict additional increases in interest rates.

Corporate earnings to start next week

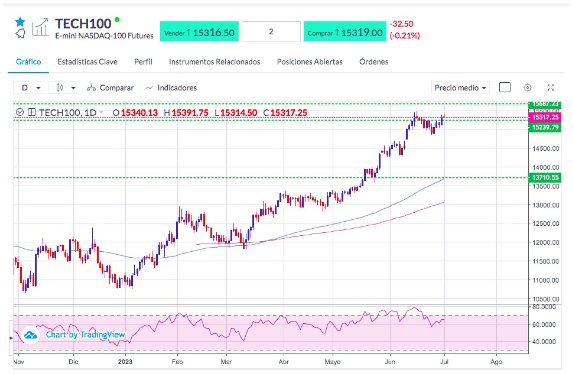

After a significant increase last Friday, stock indices are still rather stable, particularly the Nasdaq, which is still on a bullish trajectory supported by large cap technology businesses. The release of corporate results will begin next week, and this will be the fundamental factor that will affect the markets. Some of the major market participants predict that the rate increase will have a negative impact on firm revenues in the second quarter, with average reductions of 5%.

TECH100 monthly chart. Sources: Bloomberg, Reuters

Key Takeaways

- PCE came out lower than expected but underlying PCE remains at high level

- Fed expected to continue with hawkish rhetoric

- Market interest rates and treasury yields are up

- ISM manufacturing came out somewhat lower than expected

- Nonfarm payroll report to be released on Friday

- Stock indices, especially the Nasdaq, remain relatively stable

- Corporate earnings season to begin next week

Related Articles: