")

As a result of the US Consumer Price Index (CPI) for July rising less than expected and news that the number of Americans filing new claims for unemployment benefits increased last week, market sentiment shifted. This data has fuelled hopes that the US Federal Reserve (Fed) may leave interest rates unchanged at its nearest meeting.

US CPI rose 3.2% for July, opposed to expectations of 3.3%

Yesterday saw a significant shift in market risk sentiment. US indices quickly recovered on Thursday as consumer price data for July came in slightly below expectations, boosting expectations that the Fed will hold interest rates steady next month.

The CPI increased 3.2% annually in July, below the economists' forecast of 3.3%. Prices increased 4.7% during the past year, versus a 4.8% increase in the month prior, when volatile components like food and energy were excluded.

New unemployment benefit claims in the US increased above forecast

However, the number of Americans filing new claims for unemployment benefits increased by 248,000 last week, more than estimates of 230,000 additions.

All of this information raises hopes that the Fed may have already stopped raising interest rates, and 10-year Treasury yields have fallen below 4% as a result.

Hopes that the end of the Fed’s rate hikes are mounting

Both the general and core CPI are increasing at a rate of 0.2% month over month, which, if sustained, may lead to a decline in prices to levels around the Fed's objective in the upcoming months. It might take longer than a year.

It is also unlikely that the Fed will decrease interest rates because the rate of decline in inflation is still relatively gradual. This will likely happen when the labour market shows obvious signs of weakness or the economy experiences a recession, which is not currently in the cards as the current interest rate curve illustrates.

Bond yields fell but returned to previous levels

While the federal funds rate is now at 5.50%, the yields on the 5- and 10-year bonds are still around 4% and the yield on the 2-year bond is 4.77%.

The bond yields, particularly those in the middle and long section of the curve, will shift upwards if the labour market data continues to be positive and inflation declines at a slow rate.

In fact, yesterday, the yields dropped following the release of economic data but then quickly climbed back to their original levels.

Will the Dollar strengthen if inflation continues to decline?

If this situation materialises, the Dollar would appreciate and the stock markets would become more vulnerable, especially those that are most susceptible to interest rate fluctuations, such as those of technical firms.

The most impacted asset in this scenario would be gold due to the favourable, yet slow evolution of inflation and the potential long-term persistence of high interest rates.

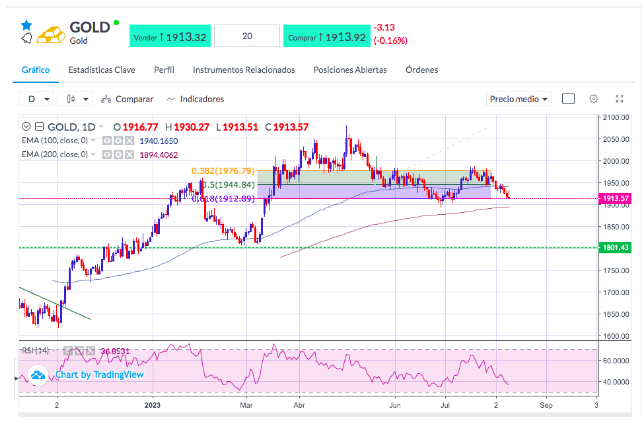

Since the middle of July, gold has been trending downward. It is now very close to the support area between $1890 and $1900.

Gold monthly chart, August 11, 2023. Sources: Bloomberg, Reuters

Key Takeaways

- US indices rebounded sharply yesterday.

- July CPI rose 3.2% annually, less than the 3.3% expected by economists.

- US unemployment benefit claims increased more than expected last week.

- Fresh data from the US is fuelling hopes that the Fed may leave rates unchanged.

- Treasury yields fell below 4% on the 10-year bond.

- Yields of the 5- and 10-year bonds are still at around 4% and the 2-year bond is at 4.77%.

- If labour market data remains strong and inflation declines, bond yields will adjust.

- The Dollar may strengthen if data continues to show this pattern.

- Gold may be the most affected asset of this kind of scenario.

Related Articles: