")

As global markets enter November 2025, traders are watching three key stories unfold across commodities, equities, and currencies. Copper, after a powerful rally earlier in the year, is now trading near 4.95 dollars per pound as momentum cools. The metal remains well supported by long-term demand from clean energy and infrastructure, but short-term worries over China's slowing manufacturing sector and a stronger U.S. dollar have tempered enthusiasm. In equities, AMD continues to ride the artificial intelligence boom, posting a 36 percent jump in third-quarter revenue to about 9.25 billion dollars. However, despite strong earnings, its stock has seen mild pressure as investors weigh competition, export limits, and high expectations. Meanwhile, in currencies, the New Zealand dollar is struggling near 0.56 against the U.S. dollar after the Reserve Bank of New Zealand's October rate cut to 2.5 percent. Weak labor data and the prospect of another rate reduction later in November have kept the kiwi under pressure, while the U.S. dollar stays firm on the back of steady data and a cautious Federal Reserve. Together, these moves highlight a market environment where strong U.S. fundamentals, cooling global growth, and shifting monetary policies continue to shape the tone across assets.

As global markets enter November 2025, traders are watching three key stories unfold across commodities, equities, and currencies. Copper, after a powerful rally earlier in the year, is now trading near 4.95 dollars per pound as momentum cools. The metal remains well supported by long-term demand from clean energy and infrastructure, but short-term worries over China's slowing manufacturing sector and a stronger U.S. dollar have tempered enthusiasm. In equities, AMD continues to ride the artificial intelligence boom, posting a 36 percent jump in third-quarter revenue to about 9.25 billion dollars. However, despite strong earnings, its stock has seen mild pressure as investors weigh competition, export limits, and high expectations. Meanwhile, in currencies, the New Zealand dollar is struggling near 0.56 against the U.S. dollar after the Reserve Bank of New Zealand's October rate cut to 2.5 percent. Weak labor data and the prospect of another rate reduction later in November have kept the kiwi under pressure, while the U.S. dollar stays firm on the back of steady data and a cautious Federal Reserve. Together, these moves highlight a market environment where strong U.S. fundamentals, cooling global growth, and shifting monetary policies continue to shape the tone across assets.

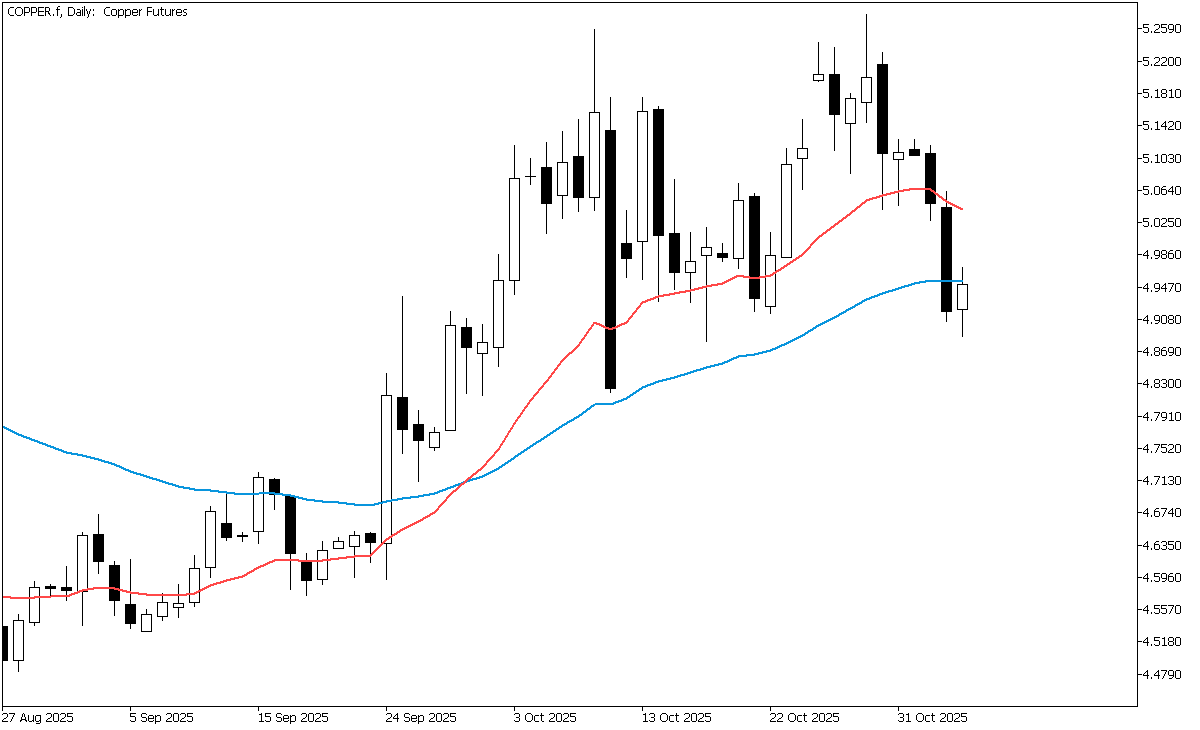

Copper Takes a Breather After a Strong Rally

As of early November 2025, copper is trading around US$4.95 per pound, keeping it near multi-month highs but showing signs of cooling after a strong rally earlier in the year. The market remains well supported by long-term demand from clean energy, electric vehicles, and infrastructure projects, but short-term sentiment has turned more cautious. Concerns about a slowdown in China's manufacturing sector, the world's largest consumer of copper, have weighed on prices in recent sessions, while a stronger U.S. dollar has added pressure by making commodities more expensive for international buyers. Overall, copper prices are still elevated, but the market appears to be catching its breath, with traders watching for clearer signals on global demand and economic momentum before taking new positions.

Strong Future Demand, but Short-Term Risks Keep Copper in Check

Copper's long-term outlook remains supported by strong demand from the green energy transition, electric vehicles, and new infrastructure projects, which all rely heavily on the metal. Growing investment in data centers and renewable power grids is also boosting its industrial importance. However, supply has struggled to keep up. Many large mines are facing delays or production issues, and new projects are coming online slowly, creating expectations of a long-term supply deficit. Some analysts even believe copper could approach US$12,000 per tonne if these conditions persist. On the other hand, short-term risks remain. If China's manufacturing and construction sectors weaken further, demand could soften and weigh on prices. Rising inventories or an increase in recycled supply could also ease the market tightness, while copper’s already elevated price means much of the long-term optimism may be partly priced in. As a result, while the long-term fundamentals look solid, the near-term outlook carries a note of caution.

Copper Caught Between Weak Demand and Looming Supply Shortage

The global backdrop for copper is being pulled in different directions. On one side, signs of weaker factory activity in China and a stronger U.S. dollar are weighing on short-term demand, making copper more expensive for buyers outside the United States. On the other side, the International Copper Study Group has lowered its outlook for global copper production and now expects the market to move into a supply shortage by 2026, highlighting the long-term imbalance between supply and demand. At the same time, the World Bank notes that while base metal prices have risen lately, slow global growth and ongoing policy uncertainty could limit further gains in the near term.

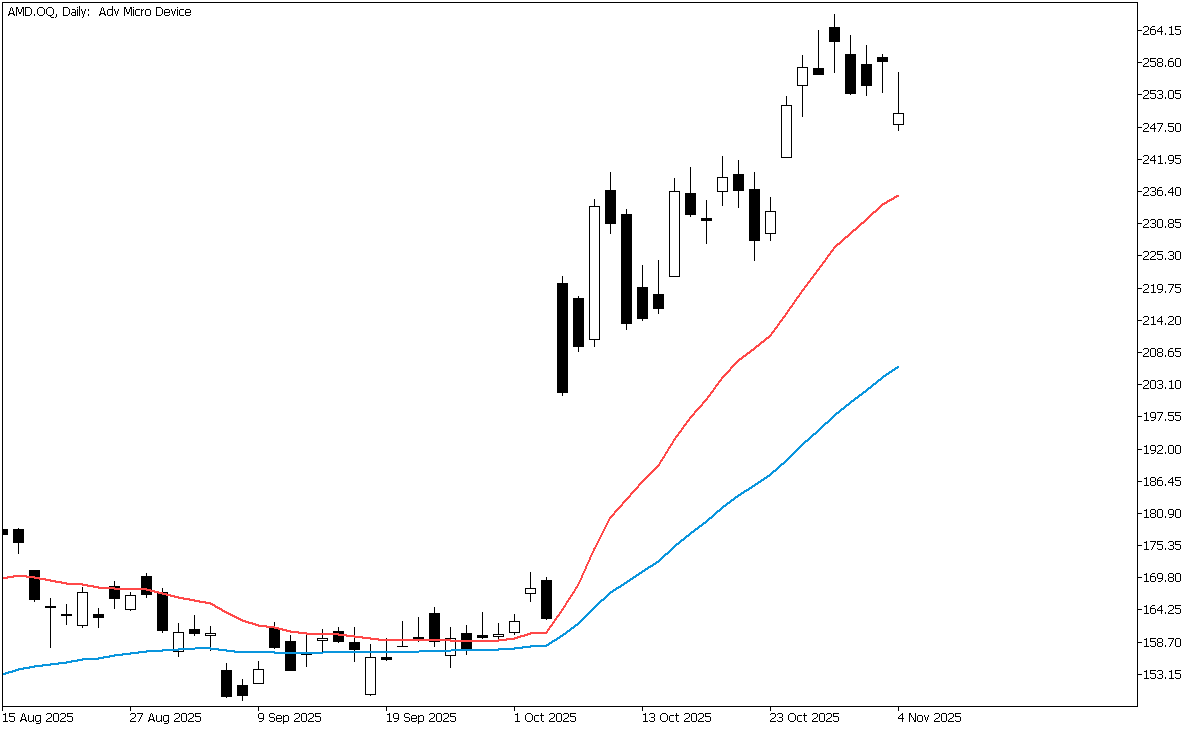

AMD Rides the AI Wave with Strong Q3 Growth and Expanding Market Reach

AMD is a global semiconductor company that designs and sells computer chips used in personal computers, gaming devices, and data centers. Its main products include processors for desktops, laptops, and servers, as well as advanced graphics and AI chips. The company does not manufacture its own chips but relies on external foundries, making efficient supply chains vital to its success. It competes closely with larger players in the fast-growing market for artificial intelligence and high-performance computing. Over the years, AMD has evolved from a traditional chipmaker into a key player focused on innovation and cutting-edge computing technologies.

AMD Delivers Strong Q3 Results but Faces Cautious Investor Reaction

AMD reported strong third-quarter 2025 results on November 4, 2025, with revenue of about 9.25 billion dollars, up roughly 36 percent from a year earlier. Earnings per share came in at 1.20 dollars, beating expectations. Looking ahead, the company guided for fourth-quarter revenue of around 9.6 billion dollars, plus or minus 0.3 billion. Despite these upbeat numbers, AMD's stock, currently trading near 250 dollars, slipped slightly in after-hours trading as investors weighed the strong growth against ongoing competition and high expectations.

AI Boom and Strong PC Demand Power AMD’s Growth

AMD's growth is being driven by strong demand across multiple areas. Its data center business rose about 22 percent in the third quarter to around 4.3 billion dollars, reflecting the surge in interest for AI and cloud computing. The client and gaming division also jumped roughly 73 percent year over year to about 4 billion dollars, showing that AMD is gaining momentum in both enterprise and consumer markets. In addition, new partnerships with major technology firms for AI chip development are boosting confidence in its long-term growth. Together, these factors highlight how AMD is benefiting from the ongoing global investment wave in artificial intelligence, cloud services, and next-generation computing.

Tough Competition and Export Limits Test AMD's Momentum

AMD faces several challenges. Competition remains fierce, as the company continues to trail the leading player in AI-training GPUs and must execute strongly on performance, cost, and efficiency to narrow the gap. Export controls and geopolitical tensions also pose risks, with new restrictions limiting the shipment of certain AI chips to key international markets, potentially affecting growth and profit margins. In addition, with AMD's stock already reflecting high expectations, any signs of slower demand, weaker margins, or delays in product launches could make investors more cautious and trigger a pullback in sentiment.

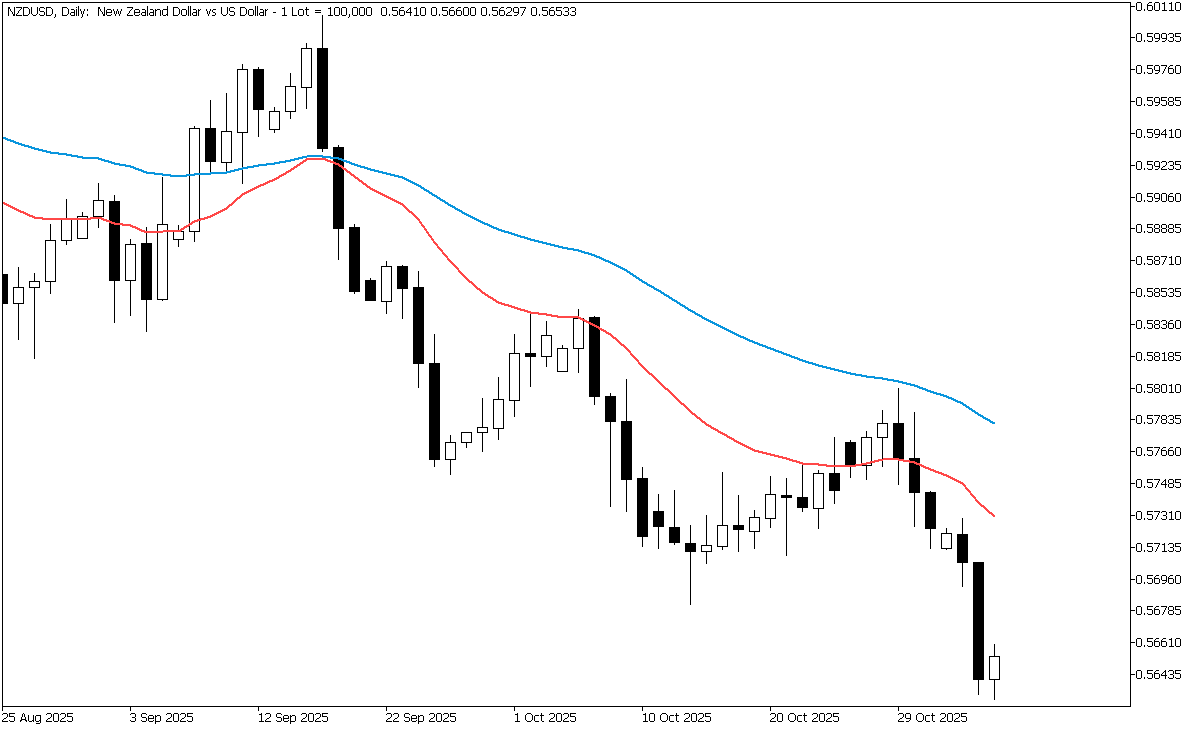

NZD Struggles as Jobless Rate Jumps and Rate-Cut Bets Rise

As of November 5, 2025, NZD/USD is trading between 0.56 and 0.57, near its weakest levels since April. Over the past month, the New Zealand dollar has slipped about 1.2 percent as investors react to soft domestic data and diverging monetary policies.

The tone remains bearish for the kiwi, reflecting growing expectations that the Reserve Bank of New Zealand will need to ease policy further to support a slowing economy. The shift intensified after New Zealand's unemployment rate rose to 5.3 percent in the third quarter of 2025, the highest since 2016, which sent NZD/USD briefly down to around 0.5640.

At the same time, the U.S. dollar remains firm, supported by steady U.S. economic data and expectations that the Federal Reserve will keep interest rates higher for longer, adding to downward pressure on the New Zealand dollar.

RBNZ Delivers October Rate Cut Amid Signs of Economic Slowdown

On the New Zealand side, the Reserve Bank of New Zealand lowered its official cash rate by half a percentage point in October 2025 to around 2.5 percent in an effort to support the slowing economy. Markets now expect another smaller cut of about 0.25 percent at the next meeting in late November. The labor market has softened, with unemployment rising to 5.3 percent in the third quarter and wage growth slowing, which strengthens the case for further easing. On a brighter note, export prices—especially for dairy products—remain relatively strong, offering some support to New Zealand's trade sector.

Strong Dollar Holds Firm as Fed Stays Cautious

On the U.S. side, the dollar remains strong because the Federal Reserve has taken a cautious stance and hasn't indicated any plans to cut interest rates soon. This keeps U.S. yields higher than New Zealand's, making the dollar more attractive to investors. Overall, U.S. economic data continues to outperform New Zealand's, and in times of market uncertainty, investors often move toward the dollar as a safe haven. In short, while New Zealand's economy is slowing and may need more support, the U.S. dollar still has solid backing, putting pressure on NZD/USD.