")

The notion that the US Federal Reserve (Fed) may leave interest rates unchanged at its nearest meeting was reinforced after the release of the Consumer Price Index (CPI) for August.

US Core CPI continues to fall

The mixed inflation report released yesterday increased anticipation that the Fed will hold off on raising interest rates but will refrain from announcing the end of its tightening cycle.

When compared year over year, the headline CPI increased to 3.7% from 3.2% the previous month, while the core CPI decreased to 4.3% from 4.7%.

Consequently, this mixed data – which is the inflation data that the Fed pays the greatest attention to - improves while the overall data worsens.

As long as core CPI continues to decline modestly, the effect can be viewed as neutral to slightly positive.

Stock indices saw modest growth

In expert opinion, the probability of a rate hike next week from the Fed is continuing to remain low, with a rate hike in November having a 50% possibility.

Bond yields on the market essentially remained constant after a small increase following the release of the CPI report yesterday.

The stock indices responded favourable to the data. Slight gains were observed, especially in the Nasdaq index, mainly due to the improvement in the underlying CPI, after a brief drop immediately after the figure was released.

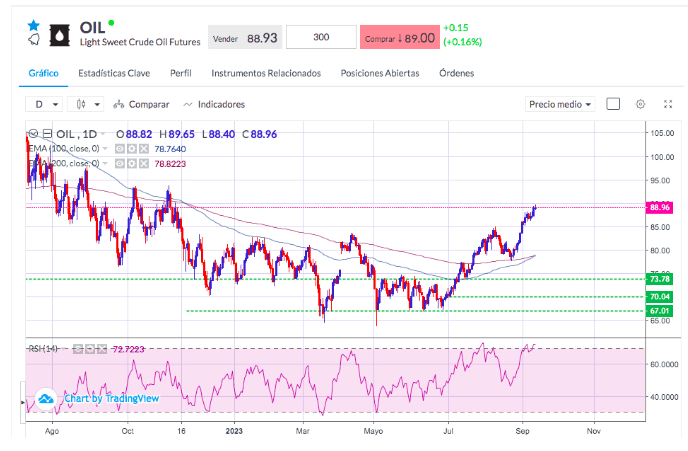

Despite the fact that the inventory data revealed a higher-than-anticipated increase, the US Dollar held steady yesterday and oil kept on its upward trend.

Technically, crude oil has already entered the overbought region on the daily chart, although there are still no indications of divergence after having approached the $90 level yesterday.

The Governing Council of the ECB meets today

Today the meeting of the Governing Council of the European Central Bank (ECB) will be held.

In analysts opinion, the market is not expecting the ECB to raise interest rates again in the wake of the troubling economic data for Europe. The data that stands out is that of Germany, which is already in a clear recession.

Although this is the case, the bank will most likely leave the option to raise rates further open for future meetings, given the continent's still-high inflation rate.

If the ECB does decide to leave rates unchanged, this could hurt the value of the Euro. The words of the President of the ECB, Christina Lagarde, after the release of Governing Council’s report will also play a role on how the Euro will react.

The EUR/USD pair has been trading near the 1.0700 level. Below that area a significant support zone can be seen around 1.0660.

Oil monthly chart September 14, 2023. Source: CAPEX.com WebTrader.

Key Takeaways

- Headline US CPI for August rose to 3.7% from 3.2%.

- Core CPI fell to 4.3% from 4.7%, which may be considered positive.

- Expectations that the Fed may leave interest rates unchanged are rising.

- Market interest rates and bond yields saw a slight spike after the release.

- Stock indices slightly rose, especially the Nasdaq index.

- The US Dollar remained stable.

- Oil continued to rise even though inventory figure came out greater than expected.

- The Governing Council of the ECB will meet today.

- A raise in interest rates by the ECB is not expected.

- The EUR/USD pair has been trading near the 1.0700 area.

Related Articles:

Sources: Bloomberg, Reuters