")

This is a relevant figure for the state of the economy, and especially for the manufacturing sector, with levels above 60 indicating a high degree of expansion. However, the employment component of this figure, ISM Manufacturing Employment for the same month, experienced a significant drop from 61.5 in the previous month to 50.9. This is not a good precedent for the labor market as it could negatively affect the important employment figure to be published this Friday.

In any case, the general data had a positive effect on the market, translating to increases in the yields of the U.S. Treasury bonds. The 10-year benchmark bond yield is heading back towards the latest highs.

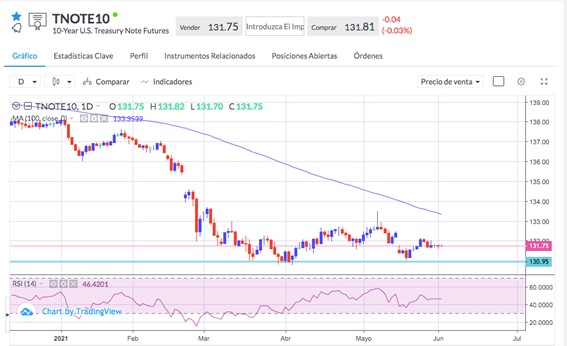

Tnote fell again, approaching the support zone currently situated at 130.95. Below this level, it could open the way to further falls corresponding to a yield of around 1.90.

The degree of uncertainty remains high, and there is still no clear position in the market about the next step for the Federal Reserve in terms of its monetary policy. What is certain is that more and more analysts anticipate when the Fed will begin to reduce its purchase of assets, placing it as early as the end of the current year, which would mean increases in long-term interest rates.

The U.S. Dollar reversed all the losses from the end of the month thanks to the rebound in yields and the end of the selling flows that were probably due to investment portfolio adjustments.

USD/JPY, the pair with the highest positive correlation with long-term interest rates, resumed its upward path. From a technical perspective, it is approaching the resistance level located around 110, which can be considered a pivot in the current technical scenario.

Sources: investing.com, Bloomberg.