")

Markets are moving through late October with a mix of tension and recalibration across major assets. The British pound is struggling as weak UK data and lingering fiscal worries weigh on sentiment, keeping GBP/USD under pressure near 1.33. In contrast, silver is attempting to recover from a steep correction, holding near $49 per ounce as investors weigh strong industrial demand against the risk of a stronger US dollar. Meanwhile, in equities, Netflix's sharp post-earnings sell-off underscores the challenges facing high-growth tech names, as slowing profit momentum and rising competition test investor confidence. Together, these moves paint a picture of markets caught between resilience and fragility—where every data release, policy signal, and corporate result has the power to shift sentiment in an instant.

Markets are moving through late October with a mix of tension and recalibration across major assets. The British pound is struggling as weak UK data and lingering fiscal worries weigh on sentiment, keeping GBP/USD under pressure near 1.33. In contrast, silver is attempting to recover from a steep correction, holding near $49 per ounce as investors weigh strong industrial demand against the risk of a stronger US dollar. Meanwhile, in equities, Netflix's sharp post-earnings sell-off underscores the challenges facing high-growth tech names, as slowing profit momentum and rising competition test investor confidence. Together, these moves paint a picture of markets caught between resilience and fragility—where every data release, policy signal, and corporate result has the power to shift sentiment in an instant.

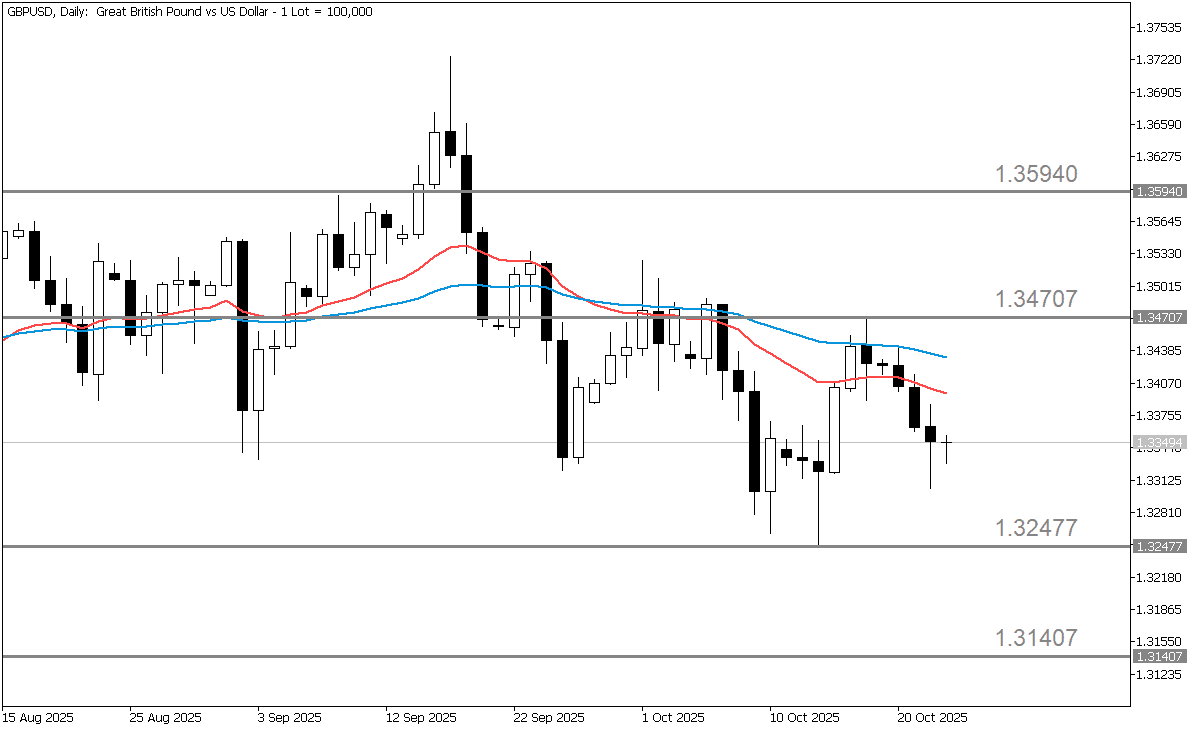

Weak Data and Fiscal Worries Weigh on the Pound as GBP/USD Struggles Near 1.3300

The UK economy is showing signs of strain, and recent inflation data came in weaker than expected — a disappointment that put pressure on the British pound and, by extension, the GBP/USD exchange rate, currently trading at 1.33510. At the same time, concerns are growing about the UK's fiscal position, as investors remain wary of how government spending and debt levels could affect long-term stability. This uncertainty has made it harder for sterling to gain momentum. On the monetary policy front, the Bank of England (BoE) remains cautious. Although inflation in the UK is still higher than in many other major economies, policymakers are reluctant to cut interest rates too aggressively, balancing between curbing inflation and supporting growth.

Dollar Finds Its Footing as GBP/USD Slides Under Renewed Pressure

On the other side of the equation, the US dollar appears to have found support, keeping GBP/USD under pressure as the pair continues to drift lower. Recent price action suggests that traders are reassessing expectations for Federal Reserve policy, with fewer betting on near-term rate cuts. This steadier dollar tone has limited any recovery attempts in the pound. Broader market sentiment has also cooled, with investors showing renewed caution and a partial return to safe-haven assets, further bolstering the greenback. Without stronger UK economic data or clearer policy signals from the Bank of England, sterling's downside risks remain in focus. Overall, the backdrop for GBP/USD looks cautiously bearish— the dollar's stability and the UK's domestic headwinds are both working against a sustained rebound.

Pound Stuck in Range as Markets Weigh UK Weakness and Softer Dollar

Looking ahead, GBP/USD is expected to remain within a broad range of 1.32 to 1.36 for the rest of the year. The pound may experience modest support if the US dollar continues to soften, though persistent concerns about the UK economy could limit significant upside. A clear move above the 1.35–1.36 zone would suggest potential for further strength toward 1.37, while a drop below 1.32 could point to renewed weakness toward 1.30. Overall, the pair appears to be in a consolidation phase, with direction likely to hinge on upcoming UK economic data, Bank of England commentary, and broader shifts in US dollar sentiment.

Silver Rebounds After 12% Dip, but the Next Move Hangs on the Dollar and Demand

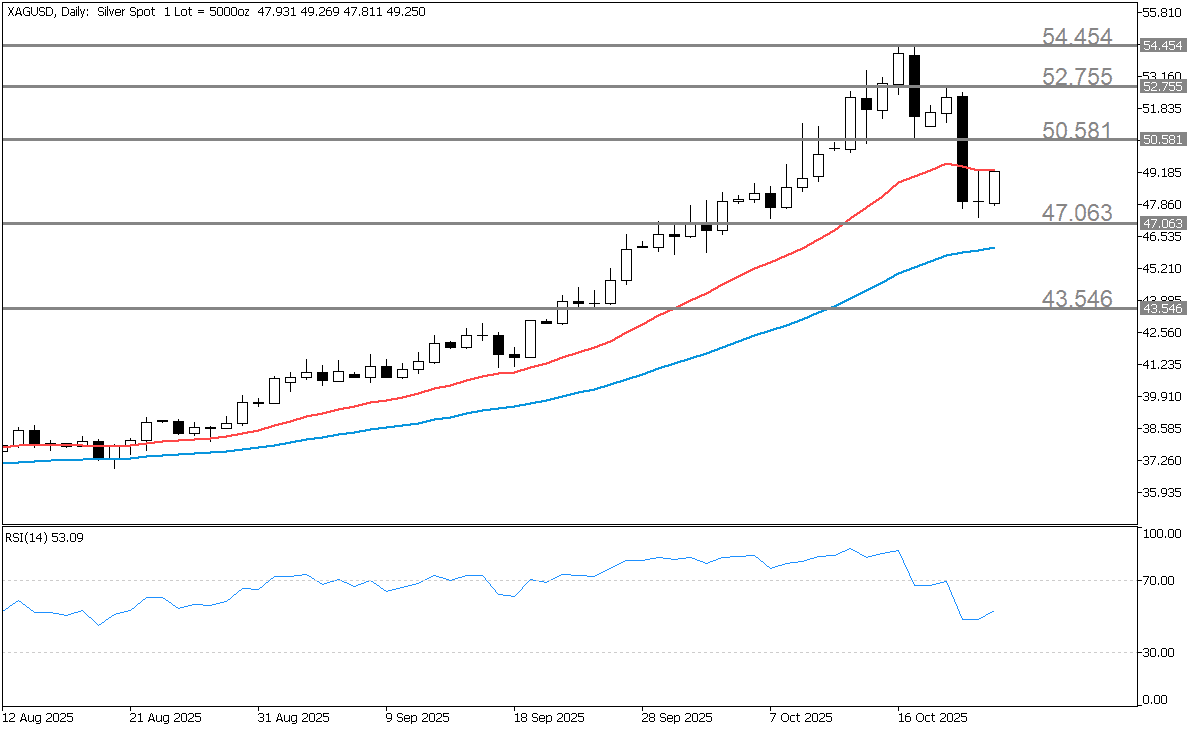

As of October 23, 2025, silver (XAG/USD) is trading around $49 per ounce, recovering after a sharp 12% pullback earlier this week. The correction followed an exceptional rally that had lifted prices from about $42 in early September to above $50 by mid-October, marking one of silver's strongest surges in years. Over the past month, the metal is still up roughly 18%, and year-to-date gains remain near 70%. Technical indicators suggest that while short-term momentum briefly cooled during the recent dip, longer-term moving averages continue to show a solid uptrend. In simple terms, silver's rally has taken a healthy breather, and the current rebound signals that buying interest remains strong as the market regains its footing after the correction.

Strong Fundamentals, Fragile Balance: Silver's Rally Faces a Test

Silver's strength is being driven by a mix of safe-haven demand, industrial growth, and supply constraints. Investors continue to favor silver as an alternative store of value amid ongoing global uncertainty, while its crucial role in electronics, solar panels, and other green technologies keeps industrial demand solid. Reports also point to tight inventories, particularly in London, suggesting limited physical supply that adds to upward price pressure. On the monetary side, weaker labor-market data and growing expectations of further central-bank rate cuts have supported non-yielding assets like silver. However, risks remain. After such a strong rally, valuations appear stretched, and a surprise shift toward tighter US monetary policy could strengthen the dollar and weigh on precious metals. Rising mining output or recycling could also ease supply tightness, while any slowdown in industrial sectors like renewable energy or electronics could dampen demand. Overall, silver's fundamentals remain supportive but increasingly vulnerable to short-term corrections if market sentiment shifts.

Silver Pauses for Breath, but Bulls Eye a Return Toward $60

In the short term, silver may experience a period of consolidation or a continuation of the recent pullback after its sharp rise, with key support seen in the $43–47 per ounce range. If prices hold above this zone, a renewed push toward $50–60 is possible, but a decisive drop below $47 could trigger a deeper correction. Over the medium term, the outlook remains cautiously bullish as long as industrial demand stays robust and supply remains tight, potentially paving the way for new highs above $60. However, if the US dollar strengthens or interest rates rise again, silver could lose momentum and drift back toward the $40–45 range. For investors, the strategy depends on positioning: bullish traders might look to buy on dips but manage risk carefully, while neutral or hedged players should monitor support levels and protect gains with stop-losses. Bearish positions make sense only if both technical and macro signals—such as a stronger dollar or a hawkish Fed stance—start turning against silver.

Streaming Giant at a Crossroads: Netflix Balances Growth, Competition, and Valuation Risk

Netflix stands as one of the world's leading entertainment platforms, boasting over 300 million paid memberships across more than 190 countries. Its extensive library spans TV series, films, and games in multiple genres and languages, offering viewers flexible access to content anytime, anywhere. Subscribers can play, pause, and resume at their convenience, with the freedom to modify their plans as they wish.

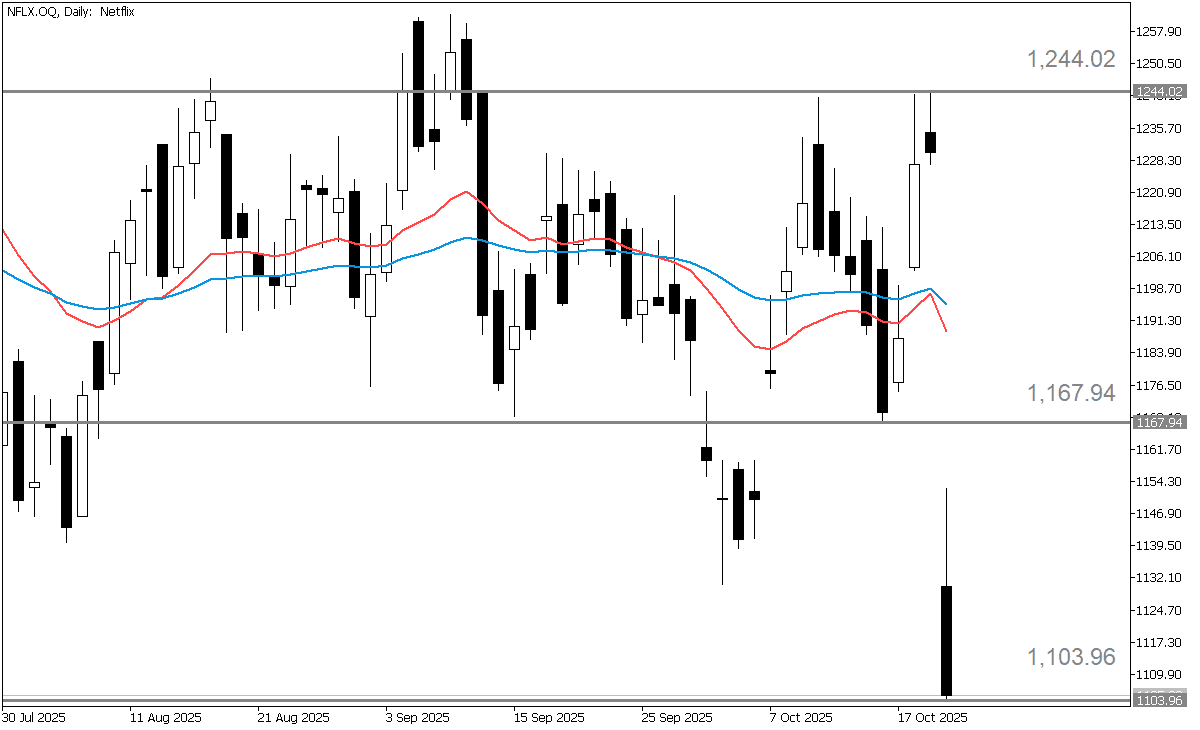

Netflix Grows Fast but Stumbles on Earnings Miss

Netflix reported Q3 2025 revenue of $11.51 billion, marking a solid ~17% year-over-year increase, supported by broad strength across its global streaming business. The company reaffirmed its full-year 2025 revenue guidance of $44.8–45.2 billion, representing about 16–17% growth on an FX-neutral basis—meaning revenue growth calculated without the impact of currency fluctuations, to show the company's true operational performance. A key highlight this quarter was the accelerating adoption of its advertising-supported tier, with analysts expecting ad-related revenue to nearly double in 2025. Netflix also continues to shift its focus from pure subscriber growth toward monetization, emphasizing ARPU expansion—that is, earning more revenue per user through price increases, ad sales, and higher-value plans—alongside greater user engagement and international scaling.

However, the results weren't without setbacks. Despite strong top-line momentum, Netflix posted EPS of $5.87, missing analyst expectations of around $6.96. Profitability was hurt by a one-time $619 million tax charge linked to a Brazilian tax dispute. Looking ahead, Q4 revenue guidance of $11.96 billion broadly meets but doesn't significantly exceed the Street's forecast of $11.9 billion. Following the earnings release, shares fell 10% as investors reacted to the earnings miss and modest outlook, reflecting a more cautious market sentiment.

Netflix Feels the Strain as Rivals Close In

Netflix faces several notable risks and headwinds despite its strong revenue growth. Competition remains fierce, with Disney+, Amazon Prime Video, YouTube, and regional streaming platforms all battling for market share and viewer attention. Profit margins could come under pressure, as the recent Brazilian tax expense highlights both regulatory and geographical vulnerabilities, while rising content costs—particularly in live sports and gaming initiatives—may weigh further on profitability. Additionally, Netflix's decision to stop reporting detailed subscriber figures has created some investor uncertainty, as analysts now have fewer visibility metrics to gauge growth and engagement. Finally, the company's valuation poses its own risk: with high expectations already priced into the stock, even a slight earnings miss or slowdown in growth could trigger a sharper downside reaction.

Netflix's Next Act: Long-Term Promise, Short-Term Caution

The recent earnings setback, caused by a one-time tax charge and modest Q4 guidance, combined with Netflix's lofty valuation, suggests that near-term upside may be limited and the risk of disappointment remains elevated.

From an investment perspective, the outlook depends on confidence in Netflix's execution. Investors who believe the company can scale its ad business, sustain global growth, and steadily expand margins over the next few years may still find the stock appealing for long-term positioning. Conversely, for those more cautious about execution challenges, regulatory surprises, or margin pressure, the current valuation offers less cushion for error. Overall, Netflix appears to be a hold or conditional buy—attractive for patient, conviction-driven investors focused on the long game, but less compelling for those seeking immediate gains or downside protection.