")

Global markets are moving through late October with a mix of optimism and caution as equities, corporates, and currencies each tell a different story. The S&P 500 continues to hover near record highs, fueled by strong corporate earnings and hopes of steady monetary policy, though stretched valuations and policy uncertainty threaten to cool momentum. In the corporate space, Johnson & Johnson has delivered robust third-quarter results, lifting its full-year outlook and reinforcing investor confidence in its steady, diversified growth strategy. Meanwhile, in currencies, the New Zealand dollar remains under pressure after the RBNZ's surprise rate cut, as weak domestic data and global uncertainty weigh on sentiment. Together, these themes capture a market balancing resilience and risk—where strength in U.S. equities contrasts with caution in global growth and currency markets.

Global markets are moving through late October with a mix of optimism and caution as equities, corporates, and currencies each tell a different story. The S&P 500 continues to hover near record highs, fueled by strong corporate earnings and hopes of steady monetary policy, though stretched valuations and policy uncertainty threaten to cool momentum. In the corporate space, Johnson & Johnson has delivered robust third-quarter results, lifting its full-year outlook and reinforcing investor confidence in its steady, diversified growth strategy. Meanwhile, in currencies, the New Zealand dollar remains under pressure after the RBNZ's surprise rate cut, as weak domestic data and global uncertainty weigh on sentiment. Together, these themes capture a market balancing resilience and risk—where strength in U.S. equities contrasts with caution in global growth and currency markets.

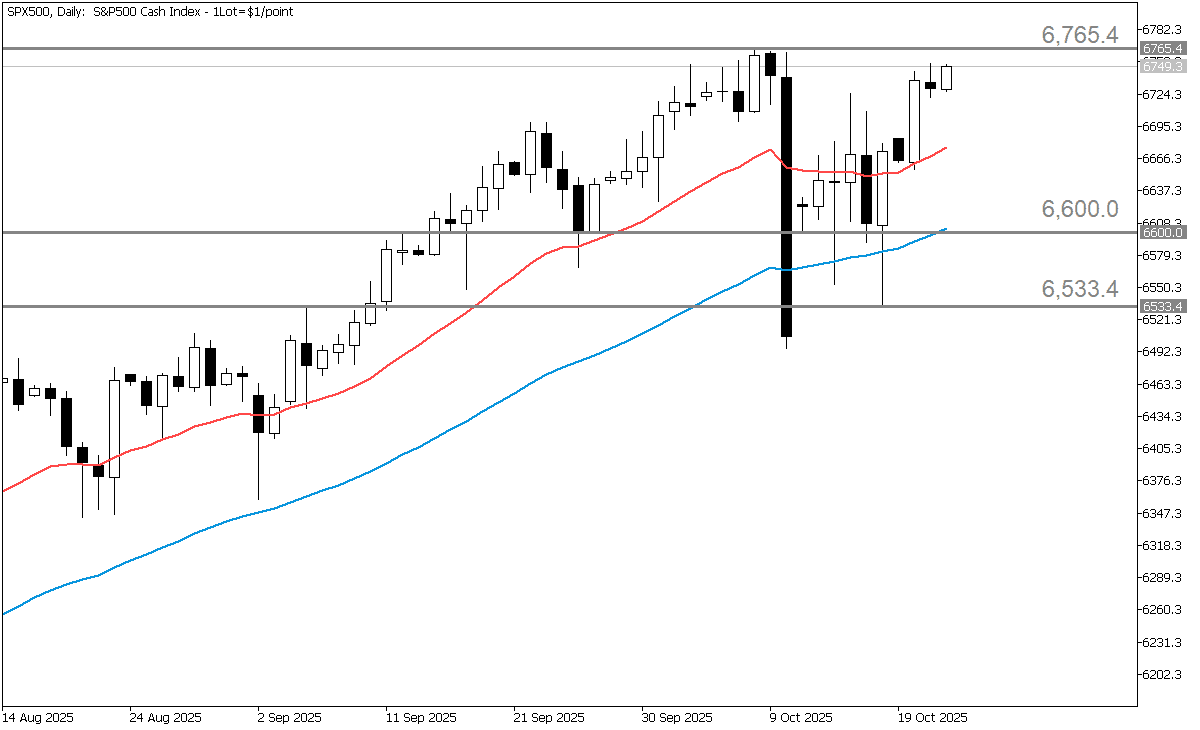

S&P 500 Near Record Highs — Can the Rally Keep Going?

The S&P 500 is hovering near record highs, trading near 6,750 as of writing. So far this year, it's up about 14.7%, helped by a 3.25% gain in September. There's been some mild volatility, including a small 3.30% drop around October 10, but overall, the market has stayed strong. Recent earnings from big banks and chipmakers have also lifted confidence, with the index climbing nearly 1.12% in October after several positive earnings reports.

Earnings Strength and Policy Hopes Keep S&P 500 Near Record Highs

Strong company earnings are one of the main reasons the S&P 500 has stayed near record highs. Analysts expect profits for major companies to grow about 9% compared to last year, and profit margins are still healthy at around 12%, which is better than the five-year average. Many businesses are also spending more on technology—especially artificial intelligence and automation—which could help boost future growth.

On the policy side, inflation and the overall economy have held up well, and earlier interest rate cuts this year have supported investor confidence. Now, traders are watching closely to see if the Federal Reserve will lower rates again or pause, since that could affect stock prices.

Technically, the market's steady rise since May may be slowing, suggesting the rally could be losing some steam. Even so, October tends to be a positive month for the S&P 500, with average gains of about 1.4%. However, risks remain—ongoing U.S.–China trade tensions, government spending debates, and the possibility of a U.S. government shutdown are still on investors' minds.

What Could Break the S&P 500 Rally?

The S&P 500 faces several risks that could slow its momentum. With the index trading near record highs, valuations look stretched, making the market more vulnerable if earnings or economic data disappoint. Technical charts also suggest that the strong uptrend seen earlier in the year may be losing steam, and a drop below key support levels around 6,600 could trigger a deeper correction. Rising U.S.–China tensions, especially if new tariffs or export restrictions are introduced, could also unsettle investors. Another concern is monetary policy—if the Federal Reserve unexpectedly takes a more hawkish stance, it could weigh on risk assets. Finally, much of the market's advance has been driven by a small group of large tech and AI-related stocks, raising concerns that the rally lacks broad support across sectors.

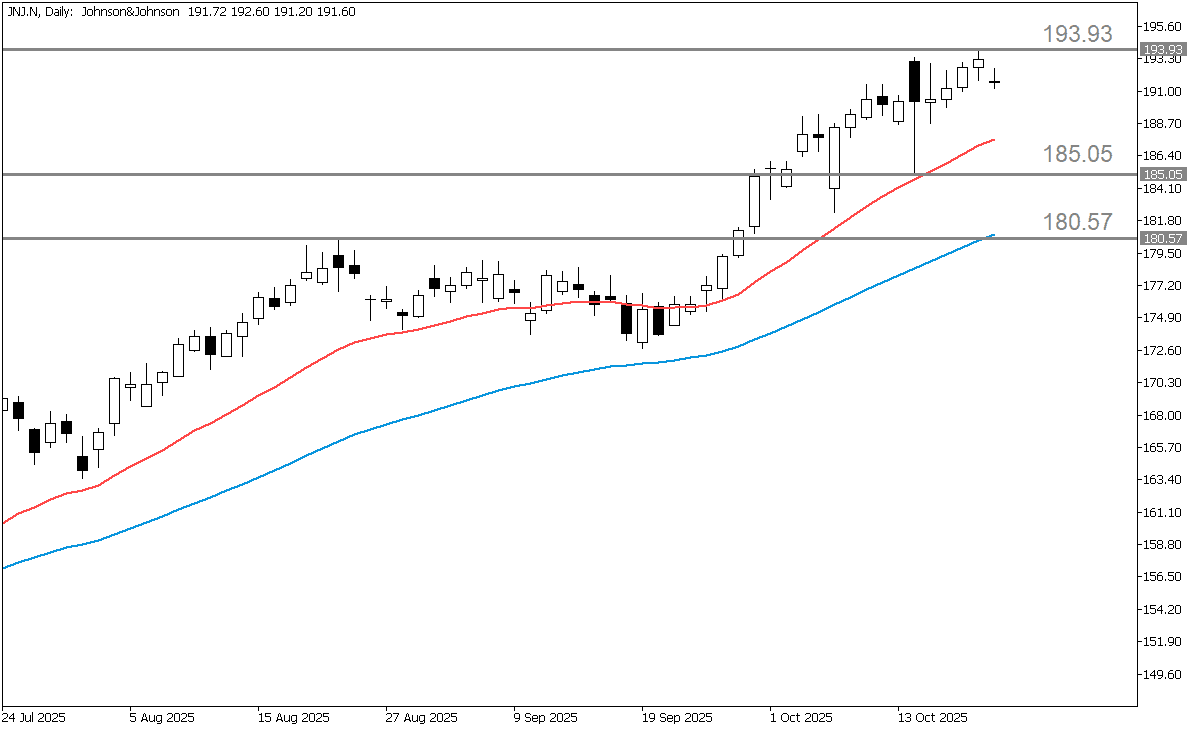

J&J Builds Momentum with Strong Earnings and a Clear Path for Future Growth

In the third quarter of 2025, Johnson & Johnson reported sales of 23.99 billion dollars, which was a 6.8 percent increase compared to the same time last year. After adjusting for currency changes and business divestitures, its operational growth came in at about 5.4 percent. The company earned 2.80 dollars per share, up from 2.42 dollars a year earlier, a gain of roughly 15.7 percent. For the full year, J&J raised its sales forecast to around 93.7 billion dollars, suggesting growth of about 5.7 percent. The company also announced a quarterly dividend of $1.30 per share, to be paid on December 9, 2025, with an ex-dividend date of November 25. Over the past decade, J&J has returned about 157 billion dollars to shareholders through dividends and share buybacks—equal to roughly one-third of its current market value.

Steady Growth and Strong Foundations Keep J&J Ahead

Johnson & Johnson's main strengths lie in its diversified healthcare business, which covers both pharmaceuticals and biotechnology under its Innovative Medicine segment, as well as medical devices through MedTech. This broad mix gives the company exposure to several growth areas and helps it stay resilient during market shifts. Management continues to focus on expanding in high-potential fields such as oncology, immunology, neuroscience, cardiovascular care, surgery, and vision. The company also stands out for its consistent shareholder returns, having raised its dividend for more than 60 consecutive years and regularly buying back shares, which reflects strong financial confidence and provides steady income for investors. J&J's decision to raise its full-year revenue outlook further signals solid business momentum, while ongoing operational improvements—especially in MedTech areas like vision and electrophysiology—highlight the company's ability to deliver steady growth.

J&J Eyes a New Era of Steady, Focused Growth

Over the next six to twelve months, Johnson & Johnson's outlook looks positive thanks to stronger third-quarter results and higher revenue expectations. If new products in areas like cancer treatment, immune-related diseases, and eye care perform well, they could help boost growth even more. The company also plans to spin off its Orthopedics business, which could create extra value for shareholders if managed well.

Looking further ahead, J&J aims to enter what it calls a "new era of growth," focusing on faster-growing parts of its business and continued investment in research, innovation, and manufacturing. The main question is whether the company can grow faster than its current pace of about five percent a year while keeping profit margins steady as older products face more competition and pricing pressure.

Key things to watch include the progress of new drug approvals and launches, growth in its medical technology division—especially in eye care and heart-related products—profit margins as temporary gains fade, management's future financial guidance, and how smoothly the Orthopedics spin-off happens. Investors should also keep an eye on outside factors like government pricing rules, biosimilar competition, and potential tariffs that could affect costs.

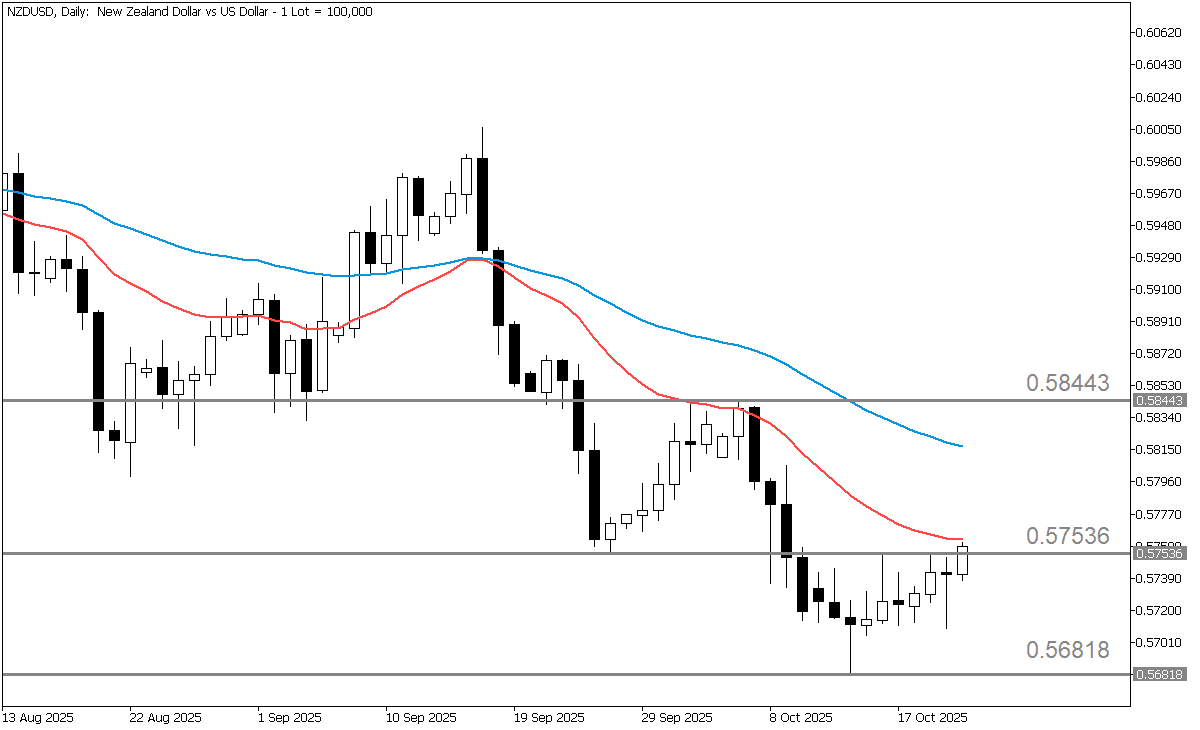

Kiwi Under Pressure as RBNZ Rate Cuts and Global Risks Weigh on Outlook

The Reserve Bank of New Zealand (RBNZ) surprised markets in early October by cutting its Official Cash Rate (OCR) by 50 basis points to 2.50%, a larger-than-expected move that underscored mounting concerns over sluggish domestic growth and easing inflation pressures. The central bank also signaled that further rate cuts remain possible if economic momentum fails to recover, reinforcing a dovish outlook that has kept the New Zealand dollar under sustained pressure. On the sentiment front, the NZD typically performs better when global growth is robust—particularly through its trade links with China and commodity exports—but tends to weaken during risk-off periods. Although recent data have shown some improvement in risk appetite across Asia, that rebound has provided only limited support for the NZD and has not been enough to offset the drag from New Zealand's domestic softness.

Kiwi Faces Crosswinds from Weak Data and Global Uncertainty

Key risks for NZD/USD revolve around both domestic and global factors. On the home front, weaker-than-expected GDP, employment, or inflation data in New Zealand would likely deepen downside pressure on the currency, especially if they reinforce expectations for further monetary easing. Any additional dovish signals from the Reserve Bank of New Zealand—such as hints of more rate cuts or a softer policy tone—would also be negative for the NZD. Externally, stronger U.S. inflation or a more hawkish Federal Reserve stance could boost the U.S. dollar and weaken NZD/USD, particularly during episodes of risk aversion that favor safe-haven assets. Global growth dynamics, especially in China, remain critical: upbeat Chinese data could lift the kiwi, while disappointments would hurt it. Given New Zealand's reliance on commodities and exports, a downturn in global demand or terms of trade would further strain the currency. Finally, as a pro-risk currency, the NZD tends to underperform in "flight-to-safety" market environments where investors move toward the dollar and other defensive assets.

Kiwi Slips as Dovish RBNZ Weighs on Momentum

The NZD/USD pair remains tilted to the downside, weighed by New Zealand's dovish monetary stance and broader structural headwinds. In the short term, the pair is likely to trade within the 0.568–0.580 range, with a bias toward the lower end and the potential to test the 0.561 support if key levels fail. Upside potential appears limited unless there is a notable improvement in global growth sentiment or a meaningful rebound in New Zealand's economic fundamentals. Traders and investors should closely monitor these critical price levels, along with upcoming New Zealand data releases and any major U.S. macroeconomic developments that could influence dollar strength.