")

Global markets end October on a mixed note. The S&P 500 trades near record highs around $6,847, lifted by cooling inflation and Fed rate-cut hopes. WTI crude oil rebounds to about $61.94, supported by trade optimism and US sanctions on Russia, though supply growth tempers gains. Ford posts strong third-quarter earnings but trims guidance as supply strains and EV costs weigh. Optimism persists, but markets remain cautious heading into year-end.

Global markets end October on a mixed note. The S&P 500 trades near record highs around 6,847, lifted by cooling inflation and Fed rate-cut hopes. WTI crude oil rebounds to about $61.94, supported by trade optimism and US sanctions on Russia, though supply growth tempers gains. Ford posts strong third-quarter earnings but trims guidance as supply strains and EV costs weigh. Optimism persists, but markets remain cautious heading into year-end.

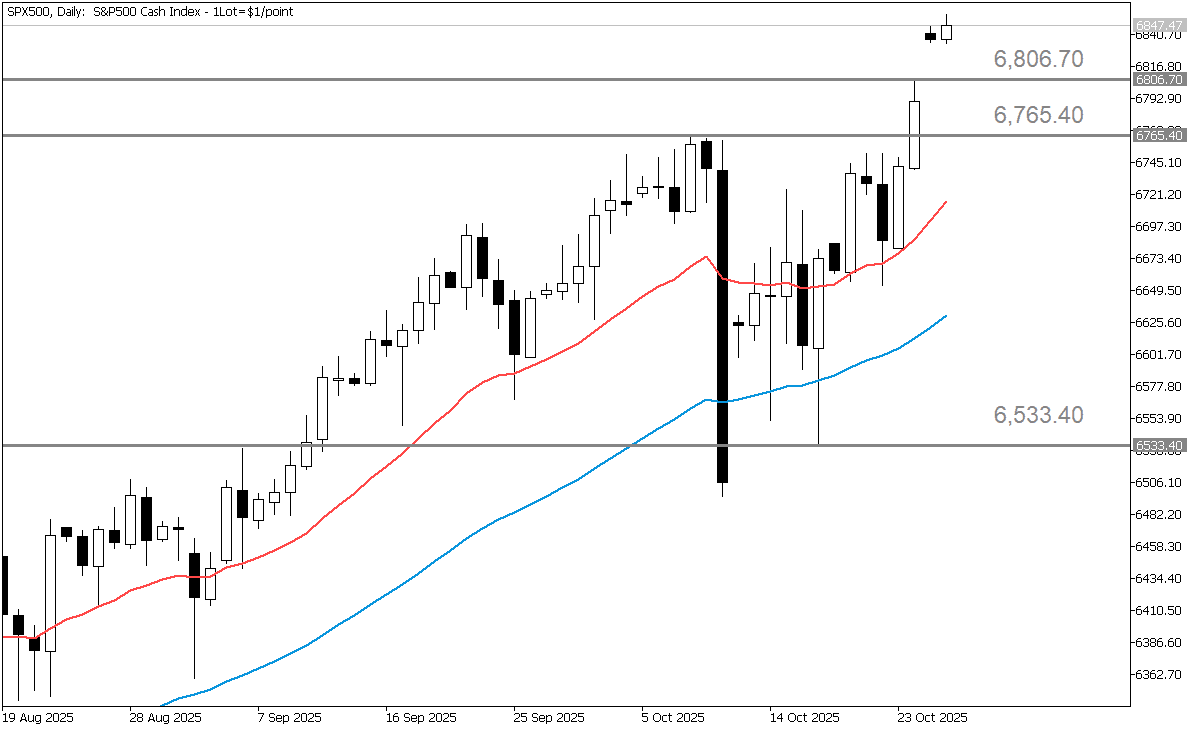

S&P 500 Hits New Highs as Cooling Inflation Fuels Fed Cut Hopes

The S&P 500 is currently trading at 6,847.27 as of the time of writing. Over recent sessions, the index hit fresh all-time highs, helped by a cooler-than-expected US inflation report, which sparked hopes of further interest-rate cuts by the Federal Reserve. Sentiment is upbeat, but the pace of gains has some market watchers urging caution.

Fed Flexibility and Tech Strength Lift Stocks — But "Macro Fog" Clouds the Outlook

On the US side, inflation is moderating, giving the Fed more flexibility to ease monetary policy—or at least signaling that the tightening phase may be nearing its end. That dynamic is supporting equities. For example, the inflation surprise lifted equities. Corporate earnings remain relatively strong, especially among large-caps and technology companies (e.g., the “Magnificent Seven"). On the flip side, global growth concerns, trade and credit risks hang over the backdrop; for example, Bank of America flagged "macro fog" and private-credit stress as risks to the index. So, the fundamental picture is favorable but not without headwinds.

Stocks Soar, But Cracks Begin to Show Beneath the Surface

Investor sentiment toward the S&P 500 is optimistic but turning more cautious. The index's steady rise to record highs has been fueled by strong corporate earnings and subdued volatility, showing that risk appetite remains healthy. However, positioning has become stretched as investors continue to pile into equities, chasing momentum even as valuations reach elevated levels. Surveys suggest that while confidence among asset managers has improved, many professionals are wary of overstretched conditions and the growing disconnect between price and fundamentals. At the same time, several historical warning signals—such as softening credit conditions and high concentration in large-cap tech stocks—are beginning to flash. In short, the mood is still constructive, but confidence feels thinner than before, leaving the market increasingly exposed to potential shocks if growth weakens or liquidity tightens.

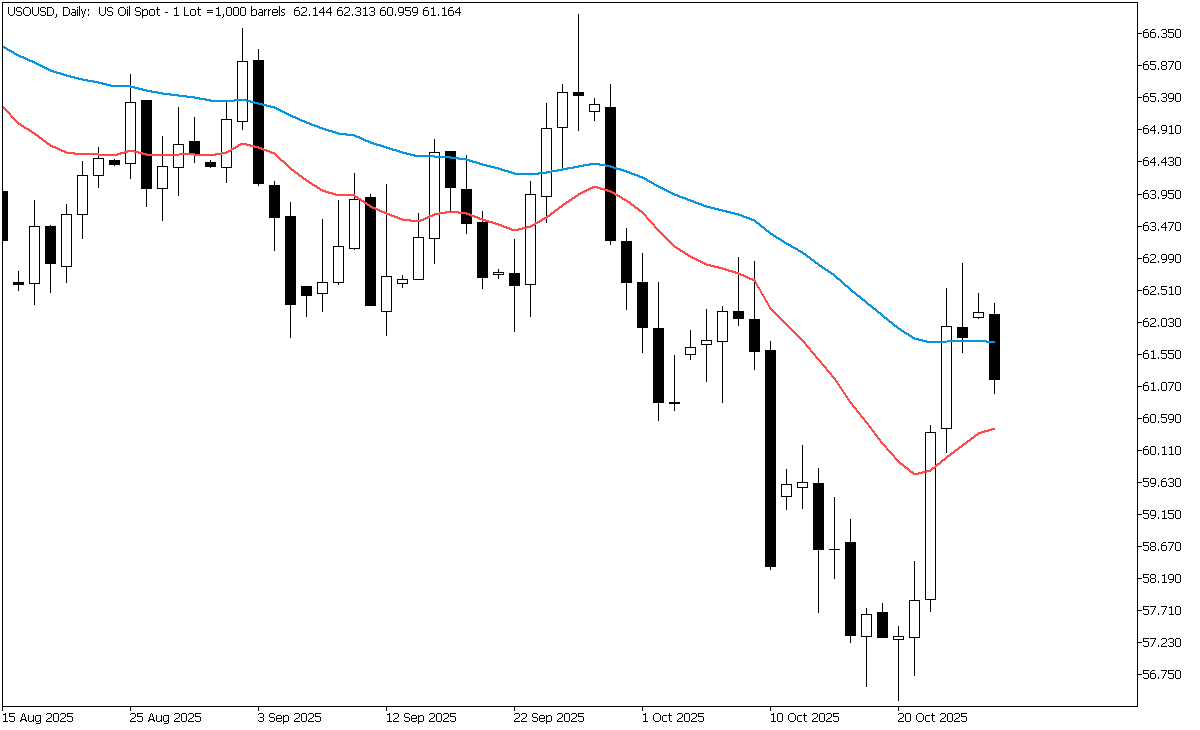

WTI Climbs on Trade Optimism and Sanctions, but Supply Clouds the Outlook

WTI crude oil is trading around US $61.94 per barrel for the front-month contract on October 27, 2025, marking a notable recovery in prices. Just a week earlier, it hovered near US$57.82, meaning the market has climbed roughly 7 percent over the past week. The latest surge reflects growing optimism surrounding the renewed US–China trade negotiations, which have eased concerns about global demand, and fresh US sanctions on Russian oil companies, which have reintroduced supply risks and geopolitical tension into the market.

On the supply side, US commercial crude oil inventories stood at about 422.8 million barrels for the week ending October 17, roughly 4 percent below the five-year average for this time of year. This level suggests the market remains relatively tight. Moreover, a one-million-barrel drawdown from the previous week underscores that supply-side constraints are still in play, adding further support to prices as traders weigh both tightening fundamentals and shifting geopolitical developments.

Geopolitics Lift Oil, but Rising Supply Keeps Caution in Play

Several key factors are driving WTI's recent price movement. On the bullish side, sanctions on major Russian oil companies such as Rosneft and Lukoil have raised concerns about possible supply disruptions, providing upward pressure on prices. Progress in US–China trade discussions has also helped ease demand concerns, improving expectations for global oil consumption. In addition, US crude inventories remain below the five-year average, reflecting underlying tightness in the market and reinforcing a sense of limited near-term supply.

However, several bearish forces counterbalance this optimism. Global supply growth continues to act as a headwind, with forecasts suggesting that inventories could rise through 2026, which would likely weigh on prices over time. Earlier in October, US crude inventories increased by 3.7 million barrels for the week ending October 3, signaling softer demand and potential oversupply risks. Moreover, if sanctions on Russia are bypassed through alternative shipping arrangements or non-dollar transactions, the current supply risk premium could diminish. Overall, while short-term sentiment remains positive due to geopolitical and supply-related factors, the broader fundamentals—characterized by increasing production and moderate demand growth—keep the market cautiously bearish.

Rate Cut Hopes and Trade Progress Keep Oil Supported

From a broader macroeconomic and policy perspective, several themes are shaping the outlook for WTI. Expectations of lower interest rates in the United States have weakened the dollar, making oil more affordable in other currencies and supporting demand. Softer labor data has reinforced market expectations that the Federal Reserve may move toward a rate cut sooner rather than later, further adding to the dollar's softness. A weaker dollar generally benefits commodities like oil, while a stronger one can act as a drag on prices.

On the global front, the emerging US–China trade framework has eased some of the concerns about slowing demand, helping stabilize sentiment across commodity markets. Still, the durability of this optimism depends on whether global growth continues to hold up; any economic disappointment could quickly reverse the gains. Geopolitically, sanctions on Russian oil remain a crucial factor. If these restrictions meaningfully reduce exports, they could tighten supply and lift prices. However, if Russia manages to sidestep sanctions through alternative trade channels, the expected supply squeeze may not materialize. Overall, the current macro and policy backdrop leans slightly in favor of oil, though the balance remains delicate and highly dependent on how trade agreements and sanctions unfold in the coming weeks.

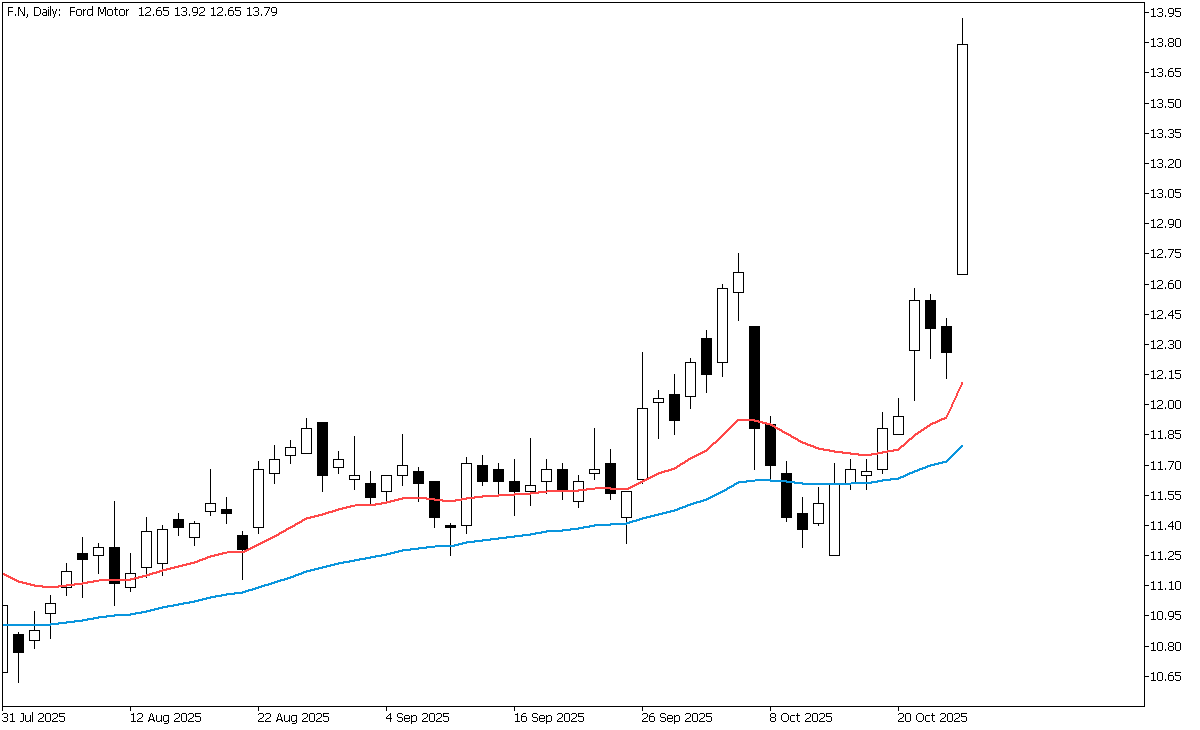

Ford Shifts Gears: Strong Quarter Underscored by Supply Strains and EV Transition Risks

Ford is a legacy global automaker producing cars, trucks, vans, and commercial vehicles under the Ford and Lincoln brands. It operates three main segments: vehicle manufacturing (ICE/hybrid/EV), commercial fleet services ("Ford Pro"), and automotive financing (Ford Credit). Ford is focusing increasingly on trucks and commercial-fleet business, areas where it sees better margins and stronger competitive positioning. It faces industry-wide transitions: electrification, supply-chain pressures, tariffs, and shifting consumer preferences.

Ford Beats Q3 Estimates

Ford Motor Company reported third-quarter 2025 revenue of approximately US$50.5 billion, marking a solid 9% year-on-year increase. The company delivered adjusted earnings per share (EPS) of US$0.45, comfortably beating the consensus estimate of about US$0.38. Despite the earnings beat, Ford lowered its full-year guidance, forecasting adjusted EBIT between US$6.0 and 6.5 billion, down from its prior range of roughly US$6.5 to 7.5 billion, and projecting free cash flow of US$2 to 3 billion. As of October 24, 2025, Ford's stock traded around US$13.79, up 12.2% on the day, with an intraday range between US$12.65 and US$13.92 on heavy volume of nearly 298 million shares. The stock briefly touched a 52-week high, reflecting investor optimism following the results. However, the market's overall reaction remains cautious—while Ford exceeded earnings expectations, the trimmed outlook signals persistent challenges from supply-chain disruptions and margin pressure.

Ford Balances Strong Growth with Mounting Challenges in a Transition Year

Ford's third-quarter results highlight several encouraging trends. Revenue rose about 9% year-on-year, showing that the company can still grow its top line even amid global headwinds. The strength of its commercial and truck segments—particularly Ford Pro and the F-Series lineup—continues to underpin profitability and cash generation. Analysts noted higher shipment volumes in these segments, reinforcing Ford's strong position in the pickup and fleet markets. The company also generated solid free cash flow of roughly US$4.3 billion in Q3, supported by healthy liquidity and disciplined cost control. This financial cushion provides flexibility as Ford continues to invest in new technologies and production capacity during a period of significant industry transformation.

Despite the strong quarter, Ford faces several ongoing challenges. A major disruption at aluminium supplier Novelis has affected output of its high-margin F-Series trucks, potentially reducing earnings by as much as US$1.5–2.0 billion. The company also lowered its full-year guidance, suggesting that management expects continued cost and supply-chain headwinds to pressure near-term results. Moreover, Ford’s heavy investment in electric vehicles—while strategically essential—remains a drag on profitability. EV margins are still weak, and the division continues to absorb high capital expenditures without matching returns. Together, these factors point to a company in transition: financially resilient, but still contending with costly structural shifts and external risks.

Ford’s Road Ahead: Recovery Hopes Meet Cautious Optimism

Looking ahead, investors should focus on several key areas that will shape Ford's performance in the coming quarters. A major question is whether the company can recover lost truck production caused by the aluminum shortage and translate that rebound into stronger earnings in Q4. Cost control and margin improvement will also be critical, as ongoing pressure from electric vehicle investments and supply constraints continues to weigh on profitability. Equally important is the execution of Ford's EV strategy—its ability to scale production efficiently, manage capital spending, and balance its hybrid and electric lineup will determine its long-term competitiveness. In addition, tariff policies and raw material trends, such as aluminum and steel prices, remain major swing factors for margins.

In summary, Ford delivered a solid third quarter but still faces meaningful headwinds beneath the surface. Its strength in trucks and commercial vehicles provides stability, yet production setbacks, cost pressures, and the capital-intensive EV transition suggest that investors should remain cautiously optimistic.