")

This week the focus has been on economic data from the US which, so far, has started to point to the slowing down of the economy. As a result, bond yields have declined, the US Dollar has weakened, and stock indices have continued to climb.

US Q2 GDP at 2.1%

Market movement yesterday was largely caused by declines in bond yields and continued weakening of the US Dollar, which are two effects of additional economic data indicating a downturn in the US economy.

The ADP private employment figure came in at 177k, less than the 195k anticipated, while Q2 GDP decreased to 2.1% from 2.4% earlier.

The 2-year bond experienced a greater loss, 6 bps, than the 3 bps drop of 10-year bond, which shows that investors are starting to wager that the Federal Reserve (Fed) won't hike interest rates again.

Focus shifts to duration of high interest rates in the US

In any case, this will largely depend on how the inflation data develops. Given the state of the market, it seems the duration of high interest rates is more important than whether or not interest rates will continue to rise.

This is where the Personal Consumption Expenditure (PCE) number that will be released today will be useful. An uptick in bond yields (market interest rates) could reverse the current market sentiment and bring about the strengthening of the US Dollar and losses in stock indices, which was seen throughout the month of August. This could be possible if the PCE data is strong and does not show a meaningful decline.

Expected PCE year-over-year is at 3.3% and underlying PCE at 4.2%

Nonfarm payrolls figure out tomorrow

Tomorrow will also be a crucial day for economic data as nonfarm payrolls and the unemployment rate will be released. Following the most recent weaker than expected labour market data (JOLTs and ADP), it is anticipated that the unemployment rate will rise, and the number of nonfarm payrolls will be below average. A surprise in the opposite direction would affect the market in the same way as a strong PCE would.

North American indices gain

For the time being, and while waiting for the release of today's economic data, the market is predicted to see another day of calm during which the North American indices, particularly the Dow Jones 30 which has now added four straight days of advances, could continue to recover some ground.

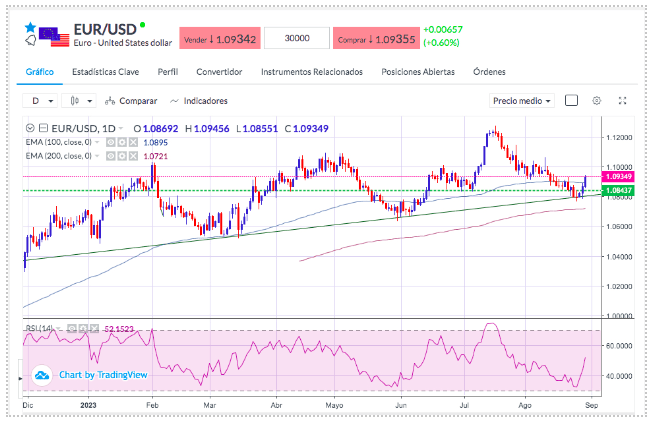

As for the currency market yesterday, the Euro/Dollar pair increased, trading once more above the 1.0900 region as the Dollar weakened under the pressure of falling market interest rates.

EUR/USD monthly chart, August 31, 2023. Sources: Bloomberg, Reuters

Key Takeaways

- US ADP private employment figure came in lower than expected at 177k.

- US GDP for the second quarter is at 2.1% from 2.4% in the first quarter.

- The fall in bonds shows investors expect the Fed not to raise interest rates.

- US PCE figures will be released today.

- US nonfarm payrolls and unemployment rate expected tomorrow.

- North American indices continue to recover some ground.

- The US Dollar fell while EUR/USD pair traded higher.

Related Articles: