")

The release of the US ISM non-manufacturing PMI yesterday came out much higher than expected, pointing to the fact that the North American economy continues to be robust in the services sector. This, and the continuous rise in oil prices, brought the yields of North American bonds up.

The US ISM non-manufacturing PMI figures for August exceeded expectations

In contrast to expectations, the US ISM non-manufacturing PMI data released yesterday showed a reading of 54.5 as opposed to the expected 52.5.

Compared to the data from the previous month of July, all the data's components—employment, new orders, and prices—showed a significant increase.

It is apparent that the services sector, which is likely to have the greatest influence on inflation, of the North American economy is still strong.

Yields of US bonds increased

The developments in the price of oil should also be taken into account as it has been rising steadily over the past two weeks. The WTI crude oil price is already getting close to the $90 threshold.

The yields on North American bonds increased again for another day yesterday, pushing the 10-year bond closer to 4.30% because of the strong non-manufacturing ISM report and rising oil prices.

Even so, the market does not anticipate a rise in the Federal Reserve’s (Fed) benchmark interest rates at its upcoming meeting; rather, it anticipates a rate cut, which is the primary cause of the market interest rate increase since last Friday and the 2-year bond yield's current level above 5%.

US indices reacted to bond sales

Bond sales are continuing, which has a negative effect on the stock markets, primarily because financing conditions are becoming more restrictive. As a result, yesterday's declines in North American indices persisted, and as is customary when interest rates markets recover, the Nasdaq technology index had the worst performance with declines of more than 1%.

Technically, this index might be developing a head-shoulder pattern with resistance near 15,500 and a neckline at 14,770.

US Dollar gained

The US currency benefits from this environment of rising interest rates and increasing risk aversion.

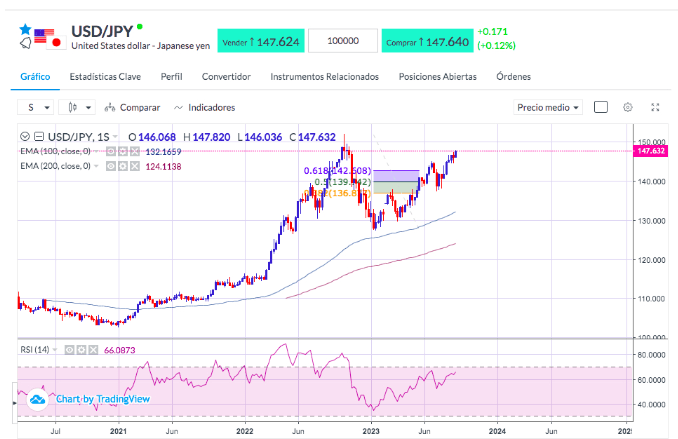

Despite potential interventions by the Bank of Japan, the Dollar has been on a continuous upward trend since mid-July, pushing the Euro to levels close to 1.07 and its price against the Yen to levels not seen since late October. Technically, the most recent highs at 151.90 serve as the next reference level.

USD/JPY monthly chart September 7, 2023. Sources: Bloomberg, Reuters

Key Takeaways

- US ISM non-manufacturing PMI data came out at 54.5.

- The North American economy continues to strengthen due to robust services sector.

- Oil prices continue to rise, with WTI crude oil approaching $90 per barrel.

- North American bond yields increased to bring the 10-year bond closer to 4.30%.

- Markets expected the Fed’s interest rate cuts to be prolonged further.

- Bonds continued to be sold, bringing North American indices down.

- The Nasdaq technology index fell by more than 1%.

- The US Dollar gained.

Related Articles: