")

Global markets are entering mid-October on uneven footing, with currencies, commodities, and equities each reflecting distinct economic crosscurrents. The Australian dollar remains under sustained pressure as global trade tensions, weaker commodity demand, and cautious RBA policy weigh on sentiment. While gold continues to shine as Australia's new export driver, overall resource earnings are softening, highlighting the fragile balance between global growth and domestic resilience. In contrast, US airline stocks—led by Delta Air Lines—are finding altitude, supported by surging premium travel demand and margin expansion, though macro risks and fuel costs keep investors wary. Meanwhile, oil markets remain subdued, with WTI struggling below $60 a barrel as rising inventories and muted demand expectations offset modest rebounds driven by shifting OPEC+ output plans. Together, these moves capture a market grappling with diverging policy paths, slowing global momentum, and a cautious risk tone heading into the final quarter of 2025.

Global markets are entering mid-October on uneven footing, with currencies, commodities, and equities each reflecting distinct economic crosscurrents. The Australian dollar remains under sustained pressure as global trade tensions, weaker commodity demand, and cautious RBA policy weigh on sentiment. While gold continues to shine as Australia's new export driver, overall resource earnings are softening, highlighting the fragile balance between global growth and domestic resilience. In contrast, US airline stocks—led by Delta Air Lines—are finding altitude, supported by surging premium travel demand and margin expansion, though macro risks and fuel costs keep investors wary. Meanwhile, oil markets remain subdued, with WTI struggling below $60 a barrel as rising inventories and muted demand expectations offset modest rebounds driven by shifting OPEC+ output plans. Together, these moves capture a market grappling with diverging policy paths, slowing global momentum, and a cautious risk tone heading into the final quarter of 2025.

Aussie Dollar Struggles as Rate Cuts, Trade Tensions, and Global Headwinds Converge

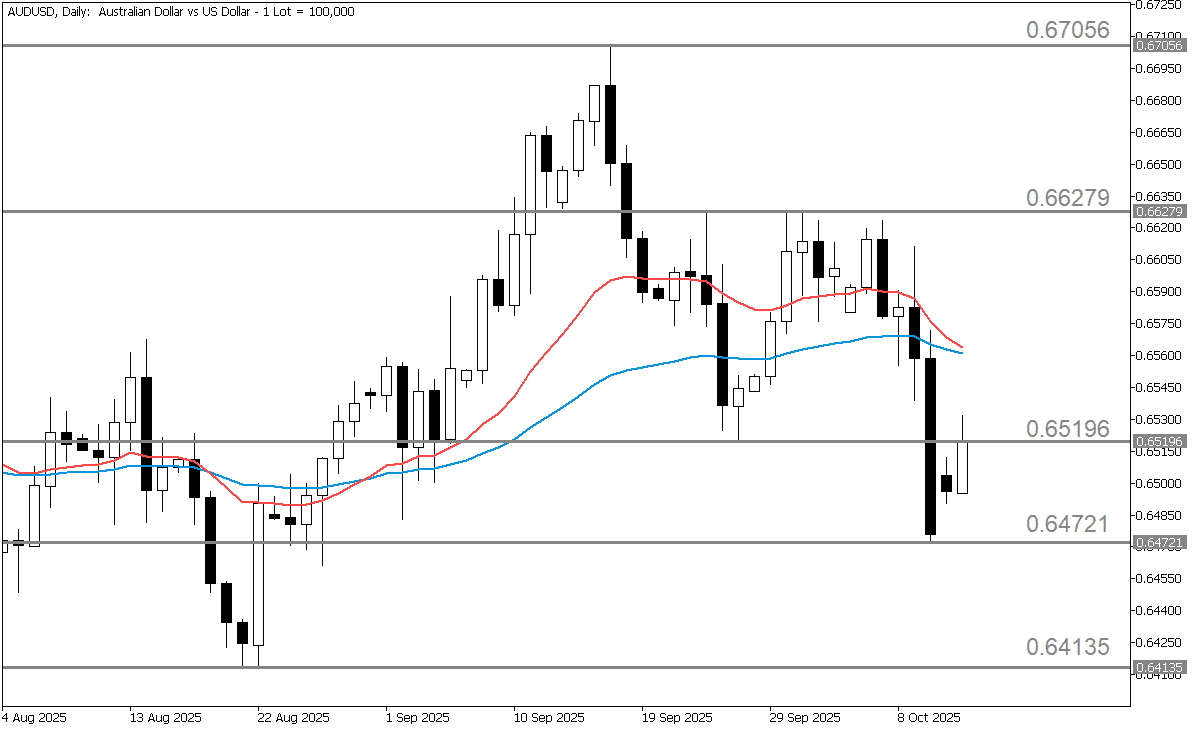

The AUD/USD pair has weakened sharply in recent sessions, trading near 0.65220 after dropping more than 1.5% month-to-date. The pair bounced off the month's low as of writing, but it remains below its 50-period EMA on shorter timeframes, reinforcing the view that the longer-term bearish momentum is still intact. Overall, the AUD is under clear downside pressure in the near term.

Gold Shines as Australia's New Export Star

Interestingly, Australia expects gold to become its second-largest resource export in 2025–26, overtaking LNG, supported by strong global gold prices. However, overall resource and energy export earnings are projected to decline by around 5% during the same period, as weaker global demand and softer commodity prices weigh on revenues. Moreover, Australia remains heavily exposed to China's economic performance, meaning that any slowdown in Chinese demand could further reduce appetite for Australian raw materials and put additional pressure on export income.

Australia Eased Rates in August as Inflation Cooled and Growth Slowed

In August, Australia's central bank cut its key interest rate by 0.25% to 3.6%, marking its third reduction this year. The move came as inflation eased into the target range of 2–3% and the economy showed signs of cooling. Policymakers said earlier rate hikes had successfully curbed demand. Still, with prices stabilizing and the labor market softening slightly, a gradual easing was warranted.

As of mid-October, the Reserve Bank remains cautious, monitoring global trade tensions and weak productivity growth that could still pressure inflation and employment. Analysts expect the central bank to maintain a data-dependent approach in upcoming meetings.

Tariff Fears and Risk-Off Mood Weigh Heavily on Aussie Dollar

Australian consumer sentiment has weakened for two consecutive months, reflecting growing caution among households. Broader geopolitical uncertainty, ongoing US–China trade tensions, and shifts in global risk sentiment continue to influence market dynamics, with the US dollar benefiting from safe-haven flows during risk-off periods, thereby pressuring the Australian dollar. Adding to the weakness, recent remarks from US President Trump about imposing higher tariffs on Chinese imports triggered a sharp sell-off in the AUD.

Aussie Dollar Faces Prolonged Pressure as Global Risks Mount

In the coming weeks, the AUD/USD is expected to stay under pressure, though short-lived rebounds or corrective rallies may occur. The dominant themes include continued US dollar strength driven by safe-haven demand, the prospect of further but gradual RBA rate cuts, weak domestic consumption, and persistent commodity and external headwinds. On the upside, if global growth—particularly in China—recovers strongly or if the Federal Reserve pivots to a more dovish stance while the RBA remains steady, the Australian dollar could regain traction. Conversely, a renewed US dollar rally, worsening global risk sentiment, or weak Australian data could accelerate losses and deepen downside momentum.

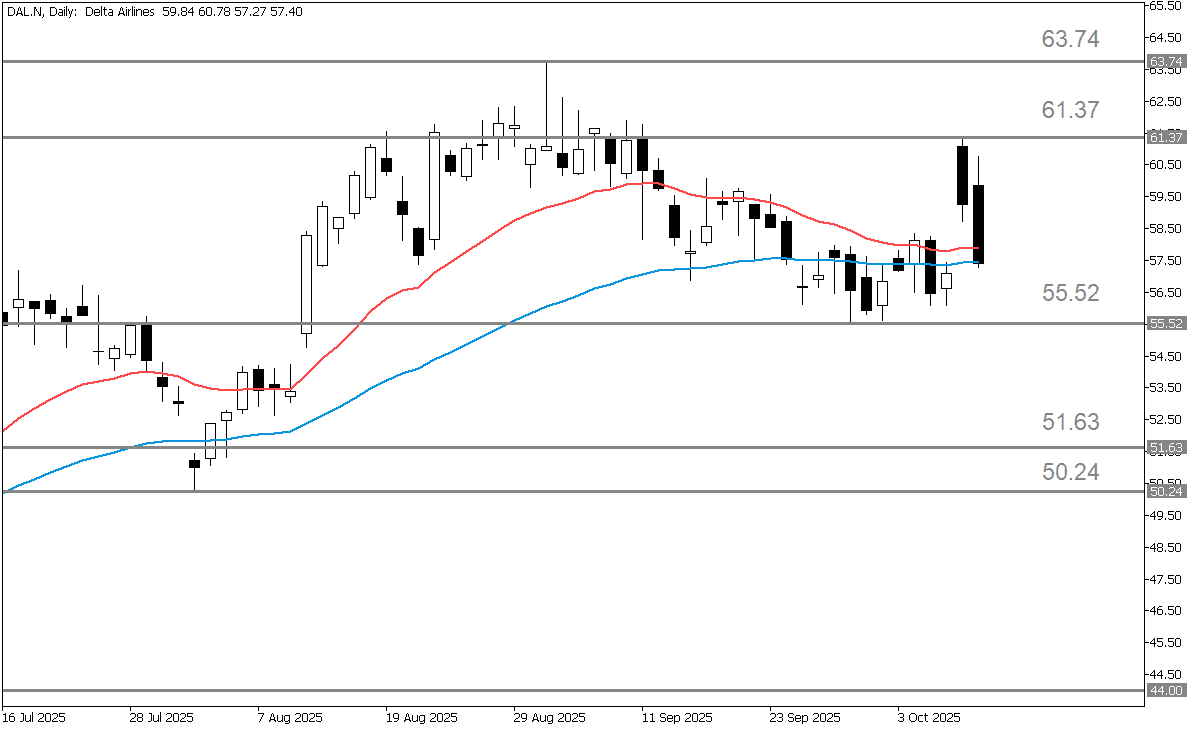

Delta's Profit Rebound Gains Altitude, Caution Prevails

Delta is riding a rebound in air travel demand, especially in premium and corporate segments, and has delivered solid recent results, restoring investor confidence. That said, macroeconomic headwinds, input cost volatility, and competitive pressures remain meaningful risks. Over the next 6–12 months, its ability to continue monetizing premium demand and control costs will be key to sustaining upside.

Premium Seats Power Delta's Profit Climb

In the third quarter of 2025, Delta Air Lines highlighted a significant rise in premium cabin revenue, with management noting that earnings from premium segments—such as first, business, and priority cabins—may soon surpass those from the main-cabin economy class. While main-cabin revenue fell about 4% year over year, premium revenue increased roughly 9%, underscoring the airline's strategic focus on higher-yield customers. Beyond ticket sales, Delta continues to benefit from diversified revenue sources, including its SkyMiles partnership with American Express, ancillary services, and its in-house maintenance and repair division. This ongoing shift toward premium and diversified income streams provides a meaningful margin tailwind, assuming the trend in corporate and premium travel demand holds steady.

Delta Eyes Higher Margins, Cautious on Costs

Looking ahead, Delta Air Lines projects modest revenue growth of about 2–4% year over year in the fourth quarter of 2025, with operating margins expected to range between 10.5% and 12%, according to management guidance and recent momentum indicators. If the airline maintains its focus on premium segments and manages capacity efficiently, there is potential for further margin expansion and earnings outperformance. Analysts remain broadly optimistic, with consensus estimates pointing to roughly 20% upside from current valuations, reflecting confidence that Delta's strategic mix shift and strong travel demand can continue to drive growth. Even so, the outlook remains tempered by familiar risks—macroeconomic volatility, rising fuel costs, and demand fluctuations—that could quickly reverse gains.

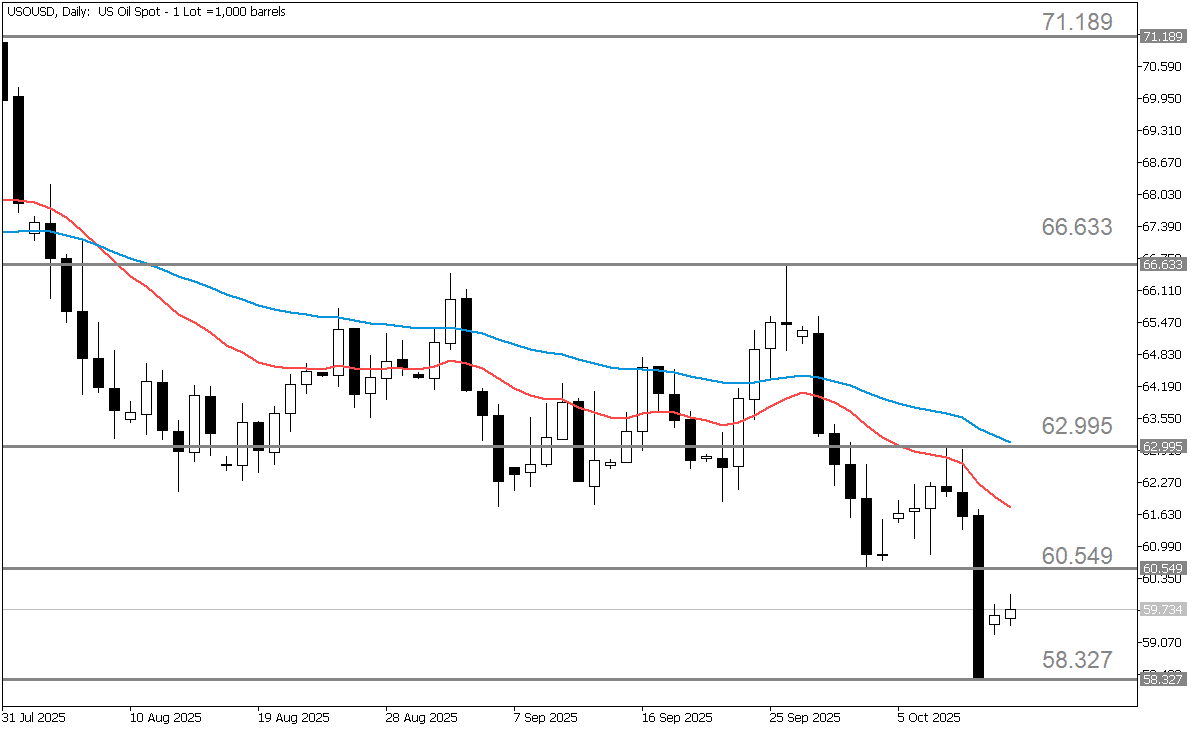

WTI Struggles Below $60 as Supply Builds and Demand Worries Deepen

As of October 13, 2025, WTI crude is trading around $59.76 per barrel, marking a 1.46% gain on the day. The rebound follows recent declines, with sentiment improving on renewed optimism over easing US–China trade tensions, which encouraged some buying interest. Despite today's uptick, WTI remains under pressure, having fallen roughly 5% month-to-date, reflecting ongoing concerns about demand softness and rising global supply.

OPEC+ Output Hike and Rising U.S. Stocks Weigh on Oil

US crude inventories rose by about 3.7 million barrels in the week ending October 3, a larger-than-expected build that added to bearish pressure. Domestic production remains strong at roughly 13.6 million barrels per day, further contributing to the supply overhang. The US Energy Information Administration projects that OPEC+ will continue gradually increasing output as it unwinds earlier cuts, leading to a steady rise in global inventories through 2026. In line with that trend, OPEC+ announced on October 5 a planned output hike of around 137,000 barrels per day for November, signaling a more assertive approach to maintaining market share.

Weak Demand Fears Keep Oil Bulls in Check

Demand concerns remain a key headwind for the oil market, with heightened US–China trade tensions and the risk of a broader economic slowdown weighing on sentiment. Geopolitical risk premiums linked to the Ukraine–Russia conflict and Middle East tensions have also eased, removing one of the earlier supports for crude prices. Meanwhile, growing US fiscal risks, including the threat of a government shutdown, could further dampen economic activity and energy consumption.

WTI Poised to Drift Lower Unless Fresh Catalysts Emerge

In the near term, WTI crude is expected to remain under pressure as soft demand, rising supply, and easing geopolitical risks suggest a period of consolidation or a gradual move lower toward the mid-$50 range. However, if US–China trade tensions ease significantly or a new supply disruption arises—such as in the Middle East or due to renewed sanctions—the market could stage a recovery, with prices potentially rebounding toward the $63 level or higher.