")

The assessment that investors and market participants, in general, have of the economic situation is faithfully reflected in the financial data published today, specifically the German ZEW.

This is data produced by the "Zentrum für Europäische Wirtschaftsforschung," one of the most prestigious economic research institutes globally and is divided into two different types of data.

The German ZEW Economic Sentiment measures the economic outlook for the next six months based on more than 350 institutional investor and analyst information. As a measurement unit, data above zero is considered optimistic about the economy and below zero pessimistic.

The figure published today has been 55 vs. 45 expected. This means that the leading investors in Germany expect a substantial improvement in the economy in the next six months.

The other data is the German ZEW Current Conditions. This survey is carried out at the European level, not only among investors and market analysts but also among large industrial and insurance companies. As its name indicates, it focuses more on the current situation, although without ignoring the potential projection in the medium term. It was published today with the figure of -66.5 vs. -66 expected.

As we can see, there is an apparent dichotomy that is a reflection of the current situation, with a still high degree of uncertainty. While the economy still needs to improve and this depends on various factors such as the decrease in the number of infected, the approval and administration of vaccines, the acceptance of fiscal stimulus packages promised but not yet implemented, as is the case in the United States, a satisfactory solution to Brexit ... etc.

Although all these factors remain to be resolved, investors' mood, as shown in the ZEW Economic Sentiment figure, is optimistic.

The Dollar

Due to these investor expectations, the mood is risk-on, and this is mainly reflected in a generally weaker Dollar, stock markets that remain in the upper part of their range of the last weeks, and especially in the outflow of funds from fixed-income assets.

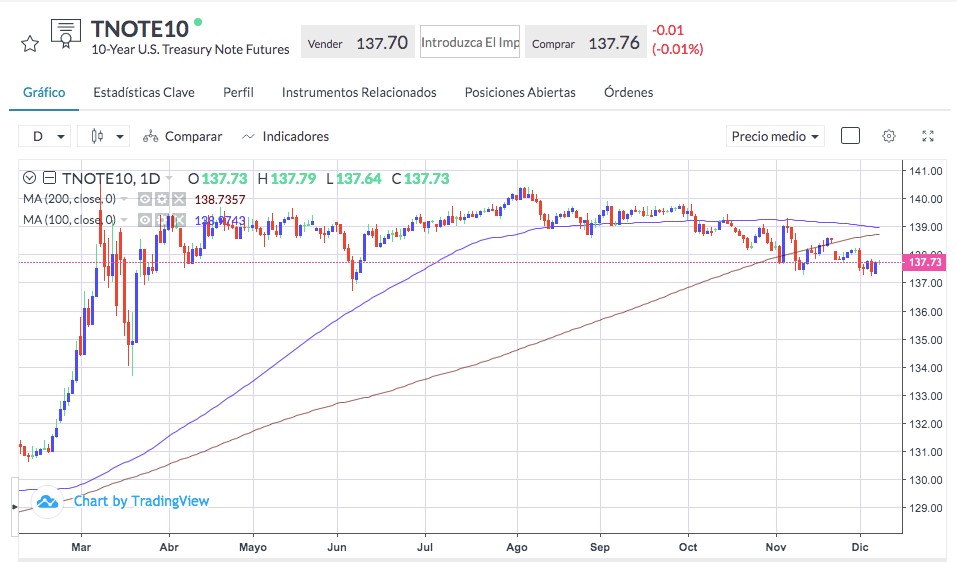

In this sense, as we can see in the graph, the Tnote, a 10-year American bond, has been losing territory from the August highs above 140 to the current price slightly below 138, which represents a yield of 0.93 % from the lowest levels in the zone of 0.50%.

This is a significant movement in this asset, even more so considering that the Federal Reserve continues to buy US Treasury bonds in the market through its asset purchase program.

GOLD

Another asset that has had a relevant movement in the market has been Gold.

After a corrective decline that led it to break the central support zone located at $1800 momentarily and pierce the 200-day SMA, the precious metal has recovered above these levels.

Today, it has managed to overcome the level of $1850 (former technical support now turned into resistance).

The sales occurred despite the Dollar's weakness, a currency with which it usually has a negative correlation and was therefore due to a technical correction given the high level of long positioning of the market.

The fundamental factors that tend to favor Gold are low real interest rates, and increased liquidity or increased money supply, as well as a weaker US Dollar, and these conditions continue to be maintained in the current market.