10 piețe globale | 100+ ETF-uri* | 5.000+ acțiuni

*Sub incidența categoriei clientului

- instrument

- price

- 24h_change

- 24h_trend

O alternativă de investiții convenabilă

Un ETF este o colecție de valori mobiliare în care poți investi fără a fi nevoie să cumperi fiecare componentă în parte.

Cu ajutorul ETF-urilor, poți tranzacționa și obține expunere la sute de acțiuni bazate pe un indice, un sector sau o anumită categorie.

De ce să investești în ETF-uri

Populare

Variate

Eficiente

Transparente

Accesibile

Flexibile

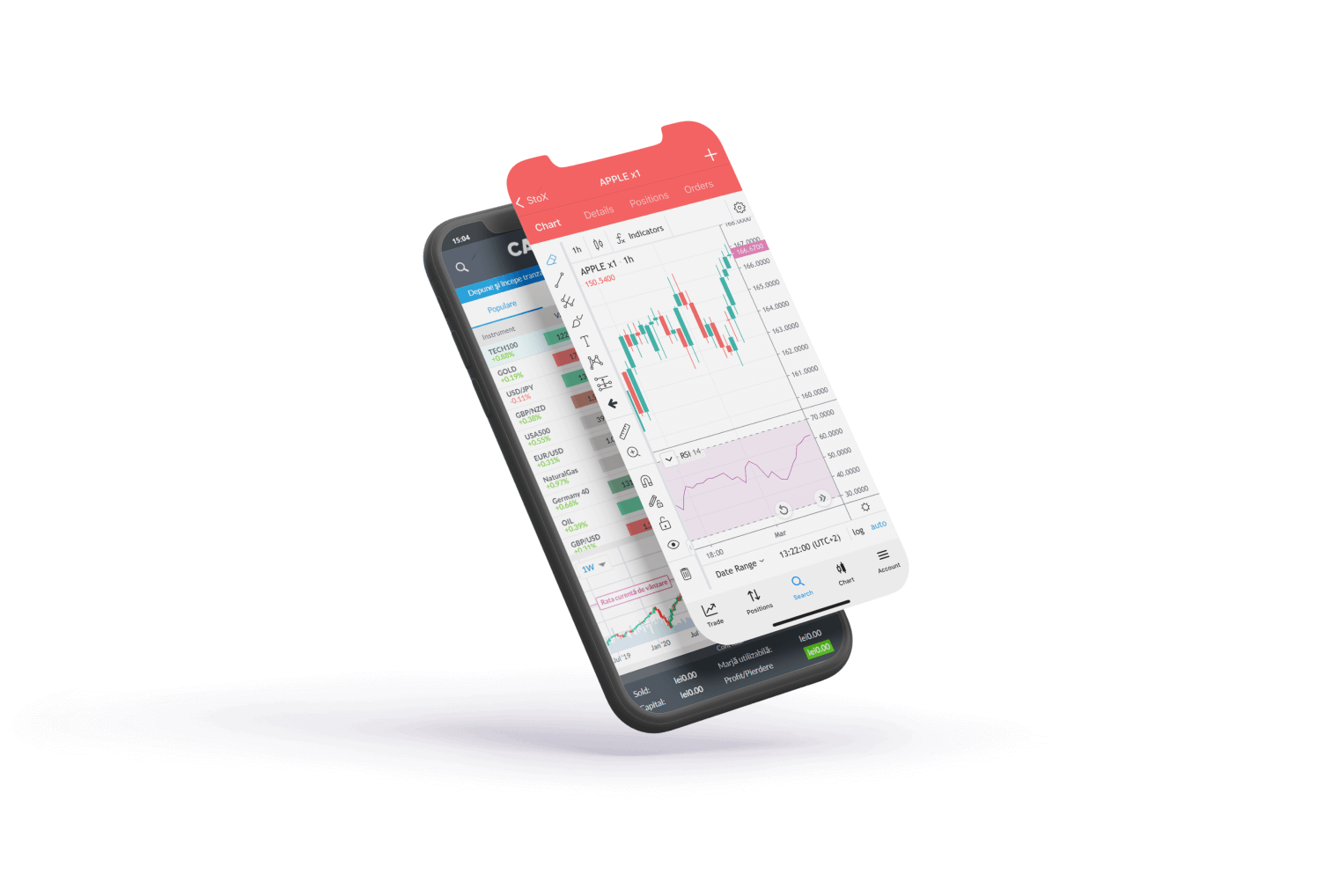

Valorificați puterea analizei multi-grafic

Beneficiază de instrumente avansate pentru a fi mereu conectat la piețele financiare și pentru a-ți construi o strategie de tranzacționare unică.

- Supergrafice

- Alerte pentru fiecare dispozitiv

- Date istorice și reprezentări

- Testeaza-ți strategiile

- Peste 100 de indicatori

- 15+ tipuri de grafice cu posibilitatea de vizualizare multiplă.

Descoperiă Perspective Unice

Descoperă beneficiile folosirii Trading Central și primește informații direct in platformă. Explorează știrile de piață și dezvoltă-ți strategia cu această unealtă tehnică disponibilă pe platforma noastra.

- Gestionează riscul cu puncte de pivot și scenarii alternative.

- Recunoaște modelele de grafice brevetate care monitorizează constant piețele 24/7.

- Funcționalități în limba locală.

- Acoperind cele mai populare instrumente financiare.

Mereu în mișcare

Tranzacționeză rapid și în siguranță. Rămâi conectat la pulsul pieței cu ajutorul aplicației noastre mobile disponibilă pentru ambele sisteme iOS și Android.

app_rating

app_rating_text

app_rating

app_rating_text

De ce

traderii aleg

CAPEX.com

Siguranță

Conturile bancare segregate păstrează banii tăi în siguranță și separați de cei ai companiei noastre

Reglementări

Cele 4 licențe de operare ale noastre aderă la reglementările stricte ale CySEC, ADGM, FSA și FSCA

Încredere

Gama variată de instrumente te ajută să îți dezvolți perspectivele de investiții

Prezență globală

5 birouri și sucursale locale, peste 400 de angajați

Știința înseamnă putere

Îmbogațește-ți cunoștiințele de tranzacționare

Descoperă cum funcționează piețele și află mai multe despre beneficiile utilizării diferitelor strategii de tranzacționare cu ajutorul videoclipurilor noastre educaționale.

ANALIZE & PREDICTII

GRAFICE IN TIMP REAL

ANALIZE & PREDICTII