After closing the

week with an increase in risk aversion caused by several factors, the main ones

being President Trump’s disease, the stagnation of the Brexit negotiations, and

a lower-than-expected non-farm payroll data, the market starts Monday in the opposite

direction with a timid return to risk-on mode.

What caused this

change? In the first place, the news about the evolution of Trump's disease. Although

still confusing, news is somewhat more positive, especially after the

announcement that the president may leave the hospital as soon as today.

The main

uncertainty in this regard was based on the possibility that Trump would remain

inactive without making political decisions. In such a scenario, President

Trump would be replaced by Vice President Pence, and would not be able to

participate in the electoral campaign less than a month before the elections.

In any case, the polls show a vast advantage for the Democratic candidate, and the market seems to have taken it positively. This is a substantial change in the approach of investors to this type of event in which a Democratic victory has meant a more defensive attitude on the part of the market. The key to this change in mindset is that the fiscal stimulus package of more than $2 trillion that the market needs to resume its bullish tone would be closer after a Democratic victory.

Brexit on the

wires again

On the other hand,

the meeting on Saturday of the president of the European commission Von der

Leyen with the British Prime Minister Johnson, although offering no final

decision, opens the doors to a continuation of the negotiations on Brexit

beyond the October 15 deadline previously unilaterally imposed by the British

prime minister.

Finally, the PMI

data published today of 48.0 vs. 47.6 expected, and of retail sales (YoY) 3.7%,

significantly higher than the expected figure of 2.2%, have contributed to improved

market risk sentiment.

Although lockdown

measures are spreading in the main European capitals due to a sharp increase in

contagion data, the general feeling is that the effects of the disease are

milder in this second wave. With these temporary measures, it will be enough to

flatten the contagion curve definitively.

This scenario has

been reflected in the market by the weakening of the Japanese Yen and a rebound

in the stock markets.

USD/JPY had recovered

more than 50 pips on the day and returned to the levels before the fall that

occurred on Friday after news of the contagion from Trump. The pair remains in

a structural downtrend that will only be broken above the 106.50 area.

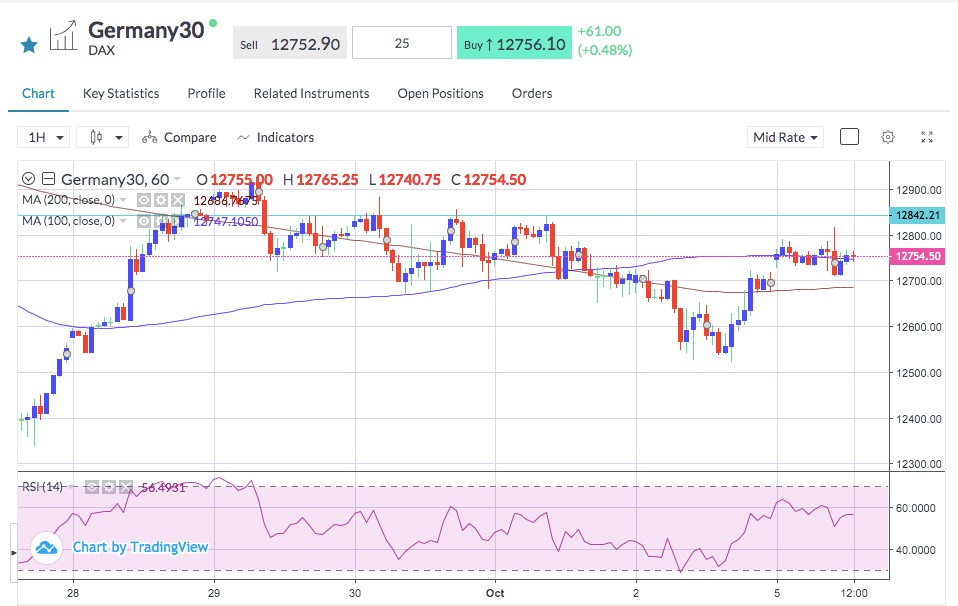

Germany30 has opened with a

bullish gap, the index is up around 0.50%, but it still needs to break above

the 12.840 zone to end the current downtrend.