Since the Saudi Riyal is pegged to the US Dollar, and USD is expected to grow stronger in relation to the Rupee in 2024, the latest SAR to INR forecast is pointing towards new all-time highs in the coming months.

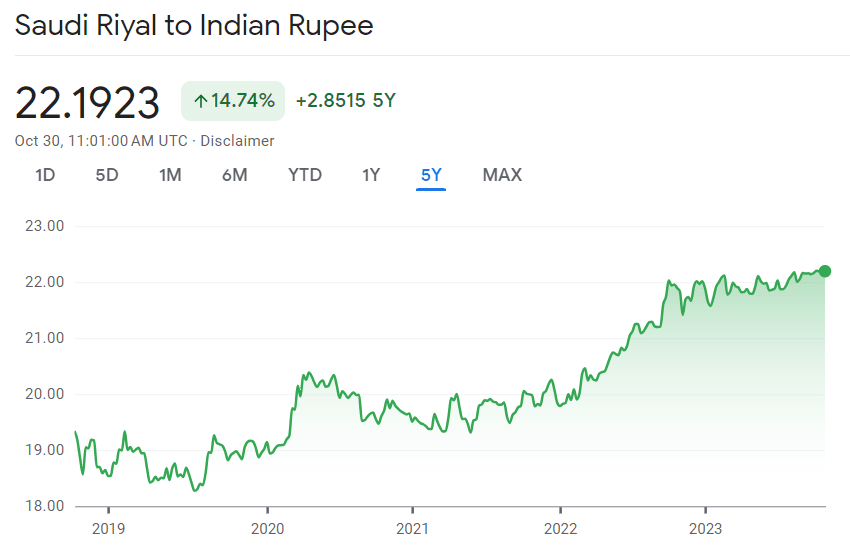

The RBI has continued to maintain the INR at about 83 to the USD and though SAR to INR at 22.13, though against relentless USD pressure, there is a bit of upwards drift appearing now, and there may be a chance of an upside break if the USD does not turn before too long.

The two main drivers for the INR, the policy rate differential and inflation differentials have not changed substantially, though Indian inflation is now headed lower in contrast to US headline inflation, and so that may help support the INR near term.

A strong Dollar due to the Fed hiking the interest rates to curb inflation in the country was counterbalanced by India’s economy outperforming many of its peers in 2023.

Here we look in more detail at what has been driving the rupee price and where it may go next, including the latest SAR to INR forecast for 2024, 2025, and 2030.

SAR to INR Forecast – Summary

- SAR to INR Forecast 2023: With RBI maintaining stability and local economy bucking the global slowdown trend, the SAR to INR is forecast to hold the 22.226 resistance level at least until the end of the year.

- SAR to INR Forecast 2024: Analysts does not expect the RBI to embark on any easing until 2024 and forecast the SAR to INR exchange rate to fluctuate within the 21.86-22.40 range and continue the actual bullish trend.

- SAR to INR Forecast 2025-2030: While some algorithm-based currency pair forecasts SAR to INR remain within a range for several years, other are pointing towards an INR strength to 21.27 by 2025 and 19.35 by 2030.

With CAPEX.com you can trade USD/INR with tight spreads starting at 0.90 pips and 1:20 leverage.

SAR to INR Forecast – Fundamental Outlook: Why India is bucking the global slowdown trend

India is the fastest-growing major economy in 2023. India appears to be doing well, even though others in the region appear to be having difficulties. Although the INR is one of the strongest currencies in the area, inflation is still high but is expected to decline further in the coming year as Indian government bonds are scheduled to be added to global indices.

Economic growth - firming, not stalling

India's second-quarter YoY growth rate was 7.8%, a notable rise from the first quarter's 6.1% growth rate. India's economy is now growing at the fastest rate among the world's major economies; this year, growth is predicted to exceed 7%.

India is seeing rapid economic growth, while the rest of the Asia Pacific area is generally experiencing slower growth. The recent downturn in both China and the West, together with the weakness in the global semiconductor industry—which is a key generator of growth for many regional economies—are the main causes of this.

Growth is mostly being driven by capital investment, which comes from domestic demand. It is expected that investment would boost India's potential for non-inflationary growth, which bodes well for the nation's future development. Weaker imports have partially offset falling exports, even though net exports aren't helping much.

The robust performance of household spending can be attributed to various factors such as the improving job market, decreasing rates of unemployment, rising labor participation, and decreasing rates of inflation. As we will explain in a moment, government expenditure indirectly promotes growth even though it does not directly cause it. This is achieved through targeted spending.

Budget deficit reduction is mindful of growth

The Union budget for this year aimed to reduce the deficit to 5.9% of GDP from 6.4% in the fiscal year ending in March 2023, which some have referred to as an "unambitious" goal.

This budget could be better described as "growth-oriented," with several capital spending measures meant to bolster India's infrastructure and the apparent goal of "crowding in" private enterprise expenditure. The GDP looks to be doing well in that area based on how it has performed so far this year.

India is rated BBB for sovereign credit, which puts it just below investment grade and exposes the bond market to the risk of a downgrade. The recent announcement that international bond indices will soon incorporate Indian government bonds seems to allay those anxieties.

In terms of India's attempts to gradually reduce the deficit and its debt-to-GDP ratio, it seems that this year will go roughly as planned, if not slightly ahead of schedule.

To fulfill the 5.9% deficit ratio, India's cumulative deficit must reach about INR 16.9 trillion by March of the following year, assuming real GDP growth of roughly 7% and average inflation of roughly 4%, as predicted by ING. Since the monthly deficit figures have so far remained close to the projected “on target” track required to achieve this, there doesn't seem to be much risk of any credit downgrades, even though the debt-to-GDP ratio is still high and is expected to moderate to roughly 81.5% by the end of this fiscal year, down from 83.8% last year.

External balance and the INR

One of the biggest surprises of the year has been the rupee's perseverance. Since October 2022, the INR's sole movements against the USD have been between approximately 80.5 and 83.0. The range has been approaching 82.5 in the past few months. The INR is currently the third best-performing currency in the APAC area year to date when compared to other rivals in the foreign exchange market, such as the Chinese yuan, which is 5.84% weaker than the USD, and the Japanese yen, which is 11% weaker against the USD. This outperformance is noteworthy.

Stable INR thanks to the RBI

Even if India's economy has outperformed many of its peers, the favorable spread of policy rates over US rates is clearly advantageous, but we do not entirely credit this FX performance to structural concerns. Instead, we think that the main factor behind the currency's year-round stability has been the Reserve Bank of India's (RBI) intervention. To maintain a relatively stable real exchange rate, the INR frequently monitors variations in inflation.

During certain times this year, Indian inflation has been lower than US inflation, which may have been brought on by a higher rupee. Except for a brief period, a few months ago, Indian inflation has increased rapidly in recent years. In the meantime, US inflation has leveled off at a little over 3%, casting doubt on INR's stability.

Considering this, the RBI seems to have a wide range of choices should it decide to keep bolstering the INR. Not only has import cover increased recently, but it remains significantly greater than the six months that are often thought to be the minimum requirement for emerging market economies.

The trade balance has deteriorated

This high FX reserve position has nothing to do with the trade sector, which is currently facing a deficit (though not a very large one by historical standards; the current account deficit is only about 2% of GDP).

Like everything else in the region, India's exports have decreased from their peak in 2021, but the decline has been quite gradual, and India may have benefited from two factors. First, India's direct trade with China is much more constrained than it is for the most part of the rest of Asia. The other is that India is still a minor role in the semiconductor business, despite having been hit particularly hard this year and only now starting to recover.

However, when it comes to exports to the rest of the area, India does poorly overall and ranks quite low when it comes to relative yearly growth rates. This appears to be influenced by two primary causes. The first is that jewelry exports, which are usually strong, have been quite sluggish this year. This accounted for almost 8.5% of all exports in 2022, which is a substantial amount of India's export portfolio. This is one area where slow Chinese demand may be having an excessive impact, as China is one of the largest markets for Indian jewelry after the US, where demand has also been negatively impacted by rising inflation rates.

The second is export limitations on agricultural products. On July 20, exports of non-basmati rice were forbidden. This occurred when it was forbidden to eat broken white rice the year before. Following the restriction on sugar exports to 6.1 million tonnes this season, exports of the commodity following the end of the current export season on September 30 will exacerbate the export downturn. Sugar exports have already all but stopped.

Government bonds being added to international indices to offer further support

Along with a consistent influx of foreign direct investment, the category "other investment" makes up the majority of India's financial account inflow. This category, which is mostly made up of American and global deposit receipts (ADRs and GDRs), shows that foreign exchange revenues from overseas stock listings have been a consistent source of income over the last 18 months.

The projected increase in volatility has been seen in portfolio flows; nonetheless, direct and "other" investments ought to be rather stable. This is comforting when the trade picture looks threatened, and a currency is arbitrarily held back from where the market would want to see it for a while.

JP Morgan's recent announcement that it will begin including Indian government bonds in its Emerging Market Bond Index on June 28, 2023, may promote future portfolio inflows. This transfer has been highly awaited after being postponed numerous times in past years. Estimates vary, but it is thought that this will undoubtedly attract substantial foreign capital inflows into Indian government bonds, with inflows anticipated to be between $25 and $40 billion.

It remains to be seen if other companies, like the FTSE Russell, will be motivated to follow JP Morgan's lead. In any event, in addition to strengthening the INR, the measure should aid in lowering corporate bond rates and the difference between government bonds and US Treasuries.

However, analysts anticipate that the INR will eventually resume its trend of nominal depreciation at a rate of about 2% annually in line with maintaining a stable real exchange rate, given that US inflation is expected to decline over the next year and Indian inflation is expected to stabilize at a level between 4.5% and 5.5%. This will follow the immediate gain from a change in market expectations that the US Federal Reserve will further ease interest rates in 2024 and 2025.

Analysts forecast USD to INR has some downside potential (INR appreciation) when the USD finally does turn weaker is more limited than some other currencies, as the currency is currently only supported in a narrow range and has not seen the same level of depreciation as other regional currencies. If this turn ever materializes, they expect to see the Australian Dollar and Korean won doing better.

Inflation and the Reserve Bank of India

Indian inflation looked to be between the RBI's target range of 2 and 6% before the year ended, indicating that policy rates might be eased. However erratic monsoons have had a significant negative influence on agriculture, increasing the price of seasonal foods. Consequently, even if inflation is already beginning to drop, it has surged above the RBI's target once more.

For the second half of the year, analysts predict inflation to continue falling as the government shields citizens from growing energy costs. The numbers for October will be released, and as early as next month, inflation might go back inside the target range.

This will keep real rates high and provide a strong justification for a rate reduction in the first half of 2024. The INR is supported by the fact that India's policy rate, at 6.5%, is 100 basis points lower than the US rate. That spread is larger than that of some of its Asian peers. The largest risk to the projection of US rates and the sustainability of the USD's strength is the US economy's persistent defiance of logic in failing to slow down. This is why the most recent SAR to INR prediction is a little bit optimistic.

SAR to INR Forecast – The Latest Calls for Central Banks

Central bank rates are reaching their peak globally, and we're already starting to see rate cuts in certain regions. Since the Saudi Arabian Riyal is pegged to the US Dollar (1 AED = 0.272257 USD) like the UAE Dirham (see also AED to INR forecast), the FED policy expectations will highly influence the AED to INR forecast. Here's what investment banks expect from policymakers from US and India over the next few months.

Federal Reserve

- Expectations: No further rate hikes with cuts starting from Spring 2024

- Rationale: The Federal Reserve continues to raise the likelihood of another rate hike this year, citing the high rate of inflation, tight labor markets, and surprisingly robust economic growth. But things will only become worse when real household discretionary income starts to stagnate concurrently with the start of student loan repayments, the tightening lending market, and the depletion of many people's pandemic reserves. Important measures of inflation are thankfully beginning to moderate. For example, the core personal consumption expenditure deflator has recorded three months in a row where month-over-month prints have been less than 0.2%. This pattern suggests that the Fed will be able to respond swiftly when the economy slows down in 2024.

- Risk: Due to a tight labour market and ongoing strong US consumer spending, inflation may stay high for an extended period. This is especially true if unions can negotiate salary agreements that outpace inflation and set the standard for larger compensation packages. The Fed is unlikely to wait to raise rates further in this situation. Alternatively, if the financial crisis resurfaces in the banking sector, most likely via the commercial real estate market, lending standards will become considerably more stringent, and the Fed might be compelled to lower interest rates more aggressively.

Reserve Bank of India

- Expectations: No further changes to the repo rate this year. Rate cuts start in the first quarter of 2024.

- Rationale: The Reserve Bank of India (RBI) has one of the strongest policy rates in the region when compared to the US Federal Reserve funds rate and to its own internal inflation rate, which is currently declining following a few recent spikes in food prices. Strong macro momentum, as evidenced by the GDP growing at one of the highest rates in the world in the second quarter of this year—7.8%—and the RBI's apparent ability to maintain a stable INR at roughly 83 to the USD and 22.133 to the SAR is likely what is preventing the RBI from easing earlier.

- Risk: There is room for the RBI to move earlier than we are suggesting, but they may prefer to wait for the US to start easing before they move themselves.

SAR to INR Forecast – Technical Outlook: Loses Momentum Above the Key Support Level

The SAR to INR upward bias remains intact as the pair holds above the key 100- and 200-day Exponential Moving Averages (EMA) on the daily chart. The immediate upside barrier to watch is seen at 22.20.

Further north, this all-time high around 22.20 will be the next resistance, followed by 22.392, a psychological round mark at 84.00 for the USD to INR pair. On the downside, a breach of the 22.20 mark could drag the pair towards 22.059 (low of September 11 and 22), towards the 21.96 swing low and 100-200 days moving averages.

From a technical perspective, the SAR to INR forecast points toward a more likely break of the tight consolidation to new all-time highs in 2024.

SAR to INR Forecast – Institutional and AI-Algorithms Price Predictions 2024, 2025, 2030

Below is the updated data of the SAR to INR forecasts as of April 2024. It either can be altered or can be proved to be wrong as it is based on essential factors like interest rates and central bank policy, in line with market assumptions. It is important to research and analyze keeping in mind that past displays do not assure future outcomes.

SAR to INR Forecast by CareEdge Ratings: RBI to Keep Rupee Range Bound against the Dollar

As crude oil prices are expected to stay elevated in the near term, CareEdge revised their projections for India’s current account deficit (CAD) by 20bps to 1.8% of GDP in FY24 from 1.6% projected earlier. This is still lower than CAD of 2% in FY23.

Their projection assumes the Indian crude oil basket would average USD 87 per barrel in FY24 versus USD 85 per barrel assumed earlier. India’s net foreign direct investment (FDI) inflows have fallen to ~USD 5 billion in Q1FY24 from ~USD 13.4 billion in Q1FY23.

They expect FDI flows to moderate in FY24, as businesses delay investments amidst a global slowdown. Elevated UST yields and a strong Dollar Index are weighing on foreign portfolio investments (FPI). India’s net FPI inflows fell to USD 2.2 billion in August from USD 5.8 billion in July and a peak of USD 6.9 billion in June.

September has seen net FPI outflows of USD 0.5 billion so far. We expect FPI flows to gain momentum once the Fed signals that interest rates have peaked. They maintain the initial view that India will witness net FPI inflows in FY24 as UST yields moderate eventually and as India benefits from favorable growth differentials arising from being the fastest-growing major economy.

In the last two MPC meetings, RBI has emphasized its commitment to bring inflation to its 4% target. Hence, we expect RBI to intervene to contain rupee volatility and imported inflation. India has adequate forex reserves, equivalent to an import cover of ~11 months, to support RBI intervention. Further, RBI’s forward book position looks comfortable at net purchases of USD 19.5 billion as of July 2023.

Elevated UST yields, weak yuan, and crude oil prices are expected to weigh on the rupee in the near term. Thereafter, some moderation in UST yields and crude oil prices should offer support.

In the coming second half of the fiscal year 2023-24, they forecast USD to INR exchange rate to fluctuate within the range of 82 to 84, gradually gravitating toward the lower boundary of this range. This projection marks a shift from their previous forecast of 81 to 83.

However, the agency forecasted SAR to INR to trade within the 21.866-22.40 range within the next 6 months.

SAR to INR Forecast by ING

Analysts forecast USD to INR has some downside potential (INR appreciation) when the USD finally does turn weaker is more limited than some other currencies, as the currency is currently only supported in a narrow range and has not seen the same level of depreciation as other regional currencies.

As a result, the ING's SAR to INR forecast for the beginning of 2024 is 22.00. The SAR to INR forecast for the next 12 months is 22.052.

AED to INR Forecast by Trading Economics

Trading Economics forecasts SAR to INR to be priced at 22.31 by the end of 2023 and at 22.75 in one year, according to its global macro model's projections and analysts' expectations.

AED to INR Forecast by Wallet Investor

Wallet Investor forecast SAR to INR to close 2023 at 22.25 and expects a Riyal appreciation during the next year.

The 2024 SAR to INR price prediction towards an all-time high of 23.53, and a closing rate of 23.31. The 2025 SAR to INR forecast is showing a potential maximum rate of 24.60 and a closing rate of 24.477. However, SAR to INR forecast is a trading range within the 21.86-22.40 levels.

AED to INR Forecast 2025 by AI Pickup

The Artificial Intelligence (AI) Pickup algorithm supports the statement that the strength of the prevailing trend and the live inflationary climate will continue to weaken the rupee in a long-term forecast until 2027. The AI algorithms AED to INR forecast 2025 points towards an advance up to 24.28.

Summary of AED to INR Forecast

- The Indian Rupee has recently breached the 83-level against the US Dollar and 22.297 against the AED, but its decline has been curtailed by interventions by the Reserve Bank of India (RBI) across various markets, including the spot, Non-Deliverable Forward (NDF), and futures markets.

- In the coming second half of the fiscal year 2023-24, most institutions and AI-algorithms forecast the USD to INR exchange rate to fluctuate within the range of 82 to 84, gradually gravitating toward the lower boundary of this range. Though, AED to INR forecast is a trading range within the 22.325-22.87 levels.