Oil market sentiment turned decidedly bearish in Q4 2023 as non-OPEC+ supply strength coincided with slowing global oil demand growth. The outlook for the oil market largely depends on OPEC+ policy which continues to hold a large amount of supply from the market to support prices. It will continue this year, despite the clear risks? Here are the latest Oil forecasts and price predictions for 2024.

The extension of OPEC+ output cuts through 1Q24 did little to prop up oil prices. By early December, they had tumbled almost 40% from September’s highs to their lowest levels in six months, $68/bbl for WTI and $73 for Brent.

As mentioned in our Oil forecast and price prediction update for Q4, October and November have historically been the weakest months of the year for crude oil over the past 44 years, with December only providing modest gains. Seasonal patterns could provide some headwinds in Q4 or prompt some bulls to book profits or scale back bullish bets as we near the year-end.

Although the prices bounced from the lows of the year, analysts forecast tighter oil markets in the first half of 2024, amid a looming surplus at the beginning of the year, driven by seasonally weaker demand. The second half of 2024 should see the market return to deficit, which suggests prices moving higher in 2H24.

Oil Forecast & Price Predictions – Summary

- Oil price prediction Q4 2023: Despite the announced cuts, analysts lowered their forecast for the oil prices in 2024. ICE Brent is forecasted to remain trading in the low $80s in the early part of 2024, while WTI in the low $75s.

- Oil price prediction 2024: While EIA and investment banks revised down their Oil forecast with 5-10 percent (see the updated Oil price predictions below), World Bank and Fitch Ratings warns that, due to supply restrictions and a regional conflict, an oil price shock of 120/bbl in 2024 would hit growth and boost Inflation.

- Oil price prediction for the next 5 years and beyond: some expect demand for fossil fuels could fall in the medium-to-long-term, leading to a lower oil price in 5-10 years’ time. EIA expects the average Brent crude prices at $61/bbl in 2025 and $73/bbl in 2030.

With CAPEX.com you can trade WTI Crude Oil and Brent Oil futures through CFDs if you want to speculate on price movements and trade or invest in Oil stocks and Oil ETFs.

Crude Oil Forecast 2024 - Tighter oil market in the second half

The market was worried about an impending surplus in 2024 heading into the first quarter of the following year due to seasonally lower demand. OPEC+, however, moved to eliminate this anticipated surplus at their most recent meeting. While a few other members have announced their own additional voluntary supply cutbacks, Saudi Arabia and Russia have decided to extend their voluntary supply restrictions till the end of 1Q24. These reductions total a little less than 2.2MMbbls/d. 900 million barrels per day is the real quantity included in the new further reduction, nevertheless.

This supply reduction should be sufficient to eliminate the excess in 1Q24 and cause a slight shortage in the market at the beginning of 2024. Even yet, our balance for 2Q24 indicates a slight excess, indicating that the market is roughly balanced for the first half of 24. This may and probably will vary based on how OPEC+ countries proceed with rolling back these voluntary cuts.

Given that balanced market, Oil prices are forecasted to remain at the 2023 low levels in the early part of 2024 and move higher in the second half of 2024 when the market should return to deficit.

OPEC+ policy is key

To bolster the market, OPEC+ has been quite active during the past 12 months. The voluntary cuts we are witnessing from the Kingdom demonstrate that Saudi Arabia has taken the lead in advocating for severe cuts. Saudi Arabia is eager to make sure that oil prices stay primarily above this level because their fiscal breakeven point is just above US$80/bbl.

Given that US production growth is reportedly decreasing, OPEC+ feels more confident about reducing supply without running the danger of losing market share. Although US supply growth surprised to the upside in 2023, it is forecasted to decline significantly the 2024, indicating that the Saudis will likely continue to withhold supply from the market.

Nonetheless, a few significant problems within OPEC+ have come to light since the most recent conference. First off, a few members—Angola in particular—have already declared they will reject their 2024 output limit and are not happy with it. From a supply perspective, though, this is not going to make much of a difference given the pressure we have seen on Angolan output.

The inability of OPEC+ to reach a consensus on cuts for the entire group ought to be a greater cause for concern. Rather, we are witnessing the voluntary resignation of a few members. It is obvious that certain members are finding it harder and harder to take any further cuts considering the extent of the group's current reduction.

Furthermore, considering the extent of the reduction we are witnessing, OPEC has a sizable amount of excess capacity. OPEC has about 5.5MMbbls/d of spare capacity if Iran is included. And considering the most recent reductions that have been revealed, this will only rise over Q24. About 58% of this belongs to Saudi Arabia. Given that one would anticipate this capacity to begin to re-enter the market should we witness major price strength, this spare capacity should also provide some confidence to markets.

Sanction risk

Next year's market is highly susceptible to supply risk due to sanctions. And this is especially true for Venezuela and Iran. In recent months, the US also seems to have tightened its enforcement of the G-7 price cap on Russian oil.

Iran's supply has grown dramatically in 2023, going from roughly 2.5MMbbls/d at the start of the year to roughly 3.1MMbbls/d now. Notwithstanding the continued imposition of US sanctions on the nation, this has occurred. Since Russia invaded Ukraine, the US has been worried about the market's high prices and supply problems and seems to be softening its stance against Iran.

But given the recent developments in Israel and the potential for Iranian involvement, there's a chance that the US may begin to impose sanctions with greater rigour in the future. If this occurred, supply loss might exceed 500 million barrels per day. We now project Iranian flows to stay at approximately 3.1 million barrels per day in 2024.

Regarding Venezuela, the United States has loosened oil sanctions in exchange for more equitable national elections the next year. If this doesn't work out, though, it's possible that sanctions against Venezuela will be reinstated. 200 million barrels per day would be the supply at danger.

The US Treasury has also been more aggressive in recent months in imposing sanctions on shipping companies that have carried Russian oil above the $60/bbl price ceiling. Given the potential sanctions risk they would encounter should the price of the oil turn out to be more than US$60/bbl, this action may completely discourage Western shipping companies from delivering Russian oil. Therefore, employing Western shipping services to carry Russian oil may become more difficult starting in the upcoming year. However, Russia has managed to circumvent the G-7 pricing cap by amassing a sizable fleet of its own tankers.

Global Oil supply forecast 2024

The global oil industry is being significantly impacted by the change in the world's oil supply from major Middle Eastern producers to the United States and other countries in the Atlantic Basin, as well as by China's growing petrochemical industry and its leading influence on global oil consumption.

Following the invasion of Ukraine, most Russian flows were already absorbed by markets east of Suez, along with increased Iranian exports. However, these markets now need to respond to rising volumes of NGLs and oil from the Atlantic Basin. The ongoing increase in production coupled with the deceleration of demand growth will provide challenges for major producers seeking to protect their market share and sustain high oil prices.

US oil supply growth has surprised to the upside in 2023, with it estimated to grow by 1MMbbls/d to a record high of 12.9MMbbls/d. However, drilling activity in the US has slowed significantly this year, which suggests that the US will see more modest supply growth in 2024, with it forecast to grow by 250Mbbls/d to 13.15MMbbls/d. A focus on shareholder returns, cost inflation, tighter credit conditions, and increased consolidation within the industry are some of the factors holding back drilling activity.

Growth in global crude oil supply has been limited in 2023 because of voluntary production cuts from Saudi Arabia and reduced production targets from other OPEC+ countries. We estimate countries within the OPEC+ agreement have lowered crude oil production by 1.4 million b/d in 2023, partly offsetting production growth of 2.4 million b/d by non-OPEC+ producers.

We forecast OPEC+ crude oil production to fall by an additional 0.6 million b/d on average in 2024. This forecast assumes some voluntary production cuts from Saudi Arabia will be extended through 2024 and overall production from OPEC+ countries will remain below targets.

Global Oil Demand Forecast 2024

There is plenty of uncertainty over oil demand in 2024, given the uncertainty over the macro picture next year. The Organization of the Petroleum-Exporting Countries (OPEC) and the IEA, which represents industrialized countries, have clashed in recent years over issues such as the long-term oil demand outlook and the need for investment in new supplies.

According to the latest IEA Oil Market Report, global oil demand growth is forecasted to rise by 1.1 million barrels per day(bpd) in 2024 up 130,000 bpd from its previous forecast, citing an improvement in the outlook for the United States and lower oil prices.

By contrast, in its latest report, OPEC stuck to its forecast that demand will rise by 2.25 million bpd in 2024. The difference between the two forecasts - 1.15 million bpd - is equivalent to around 1% of daily world oil use.

At the same time, EIA forecasted global oil demand to grow by 1.3 million b/d in 2024, down from 1.8 million b/d in 2023 as GDP growth stays below trend in major economies. Efficiency improvements and a booming electric vehicle fleet also drag on demand. Asia, and China in particular, is predicted to account for most of the demand growth in the upcoming year. Next year, the nation is anticipated to supply more than 60% of the increase in oil consumption. On the other hand, because to slower economic development, demand is predicted to slightly fall in Europe and the Americas next year.

Oil analysts at Standard Chartered Bank forecast that the world's key oil demand centers of China and India will see a marked slowdown next year, underpinning a global fall in oil demand growth. Standard Chartered forecasts that Asia-Pacific region oil demand will grow by 952,000 b/d in 2024, slower than 2023's 1.26 million b/d growth but close to the average for the five years before the pandemic of 949,000 b/d.

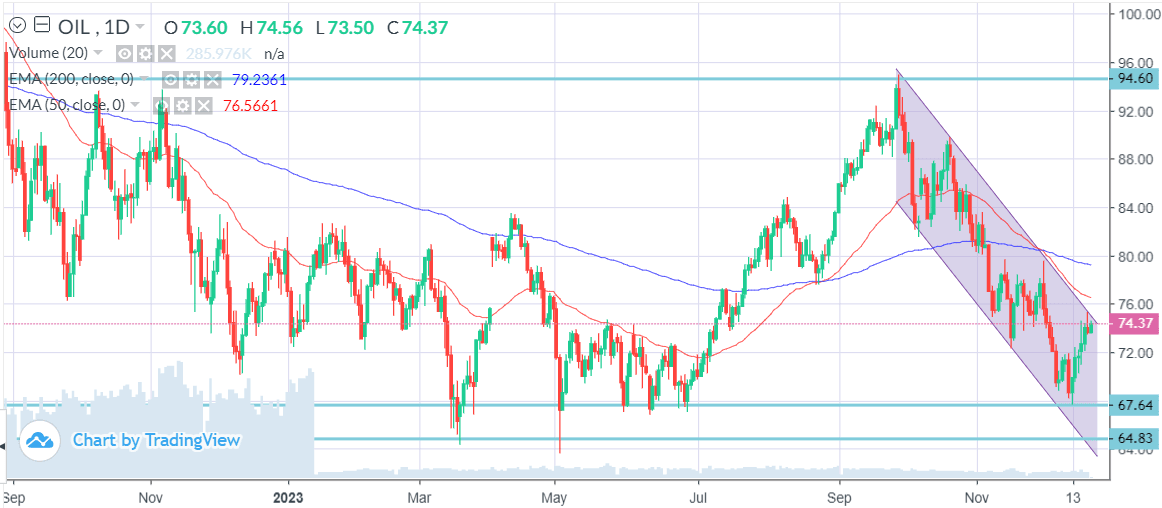

Technical Oil Prices Forecast Q4 2023 - How High Can It Go?

The price of brent and WTI crude oil continues to trade within a broad range on the long term and descendent channel on the medium term.

Range traders might consider looking for long entry on a bullish price reversal above the support level, targeting a move to initial resistance. In this scenario, a close below the reversal low might be used as a stop loss indication. A weekly close above the resistance area, would suggest a further upside resistance target.

A bullish price reversal above the long-term support level (2023 lows) should be signalled by a breakout of the medium-term channel resistance. However, a failure at this level will signal the price may trade below the 2023 lows.

BRENT Oil Technical Analysis and Price Forecast

- The support level of this long-term range is considered at the 71.00 level, while long term resistance is considered at the 94.00-95.00 level.

- The short-term dynamic resistance is at 80. A break above it signals an upside continuation within the trading range toward 94.00-95.00

- A failure signals a retest of the 71.00 support area and a more likely continuation within the descendent channel.

WTI Oil Technical Analysis and Price Forecast

- The support level of this long-term range is considered at the 65.00-67.00 level, while long term resistance is considered at the 94 level.

- The short-term dynamic resistance is at 75. A break above it signals an upside continuation within the trading range toward 94.00.

- A failure signals a retest of the 65.00-67.00 support area and a more likely continuation within the descendent channel.

To learn more about technical analysis as a forecasting tool visit CAPEX Academy.

Oil Brands

When talking about the commodity oil traded on the financial markets, we can distinguish two types. The most popular, and also the most traded, is the American oil called WTI. The other popular variant is Brent.

West Texas Intermediate (WTI)

Light sweet crude oil (WTI) is widely used in US refineries and is an important benchmark for oil prices. WTI is a light oil with a high API density and low sulfur content. This determines the density of the oil in relation to water. WTI oil is widely traded between oil companies and investors. Most trading is done through futures through CME Group. The Light Sweet Crude Oil (CL) future is one of the most traded futures worldwide.

Most of the oil of this type is stored in Cushing, an important hub for Oklahoma's oil industry. Here are large storage tanks connected to pipelines that transport the oil to all United States regions. WTI is an important feedstock for refineries in the Midwestern United States and on the coast of the Gulf of Mexico.

Brent Crude Oil

Brent oil is an important benchmark for the petroleum rate, especially in Europe, Africa, and the Middle East. Its name is derived from the Brent oil field in the North Sea. This Royal Dutch Shell oil field was once one of Britain's most productive oil fields, but most of the platforms there have since been decommissioned.

The correlation between these two futures' price development is high, and we have seen several times in recent years that Brent's price was more than $10 higher than usual. At the end of 2020, the difference was approximately $3. Such differences are caused, among other things, by supply and demand, including the costs of shipping or storing oil.

Oil Price Prediction for 2024, 2025-2030

The WTI and Brent crude oil prices are forecasted to stagnate in the first part of the year and increase in the second part of 2024, reflecting EIA's and IEA's expectations of tightening balances in global oil markets. With new developments in the past weeks, what are the latest crude oil price predictions?

Here are the most important oil price predictions released by some of the most influential financial institutions in the world today.

EIA revises down crude oil price forecasts for 2024

In the last Short-Term Energy Outlook (STEO) of 2023, the US Energy Information Administration (EIA) forecasts the Brent crude oil spot price will increase to an average of $84/bbl in first-half 2024 from an average of $78/bbl in December 2023, partly driven by recently announced OPEC+ production cuts.

Nevertheless, despite the announced cuts, EIA lowers its forecast for the Brent price in 2024. EIA forecast the Brent spot price will average $83/bbl next year, a decrease from the previous Oil price forecast of $93/bbl.

Goldman Sachs lowers its 2024 oil price forecast by 12% due to bumper US output

The Wall Street bank said recently that it now expects Brent, the global oil benchmark, to average $81 a barrel in 2024, down from its previous estimate of $92 a barrel. It forecasts Brent Oil to peak at $85 a barrel next June.

The bank’s analysts said “the key reason” for the revised price expectations was “ongoing gains in drilling speed and well completion intensity” in the United States. Goldman Sachs said, the supply cuts by OPEC+, a potential economic rebound in China, as well as a “modest” risk of a US recession, among other factors, are likely to limit the extent of falls in oil prices.

Barclays lowers 2024 Brent oil price forecast to $93/b on demand concerns

Barclays lowered its oil price forecast for Brent crude futures for 2024 by $4/b to $93/b but noted that the recent selloff in global oil prices may be overdone. Lingering concerns over the health of the global economy were supported this week by data showing a surprise spike in US oil stocks and economic weakness in top crude importer China, Barclays said in a late 2023 note.

Barclays lowered their 2024 Brent forecast by $4/b but maintain their above-curve and consensus view on prices. They've also noted that its Brent price forecast for 2024 remains $14/b ahead of the Brent forward curve.

Oil price could reach $150 a barrel in 2024, warns World Bank

The World Bank has warned that if the Israel-Hamas battle turns into a regional conflict, oil prices might rise to $150 in 2024. The Israel-Hamas war has had a limited effect on oil prices so far. However, an escalation of the current conflict could shrink global oil supply by as much as eight million barrels per day, leading to sharp price increases, said World Bank.

This disruption in the oil supply would be like the one that resulted in the loss of around 7.5% of the world's oil supplies during the Arab oil disruption of 1973. However, the World Bank notes that countries are better suited to deal with an oil supply shock now than they were in 1973.

ING forecast rising Oil price in the second half of 2024

The supply cuts should be enough to remove the surplus in 1Q24 and leave the market in a small deficit early next year, said ING. However, their balance still shows a small surplus in 2Q24, which means that the market is largely balanced over 1H24. This could and will likely change depending on how OPEC+ members go about unwinding these voluntary cuts.

Given that balanced market, ING forecast Oil Brent to remain trading in the low $80s in the early part of next year. The second half of 2024 will see the market return to deficit, which suggests we see prices moving higher in 2H24. Though, the Dutch Bank forecast Brent Oil to average US$91/bbl over the last six months of 2024.

Citi forecast Brent crude oil prices to $73 / bbl in Q2 2024

Citigroup's Brent oil forecasts for 2024 points toward $73/bbl price for Brent by Q2 2024 and $68/bbl by the end of the year. Citi do warn though that there is potential for explosive price gains should there be a polar vortex or geopolitical upheaval. However, they see a low risk for a potential widening of the war in the Middle East.

Citi believes that supply will outpace demand by an average 1.4 million b/d in 2024 citing contributions from non-OPEC supply from Argentina, Brazil, Canada, Guyana and the U.S.

JPMorgan forecasts crude will average $83 a barrel in 2024

After falling in 2023, J.P. Morgan Research forecasts Brent oil prices to remain largely flat in 2024 and edge down a further 10% in 2025: “Our Brent Oil forecast has not changed since June and is expected to average $83 per barrel (bbl) in 2024”.

This will be buttressed by solid supply-demand fundamentals: “Despite sustained economic headwinds, we see oil demand rising by 1.6 million barrels per day (mbd) in 2024, underpinned by robust emerging markets, a resilient U.S. and a weak but stable Europe.”

Fitch Ratings forecast an oil price shock would hit 2024 growth and boost inflation

Fitch’s Global Economic Outlook (GEO) forecast oil prices will average USD75 a barrel (bbl) and USD70/bbl in 2024 and 2025, respectively. Using simulations from the Oxford Economics Global Economic Model, they estimated the impact of higher oil prices throughout 2024-2025 on their baseline GEO growth and inflation forecasts.

Their scenario assumes that, due to supply restrictions, oil prices average USD120/bbl in 2024 and USD100/bbl in 2025. Higher oil prices would dampen GDP growth in almost all the GEO’s ‘Fitch 20’ economies, although the impact would largely dissipate in 2025. The absence of a significant growth rebound in 2025 implies a longer lasting, if generally moderate, impact on GDP levels in most countries, which could affect assessments of potential growth.

Algorithm-based (AI) Oil Price Forecasts

Crude oil is expected to trade at 71.74 USD/BBL by the end of this quarter, according to Trading Economics global macro models and analysts' expectations. Looking forward, they estimate it to trade at 72.69 in 12 months' time.

Brent crude oil is expected to trade at 77.09 USD/BBL by the end of this quarter, according to Trading Economics global macro models and analysts' expectations. Looking forward, they estimate it to trade at 78.05 in 12 months' time.

Long Forecast expects Brent Oil to close 2024 at 82.96 with a maximum of 90.79 in July, while WTI to close 2024 at 74.08 with a maximum price of 82.97 in July.

Wallet Investors forecast Brent Oil to close 2023 at $89.6 with a maximum price of $90.56 in November, while WTI to close at $85 with a maximum price of $86.70 in November.

Oil Price Forecast for the Next 5 Years and Beyond (2025 – 2050)

Some expect demand for fossil fuels could fall in the medium-to-long term, leading to a lower oil price in 10 years’ time. Consequently, the oil price in 2030 is widely expected below $100/bbl.

According to EIA’s annual energy outlook report, the agency held a conservative outlook for its oil price forecast for 2030. It expects the average Brent crude prices at $61/bbl in 2025, $73/bbl in 2030, $80/bbl in 2035, $87/bbl in 2040, $91/bbl in 2045 and $95/bbl in 2050.

Energy consultancy Wood Mackenzie said if global fuel consumption falls in line with the emission targets set to limit global warming, oil price projections in 2030 could fall as low as $40/bbl.

Wallet Investor forecast WTI Oil to trade at $102 at the end of 2025, while the Brent Oil price prediction 2025 is $112.

The Oil price prediction for 2025 at Long Forecast is: WTI 74.35, Brent 83.67.

The Oil price forecast for the next 5 years is 100.75 for WTI and 131.53 for Brent according to Long Forecast and $136 for WTI and $146 for Brent according to Wallet Investor.

When looking for oil-price predictions, it's important to remember that analysts' forecasts may be wrong. This is because their projections are based on a fundamental and technical study of WTI and Brent oil commodities’ historical price movements. But past performance and forecast are not reliable indicators of future results.

It is essential to do your research and always remember your decision to trade depends on your attitude to risk, your expertise in the market, the spread of your investment portfolio, and how comfortable you feel about losing money. You should never invest money that you cannot afford to lose.

How Did the Price of Crude Oil Change Over Time?

Below is a chart showing the price for West Texas Intermediate (NYMEX) Crude Oil over the last 5 years. The shown prices are in U.S. dollars. On the chart, you can clearly see the monstrous drop that happened earlier this year, and how the price has been going up and stabilizing in the months thereafter.

A Recent History of Oil

At the end of April 2020 (due to the Saudi and Russia conflict - more on that later), the oil price crashed, and the May WTI future even dipped below $0. The stock markets recovered strongly during the summer, and the oil price had also found its way up again. In August, the oil price rose well above $ 40 a barrel. With that price, the largest oil companies got some air also, but it is still far from enough for most to make a profit.

At the beginning of September, the oil price had suddenly fallen hard again. Simultaneously, with the mini-crash with the US stock markets, a crude oil barrel's worth dropped by about 15% to below $37 a barrel. This brought the oil price back below $40 a barrel for the first time since July. The drop is partly because Saudi Arabia had lowered its sales prices for October and the fear that the number of COVID-19 infections will increase rapidly in several countries.

The rebound in the number of infections could thwart the global economic recovery and decrease fuel demand. With several refineries lowering tariffs again, it seems they want to prevent oil stocks from rising back to record levels. The oil price was able to recover so strongly in recent months, thanks to the OPEC + countries' agreements regarding the reduction in production. However, due to the crisis, many countries are looking for additional income sources. Therefore, some countries are not fully complying with the agreements made. As a result, more oil flows into the market, which also has a depressing effect on oil prices.

March 9th, 2020: 30% Oil Price Crash

Monday, March 9th, can go into the history books as "Black Monday" for the oil price. Negotiations between Saudi Arabia and Russia had come to nothing.

The oil price was under pressure in previous months due to the spread of the coronavirus. The world economy was on the back burner, and as a result, the oil demand had declined considerably. By limiting oil production, the countries that are part of the oil cartel hoped to stabilize or increase the price themselves. Saudi Arabia, in particular, is strongly in favor of limiting oil production.

Saudi Arabia was now trying to force Russia in another way to join the OPEC plan. The Saudi’s were going to increase production considerably and flood the market with oil. As a result, the price of a crude oil barrel had opened more than 30% lower, the lowest price since 2016. A low oil price is disastrous for most countries. Most OPEC countries are almost entirely dependent on oil revenues.

America's shale farmers may be hit hardest. The shale revolution seems to be built more and more on quicksand, as costs remain high and the new resources that are found have a much shorter lifespan. Even with an oil price of around $60 a barrel, many of these producers were already struggling. The unrest surrounding the coronavirus also makes it difficult to raise external capital. With Saudi Arabia pushing the oil price further down, the situation seems to be untenable for many producers. Players with a fragile balance and relatively high costs are unlikely to make it. What Saudi Arabia failed to achieve in 2016 now seemed to have a good chance of success.

April 21st, 2020: WTI Goes Below Zero

In April 2020, we saw a situation in the oil markets that has never occurred before. The West Texas Intermediate Crude Oil (WTI) futures contract for May fell more than 100%. The price fell during the day and took an unprecedented dive later in the evening to $ -37.63/barrel, meaning that oil producers would indeed have to pay buyers to collect the oil.

This is mainly because the storage capacity in Cushing, Oklahoma is full. And it is precisely there that this oil is delivered. Traders and large companies who were long yesterday but ran out of storage capacity or liquidity to purchase oil were forced to close futures before expiry.

Shale Oil Influence

Oil production increased rapidly, and OPEC was not happy about this. They saw the increase in supply in the Middle East as competition. OPEC, therefore, came up with the idea of fully opening the oil taps. The production costs of shale oil were many times higher. The result was a drop in oil prices from about $110 a barrel to below $30 at the beginning of 2016. OPEC hoped to wipe out shale farmers in this way.

This strategy failed, and the OPEC countries themselves ultimately suffered considerable disadvantages from this strategy. For years they saw their income more than halved. In the meantime, the shale farmers have learned to work cheaper and more efficiently, and they are already profitable at a lower oil price. What’s typical of this form of oil extraction is that production can be increased quickly.

OPEC Influence

Demand for oil will remain stable in the coming years. But it is also apparent that there is a lot of extra supply on the market now that American oil production is rapidly increasing. Shale oil, in particular, is extracted from the ground here. The shale revolution was set in motion in 2014 by the sharp rise in oil prices. This form of oil extraction was therefore profitable, despite the high production costs. Due to the attractive market, the oil companies sprang up like mushrooms.

OPEC is trying to limit production to keep the oil price at a reasonable level. Most countries benefit from a somewhat higher, but in any case, stable, oil price. According to OPEC, the oil industry must invest more than $11,000 billion over the next 20 years. If producers don't do that, there will be a shortage. In principle, shale farmers have already invested enough in recent years to absorb a large part of these shortages.

Furthermore, OPEC states that demand continues to increase despite the emergence of electric cars and the like. OPEC writes that the massive expansion of air travel creates a greater demand for oil than the emergence of alternative energy sources can diminish.

Since the low oil price in 2016, OPEC has been trying to support the low oil price. This is done by agreeing on production restrictions with all countries that are members of OPEC. The agreements do not always go smoothly, as Iran and Iraq do not always adhere to these agreements. On the other hand, the US and other countries continue to produce more and more oil, putting oil prices under pressure for a long time.

Factors That May Affect the Price of Crude Oil

We know that oil is an indispensable raw material in the world and that it is used both as raw material and fuel to make plastics, pharmaceuticals, and many other products. Hence, the demand for oil remains strong, and these industries' health will determine most of the world's oil demand. If demand from these industries increases while production stagnates, it will lead to higher prices for this commodity. Of course, and vice versa, if these industries are in a recession, their oil demand will be lower, so demand will decline. If production remains stable or increases in this case, it will logically lead to a drop in the price of a crude oil barrel.

As you will have understood, it is mainly by analyzing the difference between supply and demand that you will determine how the price or price of crude oil will evolve.

It should also be noted that this analysis is slightly more complex today than it used to be. Until a few years ago, it was pretty easy to understand how these prices would behave. At the time, the US was the largest consumer of crude oil. On the other hand, OPEC was the main supplier to the market in terms of production. But over time and the years, this situation has become more complex and slightly more confusing. One explanation for this phenomenon is that oil drilling technologies have improved greatly and resulted in better supply. Besides, we have seen the emergence of alternative solutions for this production. Finally, new players have also joined, including China, a major oil consumer in the world.

Below we have listed factors that change the supply or demand for oil and thus contribute to the evolution of this commodity's price and price.

1. Production data in barrels per day from OPEC countries

Too much production generally leads to lower oil prices per barrel and vice versa. US crude oil inventory data is published weekly, which also affects WTI.

2. Supply, which is published weekly on the economic calendar.

Big supply also contributes to falling prices, while little supply leads to higher prices.

3. The international geopolitical situation

Conflicts affecting the oil-producing and exporting countries often influence the development of the price per barrel.

4. The value of the US dollar on the currency market.

As a barrel of oil is denominated in dollars, this currency will be weaker, and more oil purchases will be stimulated by holders of other currencies.

Final words

Make sure to create a free demo account on CAPEX.com! CAPEX.com is a useful platform for both novice and expert traders. You will be up to date on interesting updates about crude oil as an investment asset, and the user-friendly interface will come in handy if you decide to trade crude oil or any other commodity.

If you look at the price changes of oil for a while now, you will start to see a pattern, and as an investor, you can respond smartly to this.

If you want to invest in oil, it is a good investment to get in when the oil price is at a certain bottom. Of course, there is no guarantee that oil prices will ever rise as much as in the past. Oil is a limited resource and is probably the most precious material in the world. Investing in commodities is one way to improve your overall investment portfolio.

Other resources

- Gold forecast & price predictions 2024

- EurUsd forecast & price predictions 2024

- Dow Jones forecast & price predictions 2024

- Natural Gas forecast & price predictions 2024

- Turkish Lira forecast & price predictions 2024

- Silver forecast & price predictions 2024

- NASDAQ 100 forecast & price predictions 2024

- British Pound forecast & price predictions 2024

- USD to INR forecast & price predictions 2024