Oil prices surged during the first quarter of 2024 as the supply/demand outlook tightened and global geopolitical concerns intensified, pushing both U.S. and European benchmark crude futures to five-month highs. Will prices continue to surge this year? Here are the latest Oil forecasts and price predictions for 2024.

Crude oil prices continued their upward trajectory in early Q2, as heightened geopolitical tensions coincided with the prospect of a tighter supply-demand balance through the remainder of the year.

Over the first three months of the year, WTI (West Texas Intermediate) futures contract rose by 16.1% closing at $83.20, while Brent crude rose 13%, closing the quarter at $87.50. WTI rose in every month of the first quarter, following three months of declines between October-December 2023.

The United States Oil Fund (USO), an exchange traded fund that tracks the U.S. oil price showed a similar pattern of gains, rising over 18% in the first quarter.

With the above factors bolstering oil prices, it has been a good quarter for the major oil and gas producers. The major energy firms on the S&P 500 are tracked by the Energy Select Sector SPDR Fund (XLE), an exchange traded fund that has returned 14.4% so far this year.

Exxon Mobil Corporation (XOM), up 19.3% year to date, ConocoPhillips (COP), up 12.6%, and Chevron Corporation (CVX), up 7.1%, are its top three holdings.

However, as wholesale petrol prices have risen faster than crude prices, several of the downstream refinery, marketing, and transportation bets have seen the largest gains. Compare the 16% increase in WTI with the 32% quarterly gains for RBOB Gasoline futures. Thus, Marathon Petroleum Corp (MPC) gained 42.5% year-to-date, while Valero Energy Corporation (VLO) climbed 36.3%.

According to the latest crude oil forecast for the next weeks, prices may continue to rise during the second quarter, but they remain subject to the considerable near-term uncertainty.

Oil Forecast & Price Predictions – Summary

- Oil price prediction Q2 2024: Energy analysts tend to agree that oil prices are unlikely to fall back sharply in the coming weeks and months. EIA forecast the Brent crude oil spot price will average $90 per barrel (b) in the second quarter of 2024 (2Q24).

- Oil price prediction 2024: While EIA forecast the Brent crude oil price will average $89 per barrel (b) in 2024, World Bank and Fitch Ratings warns that, due to supply restrictions and a regional conflict, an oil price shock of 120/bbl in 2024 would hit growth and boost Inflation.

- Oil price prediction for the next 5 years and beyond: some expect demand for fossil fuels could fall in the medium-to-long-term, leading to a lower oil price in 5-10 years’ time. EIA expects the average Brent crude prices at $61/bbl in 2025 and $73/bbl in 2030.

With CAPEX.com you can trade WTI Crude Oil and Brent Oil futures through CFDs if you want to speculate on price movements and trade or invest in Oil stocks and Oil ETFs.

Crude Oil Forecast 2024 - OPEC’s cuts to keep prices underpinned

Rising concerns over tightening supply along with the persistent uncertainty in the Middle East continue to support the uptrend in speculative bets on Brent and WTI. China's development is beginning to pick up a little speed, U.S. economic indicators are continuing to beat forecasts, and OPEC's output cuts are scheduled to last until the end of June.

The protracted confrontation between Russia and Ukraine, which shows no obvious signs of resolution, is keeping the geopolitical environment tense. Ukraine keeps defending its borders with help from Western countries.

Middle East tensions are rising because of Israeli bombings that have reached Syria and Lebanon, which could lead to a wider confrontation in the region. Additionally, Iran's long-standing support for local militant organisations exacerbates the already prominent levels of regional unrest.

Not to mention China's territorial aspirations for Taiwan.

Speculative investors are becoming increasingly attracted to these elements. According to data from the Commodities Futures Trading Commission, speculative net long positions—bets on additional rises for crude—have risen to their highest points in five months.

Furthermore, according to Reuters last week, hedge funds were swarming into the market, purchasing top futures contracts for the equivalent of 140 million barrels in the seven days leading up to March 19 – the quickest buying pace since December 2019.

OPEC+ policy is key

The OPEC+ grouping, which consists of the Organisation of Petroleum Exporting Countries and its allies, has decided to prolong its production restrictions of 2.2 million barrels per day (BPD). Of course, Saudi Arabia is the group's main power. Its voluntary one million BPD portion of the cuts is scheduled to remain in effect until the end of June.

The main cause of this year's surge in oil prices is OPEC's cuts. Maintaining them will provide the market with a lot of underlying support. However, OPEC is no longer quite the arbiter it once was, and the impact of production cuts within the cartel will be mitigated by supplies from outside of it.

Nevertheless, in December 2023, US oil production set a record. From there, it might be stuck there for the near future. OPEC might be more confident to continue with production cutbacks considering the possibility that they will be even more successful.

Global Oil supply forecast 2024

Through 2025, non-OPEC+ producers—led by the Americas—will continue to propel the expansion of the global oil supply due to the OPEC+ alliance's ongoing output limitations, shows the IEA's oil market report released in April. Since the alliance eliminated approximately 2 mb/d of supply from the market since the end of 2022, while non-OPEC+ increased by about the same amount, OPEC+'s market share has already fallen to all-time lows.

It appears that in 2024, when non-OPEC+ increases output by a further 1.6 mb/d, this trend will continue. It is estimated that OPEC+ supply will decrease by 820 kb/d if the cuts are sustained into the second half of the year. As non-OPEC+ lead gains for a third consecutive year, climbing by 1.4 mb/d, the world oil supply is expected to rise by 1.6 mb/d in 2025, setting a new high of 104.5 mb/d.

To put things in perspective, the new oil production from the US, Brazil, Guyana, and Canada alone may be sufficient to cover the growth in global oil demand forecasted for this year and 2025. With an additional 1.2 mb/d in 2024 and 1 mb/d in 2025, these four nations are expected to produce at record-high levels once more. Even while momentum in the US slows down, in 2024 and 2025 it adds 650 kb/d and 540 kb/d, respectively, making it the largest source of supply increase globally.

Their forecast of global oil inventories in 2Q24 is expected to drop by more than 0.9 million barrels per day due to a mix of flat output and increased consumption, which EIA anticipate will push oil prices higher. Oil prices are expected to remain high in 2Q24, averaging $90, which is $2/b higher than in the previous month's STEO due to the tighter market balance.

They forecast that oil inventories will start to rise in 2025 because EIA think that once the OPEC+ supply cuts expire, production will rise. In 2025, the agency forecast that global oil inventories will rise by an average of 0.4 million barrels per day, which would drive down prices.

Global Oil Demand Forecast 2024

The growth in global oil demand has been lowered down from last month's IEA report by about 100 kb/d to 1.2 mb/d due to abnormally low OECD deliveries at the beginning of the year. As the post-Covid 19 bounce has peaked, the pace of expansion will slow down even more to 1.1 mb/d in 2025, according to their update Oil demand forecast for 2025. The projection is dominated by non-OECD nations, with demand growth of 1.3 mb/d expected in 2024 and 1.2 mb/d in 2025. In comparison, the OECD's consumption is expected to decrease by 60 kb/d in both years. Even though its portion of the global growth declines from 79% in 2023 to 45% in 2024 and 27% the following year, China is still leading the growth.

According to IEA's report, strong non-OPEC+ production combined with a predicted slowing in the increase of demand will reduce the call on OPEC+ crude by about 300 kb/d in 2025, to an average of 41.5 mb/d. Except for the Covid-19 period, effective spare capacity might reach 6 mb/d, the bloc's largest supply buffer to date, if production were to keep pace with that call.

Compared to last month's EIA oil forecast, the agency raised their estimate of the world's liquid fuel consumption for 2022 by almost 0.8 million barrels per day (b/d). Most of this change can be attributed to non-OECD consumption, which is larger than our initial projections.

The higher baseline historical data for 2022 in turn increased EIA's forecast of oil consumption in 2023 and their forecasts for 2024 and 2025. They now estimate that global liquid fuels consumption averaged 102.0 million b/d in 2023, a 2.0 million b/d increase from 2022 and about 1.0 million b/d higher than in last month’s STEO. Global liquid fuels consumption in their oil forecast for Q2 now averages 102.9 million b/d in 2024 and 104.3 million b/d in 2025, which is between 0.4 million b/d and 0.5 million b/d more in both years than in last month’s STEO. YoY oil forecast consumption growth in 2025 is largely unchanged compared with the March oil forecast report.

In contrast to their earlier oil forecast and energy outlook, the modifications to historical consumption reduced demand growth in 2024 even though they increased the projected petroleum consumption. The drivers of growth, however, are still the same: non-OECD Asian nations, especially China and India, are responsible for most of the growth in the global demand for liquid fuels, but the Middle East and the US are also expected to see substantial growth.

Technical Oil Prices Forecast Q2 2024 - How High Can It Go?

Oil prices had ended 2023 with sharp losses, falling more than 20% between their late-October peak and mid-December and bounced back towards the highs of September 2023 during the first quarter of the year.

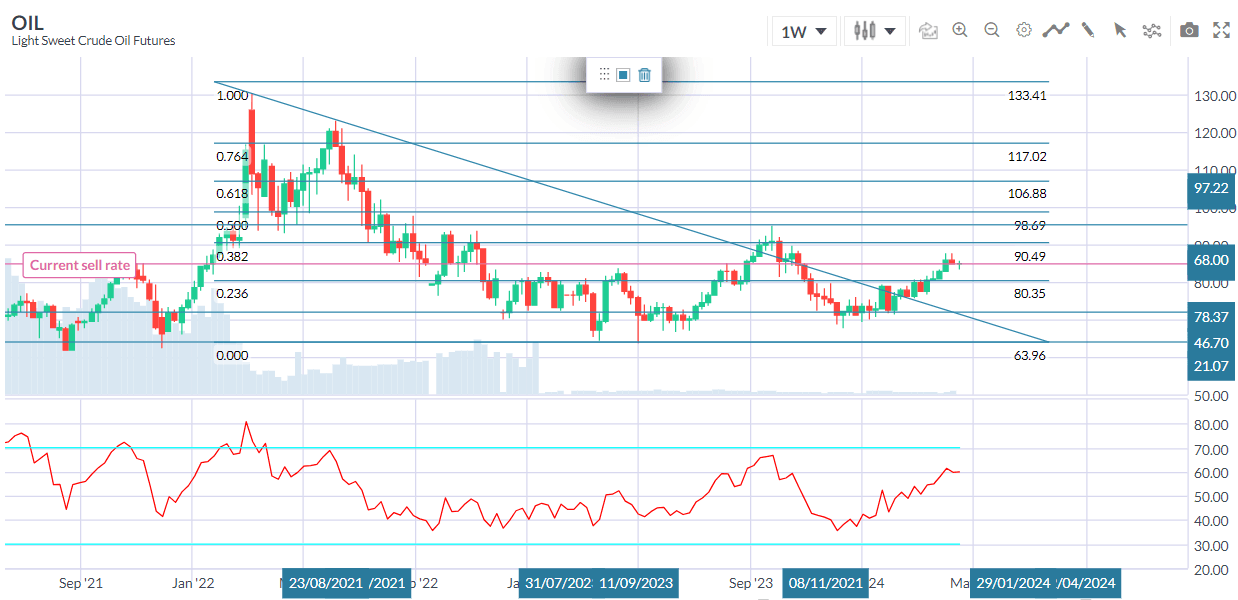

WTI Oil Forecast – Long-term trendline resistance on the horizon

The US benchmark has scaled five-month highs at the beginning of Q4 and is closing in on a longer-term downtrend line on its weekly chart. This has capped the market since mid-2022, admittedly with few tests.

If unbroken the current uptrend channel will take the market above this line if it crosses the $83 mark. A rise to that level would put resistance at the last significant high back in focus. That was the $94.57 mark hit on September 25 last year, a one-year high at the time.

Support looks solid in the $64-$65 region, but the direction of any breakout from the current ascending channel is likely to be instructive.

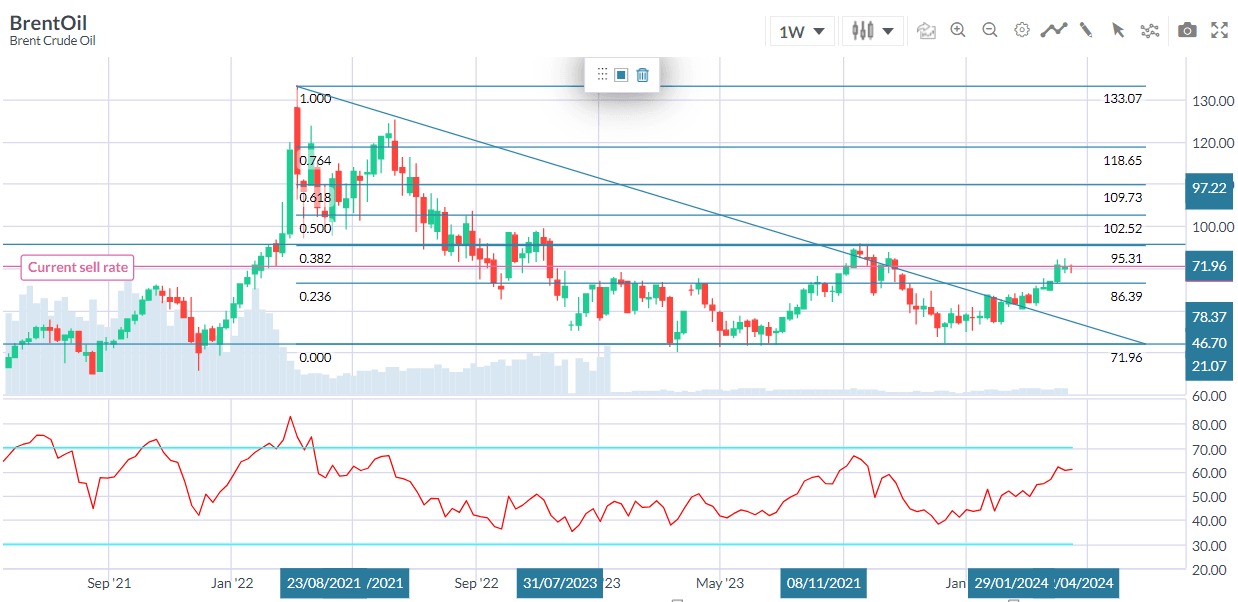

Brent Oil Forecast – Testing critical horizontal resistance

International benchmark Brent’s chart looks broadly like WTI’s, though a little less obviously bullish.

The Brent oil prices currently trade between the 50% and 61.8% Fibonacci retracement levels of their rise to the highs of March 2022 from the lows of October 2020. These offer support at $75 which has survived various tests since the start of 2023.

Bulls will need to consolidate above the $86.75 mark if they are to push on to the highs around $95 last seen, very briefly, in September.

To learn more about technical analysis as a forecasting tool visit CAPEX Academy.

Oil Brands

When talking about the commodity oil traded on the financial markets, we can distinguish two types. The most popular, and also the most traded, is the American oil called WTI. The other popular variant is Brent.

West Texas Intermediate (WTI)

Light sweet crude oil (WTI) is widely used in US refineries and is an important benchmark for oil prices. WTI is a light oil with a high API density and low sulfur content. This determines the density of the oil in relation to water. WTI oil is widely traded between oil companies and investors. Most trading is done through futures through CME Group. The Light Sweet Crude Oil (CL) future is one of the most traded futures worldwide.

Most of the oil of this type is stored in Cushing, an important hub for Oklahoma's oil industry. Here are large storage tanks connected to pipelines that transport the oil to all United States regions. WTI is an important feedstock for refineries in the Midwestern United States and on the coast of the Gulf of Mexico.

Brent Crude Oil

Brent oil is an important benchmark for the petroleum rate, especially in Europe, Africa, and the Middle East. Its name is derived from the Brent oil field in the North Sea. This Royal Dutch Shell oil field was once one of Britain's most productive oil fields, but most of the platforms there have since been decommissioned.

The correlation between these two futures' price development is high, and we have seen several times in recent years that Brent's price was more than $10 higher than usual. At the end of 2020, the difference was approximately $3. Such differences are caused, among other things, by supply and demand, including the costs of shipping or storing oil.

Oil Price Prediction for 2024, 2025-2030

The WTI and Brent crude oil prices were forecasted to stagnate in the first part of the year and increase in the second part of 2024, reflecting EIA's and IEA's expectations of tightening balances in global oil markets. With new developments in the past weeks, what are the latest Q2 crude oil price predictions?

Here are the most important oil price predictions released or updated by some of the most influential financial institutions in the world today.

EIA revises up crude oil price forecasts for Q2 and 2024

In the first Short-Term Energy Outlook (STEO) of Q2 2024, the US Energy Information Administration (EIA) forecasts the Brent crude oil spot price will increase to an average of $90/bbl in Q2 2024 from an average of $78/bbl in December 2023 and more than their Oil price forecast in March, partly driven by their expectation of strong global oil inventory draws during this quarter and ongoing geopolitical risks.

EIA updated its forecast for the Brent price in 2024. EIA forecast the Brent spot price will average $89/bbl next year, an increase from the previous Oil price forecast of $83/bbl at the beginning of the year.

Goldman Sachs lowers its 2024 oil price forecast by 12% due to bumper US output

The Wall Street bank said recently that it now expects Brent, the global oil benchmark, to average $81 a barrel in 2024, down from its previous estimate of $92 a barrel. It forecasts Brent Oil to peak at $85 a barrel next June.

The bank’s analysts said “the key reason” for the revised price expectations was “ongoing gains in drilling speed and well completion intensity” in the United States. Goldman Sachs said, the supply cuts by OPEC+, a potential economic rebound in China, as well as a “modest” risk of a US recession, among other factors, are likely to limit the extent of falls in oil prices.

Barclays lowers 2024 Brent oil price forecast to $93/b on demand concerns

Barclays lowered its oil price forecast for Brent crude futures for 2024 by $4/b to $93/b but noted that the recent selloff in global oil prices may be overdone. Lingering concerns over the health of the global economy were supported this week by data showing a surprise spike in US oil stocks and economic weakness in top crude importer China, Barclays said in a late 2023 note.

Barclays lowered their 2024 Brent forecast by $4/b but maintain their above-curve and consensus view on prices. They've also noted that its Brent price forecast for 2024 remains $14/b ahead of the Brent forward curve.

Oil price could reach $150 a barrel in 2024, warns World Bank

The World Bank has warned that if the Israel-Hamas battle turns into a regional conflict, oil prices might rise to $150 in 2024. The Israel-Hamas war has had a limited effect on oil prices so far. However, an escalation of the current conflict could shrink global oil supply by as much as eight million barrels per day, leading to sharp price increases, said World Bank.

This disruption in the oil supply would be like the one that resulted in the loss of around 7.5% of the world's oil supplies during the Arab oil disruption of 1973. However, the World Bank notes that countries are better suited to deal with an oil supply shock now than they were in 1973.

ING forecast rising Oil price in the second half of 2024

The supply cuts should be enough to remove the surplus in 1Q24 and leave the market in a small deficit early next year, said ING. However, their balance still shows a small surplus in 2Q24, which means that the market is largely balanced over 1H24. This could and will likely change depending on how OPEC+ members go about unwinding these voluntary cuts.

Given that balanced market, ING forecast Oil Brent to remain trading in the low $80s in the early part of next year. The second half of 2024 will see the market return to deficit, which suggests we see prices moving higher in 2H24. Though, the Dutch Bank forecast Brent Oil to average US$91/bbl over the last six months of 2024.

However, at the beginning of Q2, ING analysts revised higher their short-term oil price forecast, while also adjusting the profile later in the year with prices likely to peak in the third rather than in the final quarter of the year as previously expected.

Citi forecast Brent crude oil prices to $73 / bbl in Q2 2024

Citigroup's Brent oil forecasts for 2024 points toward $73/bbl price for Brent by Q2 2024 and $68/bbl by the end of the year. Citi do warn though that there is potential for explosive price gains should there be a polar vortex or geopolitical upheaval. However, they see a low risk for a potential widening of the war in the Middle East.

Citi believes that supply will outpace demand by an average 1.4 million b/d in 2024 citing contributions from non-OPEC supply from Argentina, Brazil, Canada, Guyana and the U.S.

JPMorgan forecasts crude will average $83 a barrel in 2024

After falling in 2023, J.P. Morgan Research forecasts Brent oil prices to remain largely flat in 2024 and edge down a further 10% in 2025: “Our Brent Oil forecast has not changed since June and is expected to average $83 per barrel (bbl) in 2024”.

This will be buttressed by solid supply-demand fundamentals: “Despite sustained economic headwinds, we see oil demand rising by 1.6 million barrels per day (mbd) in 2024, underpinned by robust emerging markets, a resilient U.S. and a weak but stable Europe.”

Fitch Ratings forecast an oil price shock would hit 2024 growth and boost inflation

Fitch’s Global Economic Outlook (GEO) forecast oil prices will average USD75 a barrel (bbl) and USD70/bbl in 2024 and 2025, respectively. Using simulations from the Oxford Economics Global Economic Model, they estimated the impact of higher oil prices throughout 2024-2025 on their baseline GEO growth and inflation forecasts.

Their scenario assumes that, due to supply restrictions, oil prices average USD120/bbl in 2024 and USD100/bbl in 2025. Higher oil prices would dampen GDP growth in almost all the GEO’s ‘Fitch 20’ economies, although the impact would largely dissipate in 2025. The absence of a significant growth rebound in 2025 implies a longer lasting, if generally moderate, impact on GDP levels in most countries, which could affect assessments of potential growth.

Algorithm-based (AI) Oil Price Forecasts

Crude oil is expected to trade at 86.36 USD/BBL by the end of this quarter, according to Trading Economics global macro models and analysts' expectations. Looking forward, they estimate it to trade at 91.86 in 12 months' time.

Brent crude oil is expected to trade at 90.97 USD/BBL by the end of this quarter, according to Trading Economics global macro models and analysts' expectations. Looking forward, they estimate it to trade at 96.28 in 12 months' time.

Long Forecast expects Brent Oil to close 2024 at 94.90 with a maximum of 106 in August, while WTI to close 2024 at 91.34 with a maximum price of 103 in August.

Wallet Investors forecast Brent Oil to close 2024 at $690.20 with a maximum price of August.

Oil Price Forecast for the Next 5 Years and Beyond (2025 – 2050)

Some expect demand for fossil fuels could fall in the medium-to-long term, leading to a lower oil price in 10 years’ time. Consequently, the oil price in 2030 is widely expected below $100/bbl.

According to EIA’s annual energy outlook report, the agency held a conservative outlook for its oil price forecast for 2030. It expects the average Brent crude prices at $61/bbl in 2025, $73/bbl in 2030, $80/bbl in 2035, $87/bbl in 2040, $91/bbl in 2045 and $95/bbl in 2050.

Energy consultancy Wood Mackenzie said if global fuel consumption falls in line with the emission targets set to limit global warming, oil price projections in 2030 could fall as low as $40/bbl.

Wallet Investor forecast WTI Oil to trade at $10294 at the end of 2025, while the Brent Oil price prediction 2025 is $97.

The Oil price prediction for 2025 at Long Forecast is: WTI 113, Brent 124.

The Oil price forecast for the next 5 years is 100.75 for WTI and 131.53 for Brent according to Long Forecast and $143 for WTI and $174 for Brent according to Wallet Investor.

When looking for oil-price predictions, it's important to remember that analysts' forecasts may be wrong. This is because their projections are based on a fundamental and technical study of WTI and Brent oil commodities’ historical price movements. But past performance and forecast are not reliable indicators of future results.

It is essential to do your research and always remember your decision to trade depends on your attitude to risk, your expertise in the market, the spread of your investment portfolio, and how comfortable you feel about losing money. You should never invest money that you cannot afford to lose.

How Did the Price of Crude Oil Change Over Time?

Below is a chart showing the price for West Texas Intermediate (NYMEX) Crude Oil over the last 5 years. The shown prices are in U.S. dollars. On the chart, you can clearly see the monstrous drop that happened earlier this year, and how the price has been going up and stabilizing in the months thereafter.

A Recent History of Oil

At the end of April 2020 (due to the Saudi and Russia conflict - more on that later), the oil price crashed, and the May WTI future even dipped below $0. The stock markets recovered strongly during the summer, and the oil price had also found its way up again. In August, the oil price rose well above $ 40 a barrel. With that price, the largest oil companies got some air also, but it is still far from enough for most to make a profit.

At the beginning of September, the oil price had suddenly fallen hard again. Simultaneously, with the mini-crash with the US stock markets, a crude oil barrel's worth dropped by about 15% to below $37 a barrel. This brought the oil price back below $40 a barrel for the first time since July. The drop is partly because Saudi Arabia had lowered its sales prices for October and the fear that the number of COVID-19 infections will increase rapidly in several countries.

The rebound in the number of infections could thwart the global economic recovery and decrease fuel demand. With several refineries lowering tariffs again, it seems they want to prevent oil stocks from rising back to record levels. The oil price was able to recover so strongly in recent months, thanks to the OPEC + countries' agreements regarding the reduction in production. However, due to the crisis, many countries are looking for additional income sources. Therefore, some countries are not fully complying with the agreements made. As a result, more oil flows into the market, which also has a depressing effect on oil prices.

March 9th, 2020: 30% Oil Price Crash

Monday, March 9th, can go into the history books as "Black Monday" for the oil price. Negotiations between Saudi Arabia and Russia had come to nothing.

The oil price was under pressure in previous months due to the spread of the coronavirus. The world economy was on the back burner, and as a result, the oil demand had declined considerably. By limiting oil production, the countries that are part of the oil cartel hoped to stabilize or increase the price themselves. Saudi Arabia, in particular, is strongly in favor of limiting oil production.

Saudi Arabia was now trying to force Russia in another way to join the OPEC plan. The Saudi’s were going to increase production considerably and flood the market with oil. As a result, the price of a crude oil barrel had opened more than 30% lower, the lowest price since 2016. A low oil price is disastrous for most countries. Most OPEC countries are almost entirely dependent on oil revenues.

America's shale farmers may be hit hardest. The shale revolution seems to be built more and more on quicksand, as costs remain high and the new resources that are found have a much shorter lifespan. Even with an oil price of around $60 a barrel, many of these producers were already struggling. The unrest surrounding the coronavirus also makes it difficult to raise external capital. With Saudi Arabia pushing the oil price further down, the situation seems to be untenable for many producers. Players with a fragile balance and relatively high costs are unlikely to make it. What Saudi Arabia failed to achieve in 2016 now seemed to have a good chance of success.

April 21st, 2020: WTI Goes Below Zero

In April 2020, we saw a situation in the oil markets that has never occurred before. The West Texas Intermediate Crude Oil (WTI) futures contract for May fell more than 100%. The price fell during the day and took an unprecedented dive later in the evening to $ -37.63/barrel, meaning that oil producers would indeed have to pay buyers to collect the oil.

This is mainly because the storage capacity in Cushing, Oklahoma is full. And it is precisely there that this oil is delivered. Traders and large companies who were long yesterday but ran out of storage capacity or liquidity to purchase oil were forced to close futures before expiry.

Shale Oil Influence

Oil production increased rapidly, and OPEC was not happy about this. They saw the increase in supply in the Middle East as competition. OPEC, therefore, came up with the idea of fully opening the oil taps. The production costs of shale oil were many times higher. The result was a drop in oil prices from about $110 a barrel to below $30 at the beginning of 2016. OPEC hoped to wipe out shale farmers in this way.

This strategy failed, and the OPEC countries themselves ultimately suffered considerable disadvantages from this strategy. For years they saw their income more than halved. In the meantime, the shale farmers have learned to work cheaper and more efficiently, and they are already profitable at a lower oil price. What’s typical of this form of oil extraction is that production can be increased quickly.

OPEC Influence

Demand for oil will remain stable in the coming years. But it is also apparent that there is a lot of extra supply on the market now that American oil production is rapidly increasing. Shale oil, in particular, is extracted from the ground here. The shale revolution was set in motion in 2014 by the sharp rise in oil prices. This form of oil extraction was therefore profitable, despite the high production costs. Due to the attractive market, the oil companies sprang up like mushrooms.

OPEC is trying to limit production to keep the oil price at a reasonable level. Most countries benefit from a somewhat higher, but in any case, stable, oil price. According to OPEC, the oil industry must invest more than $11,000 billion over the next 20 years. If producers don't do that, there will be a shortage. In principle, shale farmers have already invested enough in recent years to absorb a large part of these shortages.

Furthermore, OPEC states that demand continues to increase despite the emergence of electric cars and the like. OPEC writes that the massive expansion of air travel creates a greater demand for oil than the emergence of alternative energy sources can diminish.

Since the low oil price in 2016, OPEC has been trying to support the low oil price. This is done by agreeing on production restrictions with all countries that are members of OPEC. The agreements do not always go smoothly, as Iran and Iraq do not always adhere to these agreements. On the other hand, the US and other countries continue to produce more and more oil, putting oil prices under pressure for a long time.

Factors That May Affect the Price of Crude Oil

We know that oil is an indispensable raw material in the world and that it is used both as raw material and fuel to make plastics, pharmaceuticals, and many other products. Hence, the demand for oil remains strong, and these industries' health will determine most of the world's oil demand. If demand from these industries increases while production stagnates, it will lead to higher prices for this commodity. Of course, and vice versa, if these industries are in a recession, their oil demand will be lower, so demand will decline. If production remains stable or increases in this case, it will logically lead to a drop in the price of a crude oil barrel.

As you will have understood, it is mainly by analyzing the difference between supply and demand that you will determine how the price or price of crude oil will evolve.

It should also be noted that this analysis is slightly more complex today than it used to be. Until a few years ago, it was pretty easy to understand how these prices would behave. At the time, the US was the largest consumer of crude oil. On the other hand, OPEC was the main supplier to the market in terms of production. But over time and the years, this situation has become more complex and slightly more confusing. One explanation for this phenomenon is that oil drilling technologies have improved greatly and resulted in better supply. Besides, we have seen the emergence of alternative solutions for this production. Finally, new players have also joined, including China, a major oil consumer in the world.

Below we have listed factors that change the supply or demand for oil and thus contribute to the evolution of this commodity's price and price.

1. Production data in barrels per day from OPEC countries

Too much production generally leads to lower oil prices per barrel and vice versa. US crude oil inventory data is published weekly, which also affects WTI.

2. Supply, which is published weekly on the economic calendar.

Big supply also contributes to falling prices, while little supply leads to higher prices.

3. The international geopolitical situation

Conflicts affecting the oil-producing and exporting countries often influence the development of the price per barrel.

4. The value of the US dollar on the currency market.

As a barrel of oil is denominated in dollars, this currency will be weaker, and more oil purchases will be stimulated by holders of other currencies.

Final words

Make sure to create a free demo account on CAPEX.com! CAPEX.com is a useful platform for both novice and expert traders. You will be up to date on interesting updates about crude oil as an investment asset, and the user-friendly interface will come in handy if you decide to trade crude oil or any other commodity.

If you look at the price changes of oil for a while now, you will start to see a pattern, and as an investor, you can respond smartly to this.

If you want to invest in oil, it is a good investment to get in when the oil price is at a certain bottom. Of course, there is no guarantee that oil prices will ever rise as much as in the past. Oil is a limited resource and is probably the most precious material in the world. Investing in commodities is one way to improve your overall investment portfolio.

Sources:

- https://www.opec.org/opec_web/en/publications/338.htm

- https://www.iea.org/reports/oil-market-report-april-2024

- https://www.eia.gov/outlooks/steo/pdf/steo_full.pdf

Other resources:

- Gold forecast & price predictions 2024

- EurUsd forecast & price predictions 2024

- Dow Jones forecast & price predictions 2024

- Natural Gas forecast & price predictions 2024

- Turkish Lira forecast & price predictions 2024

- Silver forecast & price predictions 2024

- NASDAQ 100 forecast & price predictions 2024

- British Pound forecast & price predictions 2024

- USD to INR forecast & price predictions 2024

- Egyptian Pound forecast & price predictions 2024